Health Care Organizations Deploy Cost-Cutting Initiatives as Labor Costs Increase

Health Care Organizations Deploy Cost-Cutting Initiatives as Labor Costs Increase

Base payroll expense, when adjusted for growth in headcount, has increased by 9.1%

CHICAGO--(BUSINESS WIRE)--SullivanCotter, the nation’s leading independent consulting firm in the assessment and development of total rewards programs, workforce solutions, and data products for health care and not-for-profits, has released findings from its 2023 Workforce Metrics Benchmark Survey.

New #research by @SullivanCotter shows health care labor costs rising, driving organizations to deploy cost-saving initiatives and create more sustainable workforce architecture. #HealthcareWorkforce #Survey #SullivanCotter

Share

While many health care organizations have begun to experience modest post-pandemic financial recovery, ongoing workforce challenges – high turnover, employee burnout, wage pressure and other recruitment and retention issues – are adding to cost concerns. As labor expenditure remains high, hospitals and health systems are reevaluating the size and shape of their employee populations to offset rising costs and create a more affordable and sustainable workforce architecture.

Despite only slight increases (up less than 1% from 2022) in the overall size of the workforce, year-over-year comparisons show that the cost of labor continues to rise at a much faster rate. Annual base payroll expense, which constitutes the vast majority of an organization’s labor expenditures, has gone up almost 10% from 2022 to 2023. For the average participating organization with an annual base payroll expense of over $2 billion, this has added about $200 million to the expense line.

Diving deeper into these findings – including data reported on multiple job families and demographic groupings throughout different career level stages – provides insight into how organizations can support ongoing expense management and workforce efficiency initiatives.

Assessing Workforce Cost and Structure

Although growth in the size of the workforce has slowed across all career stages – Executives, Leaders, Managers and Individual Contributors – as compared to last year, many organizations are still experiencing unsustainable wage growth when adjusted for headcount. Base payroll cost for Individual Contributors, comprising the largest career stage, has increased by 9.6% as compared to 7.2% in 2022. Executives, Leaders and Managers are seeing labor cost growth (up to 5-6%) on par with last year’s results after adjusting for changes to headcount.

“While this analysis is consistent with prevailing industry wage pressures, there are also several other factors, such as new technology, clinical innovations, investments in new services, key strategic initiatives, and more driving changes in the composition of the workforce. Organizations continue to react to an evolving labor market, and they may see new positions being created, fewer lower-paying jobs, or a change in the mix of different job levels and career stages – all of which have a profound impact on overall labor expenditure – as these factors play out,” said Tim Pang, Principal, SullivanCotter.

As hospitals and health systems rebalance the size and shape of their workforce to help address cost and efficiency concerns, many are focusing more acutely on optimizing managerial oversight and span of control. The survey results indicate that a typical reporting structure based on the median number of FTEs consists of almost 180 FTEs reporting up directly and indirectly through each individual Executive. This includes 4.3 Leaders for every Executive, 2.4 Managers for every Leader, and 15.8 Individual Contributors for every Manager. These benchmarks, however, can vary widely depending on the functional area. Targeting a wider span of control can enable a more efficient management model where less supervision is required and employees are able to work more autonomously. This can correlate with higher levels of employee engagement and satisfaction – particularly when direct patient care is involved.

Additionally, many organizations continue to review Executive, Leader, and Manager positions that do not have formal people oversight to ensure appropriate leveling and accountability and reduce redundant management layers. When analyzing the direct span of control by career stage, this year’s survey reports that more than 10% of Executives do not have any direct reports. This increases to 21.9% and 26.7% for Leaders and Managers, respectively.

“Whether due to a lack of formal leveling criteria, having too many layers of management hierarchy, or running out of room on the Individual Contributor career ladder, this practice can impact perceived equity across the organization and dilute the management and leadership structure. Creating clear job and level definitions can help move people into the right roles and ensure that their title is reflective of their intended scope of responsibility,” said James Roth, Managing Principal, SullivanCotter.

Workforce Demographics – Gender, Age and Race

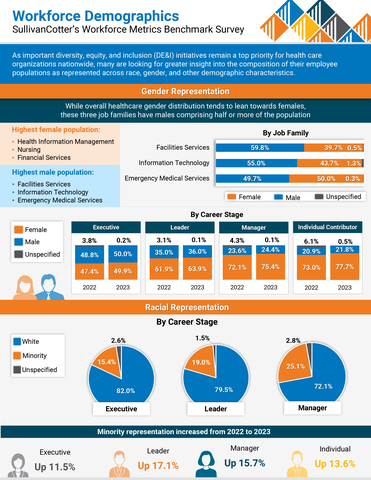

As important diversity, equity and inclusion (DE&I) initiatives remain a top priority for health care organizations nationwide, many are looking for greater insight into the diversity of their employee populations as represented across race, gender, and other demographic characteristics.

