New Updated Analysis Finds Nearly $1 Billion in Mortgage Cost Savings from FHFA’s Mortgage Credit Score Competition Decision

New Updated Analysis Finds Nearly $1 Billion in Mortgage Cost Savings from FHFA’s Mortgage Credit Score Competition Decision

- New Competitive VantageScore Incentive Programs Accelerate VantageScore 4.0 Adoption

- Switching to VantageScore 4.0 Saves Up to $132 Per Completed Mortgage

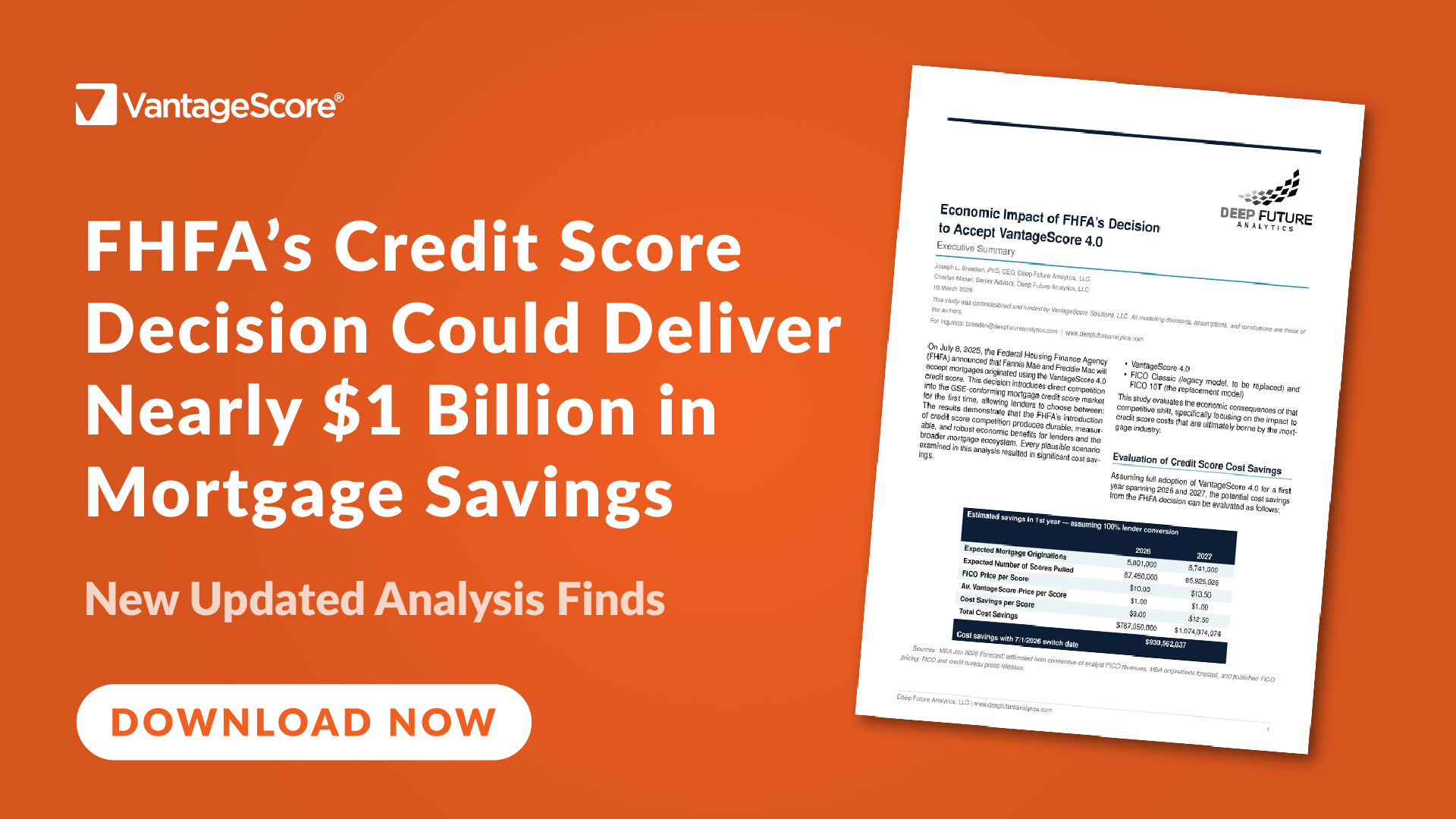

SAN FRANCISCO--(BUSINESS WIRE)--Homeowners and lenders could save nearly $1 billion over the first year of full adoption of VantageScore, according to a newly updated analysis of mortgage credit score costs published by Deep Future Analytics. The analysis was updated immediately following new competitive pricing incentives for VantageScore credit scores announced independently last week by Equifax, Experian and TransUnion. The study finds that the Federal Housing Finance Agency’s (FHFA) decision to allow the modern and more predictive VantageScore 4.0 to be used with immediate effect for Fannie Mae and Freddie Mac mortgages results in more than $930 million in cost savings during the first year of implementation.

“Competition in the credit scoring marketplace improves efficiency and dramatically lowers costs across the mortgage ecosystem,” said Dr. Rikard Bandebo, Chief Strategy Officer and Chief Economist at VantageScore. “This new analysis confirms that the full adoption of VantageScore 4.0 for mortgages helps reduce expenses in the mortgage origination process, leading to greater affordability for American homebuyers.”

VantageScore 4.0 incorporates trended credit data and advanced analytics to provide more predictive and inclusive credit scoring. The model scores millions of consumers who are often overlooked by legacy, outdated credit scoring models while improving performance in mortgage risk prediction.

Key findings include:

