Omdia: India Smartphone Market Grew 3% as Brands Gear Up for Festive Season

Omdia: India Smartphone Market Grew 3% as Brands Gear Up for Festive Season

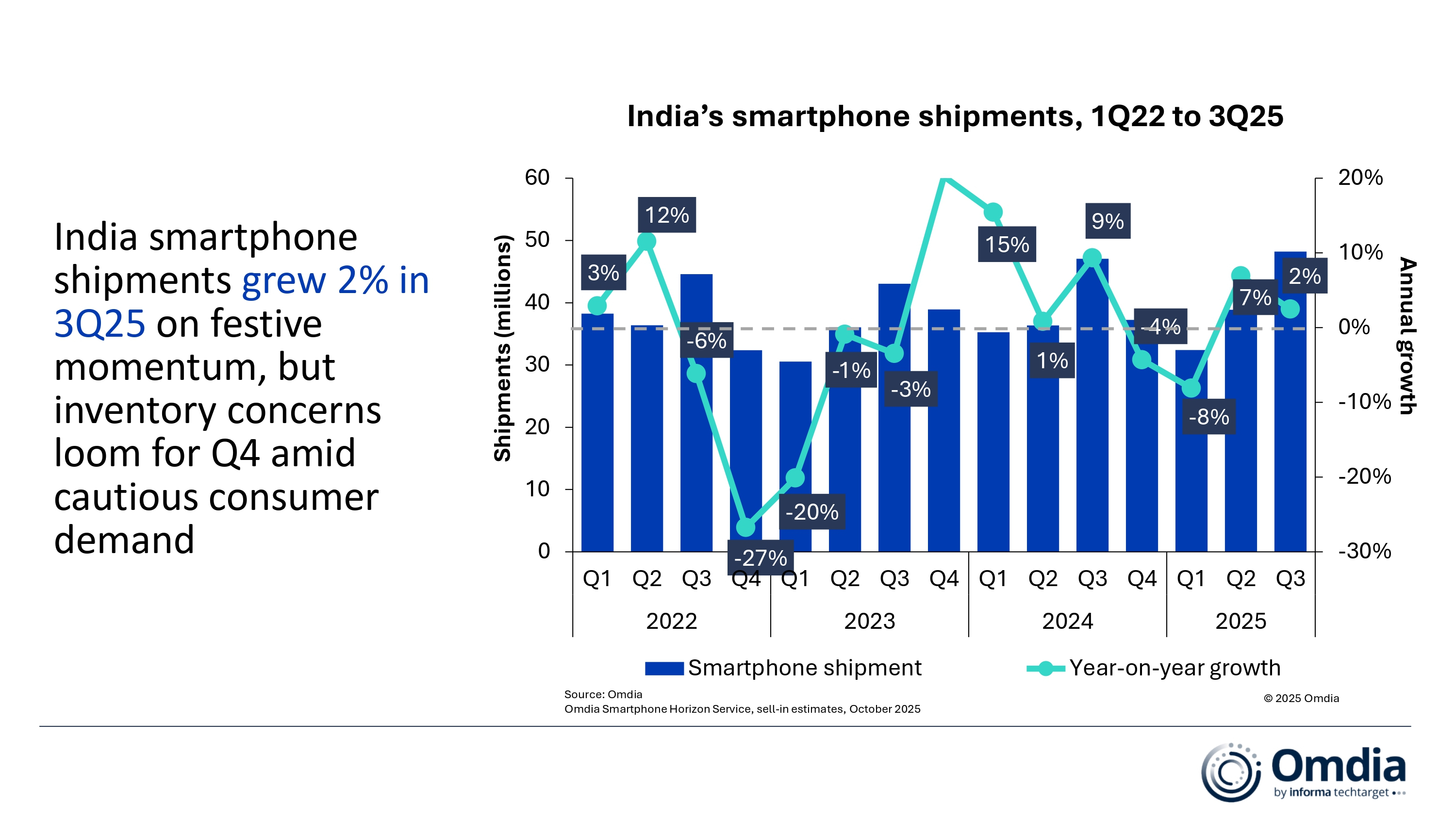

LONDON--(BUSINESS WIRE)--India’s smartphone market grew 3% year-on-year (YoY) in Q3 2025, reaching 48.4 million units shipped according to the latest research from Omdia. Vendors filled the channels with new stocks in expectation of a high-demand festive period. The modest growth was driven by a wave of new launches in July and August, retail incentivization and an earlier festive season that pulled forward inventory flows.