Across the 19 clinical and non-clinical job families included in the survey, gender representation is highly skewed with females comprising 73% of the workforce in 2023. This representation is highest in Financial Services, Nursing, and Health Information Management. While the three job families with the highest male populations are Facilities, Information Technology, and Emergency Medical Services, these are more evenly split and range from 49.7% - 59.8% males.

When analyzing by career stage, female representation at the Manager level is strong at 72.4%, but steadily declines to just under 50% for Executive roles – driven by large female populations in a small number of functional areas such as Nursing – indicating that fewer females are getting promoted into senior leadership roles despite comprising a majority of the workforce. Increasing female representation at this level continues to be an important area of focus for many organizations.

Generational representation also remains fairly stable but with slight shifts as Baby Boomers retire and open up new career pathways for Millennials into Director-level and management positions. Facilities Services and Health Information Management have the largest populations of Baby Boomers (both over 25%) and carry the most significant retirement risk. The positions attracting the most Millennials and Centennials – the youngest members of the workforce – include Basic Science and Research (76.5%) and Emergency Medical Services (71.6%).

Conversely, minority representation increased greatly year-over-year across all career stages – up 17.1% for Leaders, 15.7% for Managers, 13.6% for Individual Contributors, and 11.5% for Executives. When analyzed by distribution across career stage, minority representation is highest at the Manager level (25%) but then slowly decreases to 15.4% at the Executive level. Ongoing retirements over the next five to 10 years have the potential to change the demographic landscape of the health care workforce.

“We are starting to see some positive improvements in gender and minority representation across the board. To help maintain this progress and keep moving in the right direction, organizations must remain committed to supporting critical DE&I initiatives and building a more representative workforce. This includes bridging the gap in minority representation as you move up into the Executive ranks,” said Ted Chien, President and CEO, SullivanCotter.

Planning Considerations for 2024 and Beyond

Although health care organizations are cautiously optimistic about recent improvements in financial performance, many plan to reduce administrative expenses by modifying the size and shape of their workforce, centralizing key services, redefining job levels and career stages, and optimizing managerial span of control. There are several important considerations related to workforce cost and structure that organizations must be aware of as they move further into 2024 and beyond.

This includes:

- Address rising payroll expense by leveraging technology more effectively, improving key processes, and rebalancing the size and shape of the workforce to create a more sustainable and affordable model moving forward.

- Focus on capturing cost savings associated with the standardization and centralization of key services. The push for greater efficiency is putting internal service delivery in the spotlight and, given the somewhat fragmented operating models of non-clinical/administrative job families, it is important to understand the impact that centralization can have within functions like Human Resources, Finance, Information Technology, and more.

- Review span of control to help optimize managerial oversight and identify potential cost-saving opportunities. This includes understanding the importance of having clear job-level definitions so you can move people into the right roles as needed without diluting your management structure, creating potential inequities, or introducing redundant management layers.

- Succeed in health equity by committing to critical DE&I initiatives. Minority representation has increased across all career-level categories. Optimizing the workplace so that all employees can thrive is imperative to continued business success. It requires ongoing consideration to help avoid workforce stagnation to ensure progress.

SullivanCotter’s 2023 Workforce Metrics Benchmark Survey includes critical benchmarking data across clinical and non-clinical job families, six career-level categories, and important demographic groupings to provide insight into the following metrics:

- SIZE: Number of FTE headcount

- SHAPE: Career stage distribution of FTE headcount

- COST: Annualized base payroll expense of FTE headcount

- DEMOGRAPHICS: Gender, racial and generational representation

- OVERSIGHT: Management direct span of control

For more information on SullivanCotter’s surveys, please visit our website at www.sullivancotter.com, or contact us via email or by phone at 888.739.7039.

About SullivanCotter

SullivanCotter partners with health care and other not-for-profit organizations to understand what drives performance and improve outcomes through the development and implementation of integrated workforce strategies. Using our time-tested methodologies and industry-leading research and information, we provide data-driven insights, expertise, and data products to help organizations align business strategy and performance objectives – enabling our clients to deliver on their mission, vision and values.

Note to media: Additional data and interviews are available on request.

Contacts

Becky Lorentz

SullivanCotter

beckylorentz@sullivancotter.com

314.414.3719

Jenni Bowring

Padilla

jenni.bowring@padillaco.com

651.226.3858