NEW INCENTIVE PROGRAMS ACCELERATE VANTAGESCORE 4.0 ADOPTION: Distributors of VantageScore 4.0 have independently announced a range of competitive incentive programs aimed at encouraging faster industry adoption while helping lower costs throughout the mortgage process. By aligning credit score cost savings with broader housing affordability goals, these programs support lenders transitioning to VantageScore 4.0 and expand access to more cost-effective mortgage underwriting solutions.

SAVINGS EXCEED $130 PER COMPLETED MORTGAGE AFTER SWITCHING TO VANTAGESCORE: Under the “full adoption” scenario examined in the analysis, lenders and borrowers together save approximately $115 to $132 in direct and indirect credit scoring costs per successfully completed mortgage application after switching to VantageScore 4.0.

Lenders and partners interested in adopting VantageScore models or participating in pilot programs can contact their credit bureau representatives:

- Equifax: mortgage_inquiries@equifax.com

- Experian: mortgages@experian.com

- TransUnion: TU_Mortgage@transunion.com

Download a full copy of the report from VantageScore’s website or by visiting the Deep Future Analytics website.

To learn more about VantageScore’s growth in the GSE-conforming mortgage market, visit the VantageScore Mortgage Resource Center.

About VantageScore®

VantageScore is the fastest-growing credit scoring company in the U.S., and is known for the industry’s most innovative, predictive and inclusive credit score models. In 2024, usage of VantageScore increased by 55% to hit 42 billion credit scores. More than 3,700 institutions, including nine of the top 10 U.S. banks, use VantageScore credit scores and digital tools to provide consumer credit products or generate greater insights into consumer behavior. The VantageScore 4.0 credit scoring model scores 33 million more people than traditional models. With the FHFA allowing the immediate use of VantageScore 4.0 for Fannie Mae and Freddie Mac guaranteed mortgages, the company is also ushering in a new era for mortgage lending.

VantageScore is an independent joint venture company owned by Equifax, Experian and TransUnion.

Contacts

Ola Fadahunsi | VantageScore

Email: ola@vantagescore.com

Phone: +1 (415) 740-2559