AI Powers Record 2024 Revenue, but Automotive and Industrial Struggles Linger Says Omdia

AI Powers Record 2024 Revenue, but Automotive and Industrial Struggles Linger Says Omdia

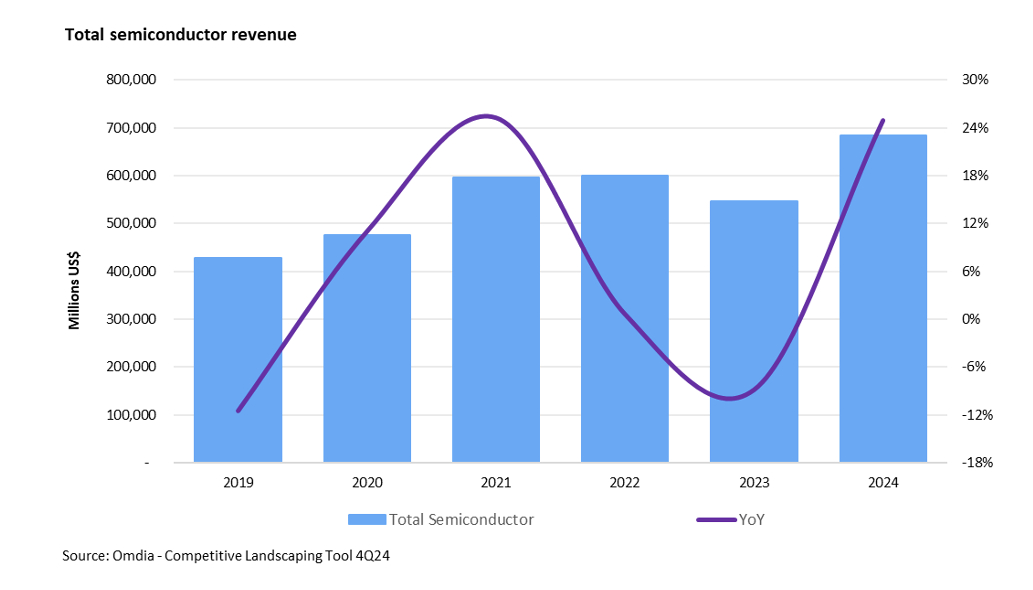

LONDON--(BUSINESS WIRE)--2024 marked a record-breaking year for the semiconductor market with annual revenue surging approximately 25% to $683 billion according to Omdia’s Competitive Landscaping Tool. The sharp rise was attributed to strong demand for AI-related chips, particularly high bandwidth memory (HBM), used in AI GPUs, which contributed to a 74% year-over-year growth in the memory segment. The rebound in memory helped lift the overall market after a challenging 2023.

However, this record-setting year masked uneven performance across the industry. While the data processing segment experienced strong growth, other key segments - automotive, consumer, and industrial semiconductor – experienced revenue declines in 2024. These struggles highlight areas of weakness within an otherwise booming market.

AI and memory complete a strong 2024

Throughout 2024, AI’s influence on the semiconductor market has been a dominant force, driving record revenues and reshaping industry dynamics. NVIDIA emerged as the clear leader, climbing the market share rankings with strong revenue growth the last few years due to its AI GPUs. HBM, a critical component for AI applications surged alongside, significantly boosting revenues for memory companies. While HBM outpaced other DRAM segments in growth, an improved supply-demand balance contributed to higher average selling prices (ASPs) and revenue gains across the broader memory market.

Industrial segment faces a second consecutive year of decline

The downturn in the industrial semiconductor segment, which began in 2023, deepened in 2024, posing challenges for companies focused on this sector. “Historically, the industrial semiconductor market has grown approximately 6% each year, however, after two years of above-average growth in 2021 and 2022, semiconductor market revenue declined in double digits in 2024,” said Cliff Leimbach, Omdia Principal Analyst. “Diminished demand coupled with inventory adjustments made 2024 a difficult year for the industrial segment. Companies with a large presence in this segment saw their market share rankings slip as a result.”

Automotive market stalls

While the automotive semiconductor market performed better than the industrial sector, it also experienced a revenue decline in 2024. After nearly doubling in size from 2020 to 2023, far exceeding the historical average annual growth rate of 10%, the sector saw an abrupt slowdown. Weakening demand led to a contraction in 2024, disrupting the steady upward trajectory the market had enjoyed in recent years.

NVIDIA takes the top spot as market rankings shift

NVIDIA’s dominance in AI-driven GPUs pushed it to the top position in semiconductor companies by revenue, surpassing Samsung which held the number one position in 2023.

The strong memory market also reshaped the leaderboard with Samsung, SK Hynix, and Micron all ranking among the top seven largest semiconductor companies by revenue. Each of these companies climbed at least one spot from their 2023 rankings, marking a significant shift from the previous year when they were spread across the top eleven.

ABOUT OMDIA

Omdia, part of Informa TechTarget, Inc. (Nasdaq: TTGT), is a technology research and advisory group. Our deep knowledge of tech markets combined with our actionable insights empower organizations to make smart growth decisions.

Contacts

Fasiha Khan: fasiha.khan@omdia.com