Omdia: AI and Cloud-Native Transformation to Drive Global Telco Network to $24.8bn by 2030

Omdia: AI and Cloud-Native Transformation to Drive Global Telco Network to $24.8bn by 2030

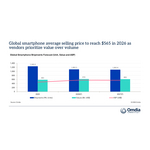

LONDON--(BUSINESS WIRE)--Global spending on telco network cloud infrastructure and software is projected to grow from $17.4 billion in 2025 to $24.8 billion by 2030, representing a compound annual growth rate (CAGR) of 7.3%, according to Omdia’s new Telco Network Cloud Market Tracker – 2025 Annual Forecast Report.

“Telcos are rapidly modernizing their infrastructure to support cloud-native network functions and AI-driven automation,” said Inderpreet Kaur, Senior Analyst at Omdia.

Share

The report highlights a significant acceleration in cloud adoption among communications service providers (CSPs), with 12% growth expected in 2025, doubling the rate seen in 2024. This momentum is fueled by the increasing maturity of cloud-native tooling, automation frameworks, and the integration of AI and GenAI into network operations.

“Telcos are rapidly modernizing their infrastructure to support cloud-native network functions and AI-driven automation,” said Inderpreet Kaur, Senior Analyst at Omdia. “The migration to containerized network functions (CNFs) is encouraging telcos to focus their investments on platforms that support both virtualized and containerized network functions (VNFs and CNFs).”

Key Telco Cloud Market Trends:

- AI Infrastructure: Over 62% of operators now consider AI/ML support critical to cloud infrastructure decisions. Vendors like NVIDIA, Red Hat, and VMware are enabling on-premises AI capabilities tailored for telco environments.

- Cloud-Native Growth: Spending on Kubernetes-based platforms is forecast to grow at a 25% CAGR, while spending on existing VM-only environments is slowing down.

- Public Cloud Adoption: Public cloud usage for network workloads is expected to rise from 3% in 2024 to 13% by 2030, with hyperscalers offering telco-specific solutions.

- Vendor Leadership: Red Hat leads the cloud infrastructure management market with a 25% share, positioning itself as the top vendor in telco cloud platforms.

Cloud-native transformation is tightly aligned with telecom operator’s automation goals. Technology vendors addressing this market segment should embrace CI/CD pipelines and GitOps practices to automate the full lifecycle of clusters and network workloads.

ABOUT OMDIA

Omdia, part of Informa TechTarget, Inc. (Nasdaq: TTGT), is a technology research and advisory group. Our deep knowledge of tech markets grounded in real conversations with industry leaders and hundreds of thousands of data points, make our market intelligence our clients’ strategic advantage. From R&D to ROI, we identify the greatest opportunities and move the industry forward.

Contacts

Fasiha Khan: fasiha.khan@omdia.com