“With limited organic demand, 3Q’s momentum was largely sustained through incentive-led channel push rather than pure consumer recovery,” said Sanyam Chaurasia, Principal Analyst at Omdia.

Share

vivo (excluding iQOO) extended its lead in the market with 9.7 million units shipped capturing a 20% market share. Samsung ranked second with 6.8 million units and a 14% market share followed by Xiaomi in third place, narrowly overtaking OPPO (excluding OnePlus), with both vendors shipping 6.5 million units. Apple returned to the top five with 4.9 million units, with incremental growth driven by smaller tier cities.

“With limited organic demand, 3Q’s momentum was largely sustained through incentive-led channel push rather than pure consumer recovery,” said Sanyam Chaurasia, Principal Analyst at Omdia. “Vendors reallocated marketing budgets to high-impact retail incentive programs that rewarded sell-through, ranging from cash-per-unit bonuses to tiered margins and dealer contests with rewards such as gold coins, bikes, and international trips. These incentives motivated distributors and retailers to absorb higher inventory ahead of the festive season. At the same time, vendors intensified consumer-facing schemes – from zero-down-payment EMIs, micro-instalment plans, bundled accessories and extended warranties – to drive conversions.

“vivo extended its lead with a balanced portfolio, aggressive retail programs, and a standout promoter network,” continued Chaurasia. “Its T-series scaled online early in the festive period, while the V60 and Y-series expanded across large-format and rural retail. Samsung gained mid-premium traction with old generation models, refreshed Snapdragon-powered S24 and S25 FE but faced pressure in the entry tier. OPPO’s volumes were driven by an aggressive multi-layered festive channel program, anchored around the F31 series. Outside the top five, Motorola hit a record 4 million units, up 53% YoY, led by G-series and Edge 60 offline expansion. Nothing grew 66%, with CMF Phone 2 Pro and Phone 3a driving volumes, as it repositioned CMF as India’s first locally headquartered sub-brand via its tie-up with Optimus.

“Apple posted its highest-ever shipments in India in 3Q, securing 10% share,” added Chaurasia. “Smaller cities drove volumes through aspirational demand, aggressive festive offers and wider availability. While older iPhones 16s and 15s drove major shipments under discount-led upgrades, the iPhone 17 base model gained traction supported by a strong iPhone 12–15 install base upgrades. Looking ahead, Apple will aim for Pro-model upgrades and deepen its ecosystem to drive long-term value.”

“Despite early momentum, 3Q’s gains are unlikely to sustain into a strong year-end. While government-led reforms such as GST reductions on large appliances lifted overall retail sentiment, smartphone-specific demand recovery remains limited. Urban consumers continue to delay upgrades due to employment uncertainties and rising cost sensitivity, despite better product availability and financing schemes. As a result, sell-out traction lags behind shipment growth, raising concerns of inventory build-up in 4Q, especially after November. In contrast, rural demand has been relatively stable, but insufficient to offset cautious urban sentiment. For full-year 2025, we continue to expect a modest decline, reflecting a fragile recovery cycle that remains highly sensitive to economic tailwinds and channel correction dynamics,” concluded Chaurasia.

India’s smartphone shipments and annual growth

|

|||||

Vendor |

3Q25 shipments (million) |

3Q25

|

3Q24

|

3Q24

|

Annual

|

vivo |

9.7 |

20% |

8.2 |

17% |

19% |

Samsung |

6.8 |

14% |

7.5 |

16% |

-9% |

Xiaomi |

6.5 |

13% |

7.8 |

17% |

-17% |

OPPO |

6.5 |

13% |

6.3 |

13% |

3% |

Apple |

4.9 |

10% |

3.3 |

7% |

47% |

Others |

14.0 |

29% |

13.9 |

30% |

1% |

Total |

48.4 |

100% |

47.1 |

100% |

3% |

|

|

|

|||

Note: vivo excludes iQOO. OPPO excludes OnePlus. Xiaomi estimates include sub-brand POCO. Percentages may not add up to 100% due to rounding.

|

|

||||

ABOUT OMDIA

Omdia, part of Informa TechTarget, Inc. (Nasdaq: TTGT), is a technology research and advisory group. Our deep knowledge of tech markets combined with our actionable insights empower organizations to make smart growth decisions.

Contacts

Sanyam Chaurasia: sanyam.chaurasia@omdia.com