Omdia: Global PC Shipments Grew 3% in 1Q26 as Supply Chain Impacts Emerged

Omdia: Global PC Shipments Grew 3% in 1Q26 as Supply Chain Impacts Emerged

LONDON--(BUSINESS WIRE)--According to the latest research from Omdia, total shipments of desktops, notebooks, and workstations in 1Q26 increased by 3.2% year-over-year to 64.8 million units. Notebooks (including mobile workstations) saw a modest year-over-year increase of 2.6% in Q1 to 50.8 million units. Meanwhile, desktops (including desktop workstations) performed slightly better, up 5.4% to 14.0 million units. Growth was supported by vendors and channel partners pulling orders forward ahead of a widely anticipated increase in component costs, the continuation of the Windows 10 replacement cycle that is still driving commercial refresh budgets, and by a heavier than usual slate of spring product launches across both Windows OEMs and Apple.

“With supply-chain pressures still building, Q1’s modest growth is likely to mark the high point for the year,” said Ben Yeh, Principal Analyst at Omdia.

Share

“With supply-chain pressures still building, Q1’s modest growth is likely to mark the high point for the year,” said Ben Yeh, Principal Analyst at Omdia. “Memory and storage costs are expected to rise further and more steeply than previously assumed from Q2, squeezing PC vendor gross margins and forcing them to pass costs through to channel partners and end-customers. AI data center build-outs are crowding consumer categories out of memory and storage supply, which have already seen roughly five-fold and three-fold cost increases respectively since Q1 2025. CPU prices are a smaller but compounding pressure, with Intel and AMD projecting increases of 10-25% into Q2.”

With costs set to rise across the bill of materials, vendors have every incentive to protect shipments, revenue and gross margin by pulling deliveries forward, and Omdia’s regional analysis is consistent with that behavior across most of Q1. Preliminary regional data suggest that channel partners in North America have already absorbed as much as they can before end‑user prices rise. In Japan, the market has begun to show a more pronounced downturn, weighed down by the high shipment volume base in 1Q25 and by more severe cost and component supply pressures in the education segment. Given the education-driven surge throughout 2025, fading policy momentum could also become one of the main drivers of contraction in 2026.

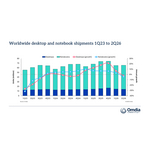

Worldwide desktop and notebook shipments (market share and annual growth) Omdia PC Market Pulse: 1Q26 |

|||||

Vendor |

1Q26

|

1Q26

|

1Q25

|

1Q25

|

Annual

|

Lenovo |

16,529 |

25.5% |

15,205 |

24.2% |

8.7% |

HP |

12,142 |

18.7% |

12,761 |

20.3% |

-4.9% |

Dell |

10,291 |

15.9% |

9,548 |

15.2% |

7.8% |

Apple |

7,112 |

11.0% |

6,750 |

10.7% |

5.4% |

Asus |

4,622 |

7.1% |

4,014 |

6.4% |

15.1% |

Others |

14,149 |

21.8% |

14,570 |

23.2% |

-2.9% |

Total |

64,844 |

100.0% |

62,848 |

100.0% |

3.2% |

|

|

|

|

|

|

Note: Unit shipments in thousands. Percentages may not add up to 100% due to rounding.

Source: Omdia PC Horizon Service (sell-in shipments),

|

|||||

Lenovo remained firmly in the top spot in 1Q26, further expanding its market share with year-over-year growth of 8.7%. Shipments reached 16.5 million units, and its share surpassed 25%. HP remained in second place, but weak performance in Europe and the United States resulted in a 4.9% decline, with shipments falling to 12.1 million units. Dell continued its strong momentum from 4Q25, posting 7.8% year-over-year growth as shipments reached 10.3 million units. Apple reached a market share of 11% with shipments growing 5.4% due to solid MacBook Air sales performance and the initial sell-in of the MacBook Neo. Asus maintained its double-digit shipment growth, with shipments climbing to 4.6 million units and market share reaching 7.1%.

ABOUT OMDIA

Omdia, part of TechTarget, Inc. d/b/a Informa TechTarget (Nasdaq: TTGT), is a technology research and advisory group. Our deep knowledge of tech markets grounded in real conversations with industry leaders and hundreds of thousands of data points, make our market intelligence our clients’ strategic advantage. From R&D to ROI, we identify the greatest opportunities and move the industry forward.

Contacts

Fasiha Khan: fasiha.khan@omdia.com

Eric Thoo: eric.thoo@omdia.com