VantageScore CreditGauge™ March 2026: Credit Conditions Improve as Consumers Pull Back on Borrowing and Reduce Card Balances

VantageScore CreditGauge™ March 2026: Credit Conditions Improve as Consumers Pull Back on Borrowing and Reduce Card Balances

- Credit Card Balances Fall, Driving Lower Utilization

- Delinquencies Decline, Led by Early-Stage Improvement in Mortgages

- Younger Borrowers and Unsecured Lending Drive Credit Growth

SAN FRANCISCO--(BUSINESS WIRE)--Households are pulling back on borrowing and reducing revolving balances, leading to improvements in consumer credit conditions, according to the latest edition of CreditGauge™ from VantageScore. The average VantageScore 4.0 credit score held steady at 701, reflecting continued consumer resilience amid elevated borrowing costs and broader macroeconomic uncertainty.

“Improved credit conditions this month reflect a cautious but resilient consumer who is actively managing debt and moderating borrowing,” said Susan Fahy, EVP and Chief Digital, Data and Technology Officer at VantageScore. “The decline in credit card balances and stabilization in delinquencies point to households prioritizing balance sheet health even as economic pressures persist.”

Watch CreditGauge LIVE for additional key insights from the March 2026 edition of CreditGauge that include:

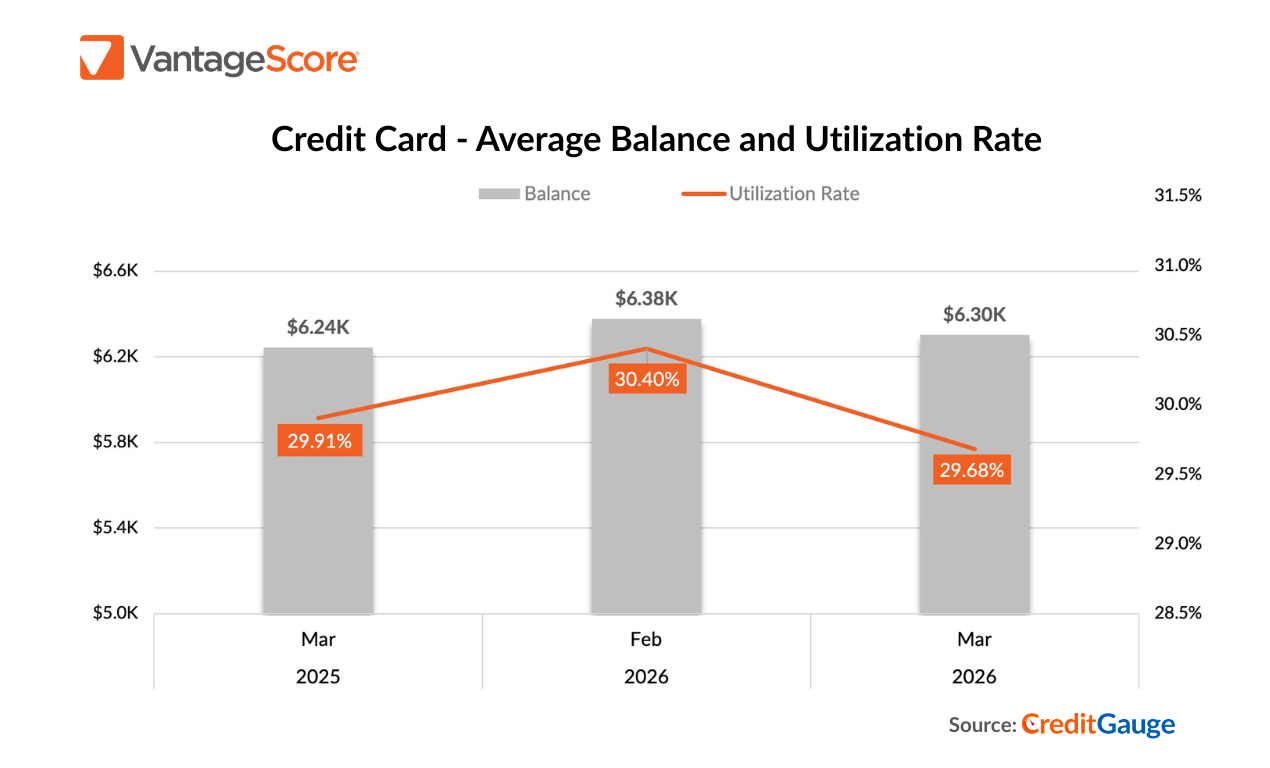

CREDIT CARD BALANCES DECLINE, DRIVING LOWER UTILIZATION: Average credit card balances declined month-over-month from February 2026, contributing to a drop in utilization to 29.68%, which fell both month-over-month (-0.72%) and year-over-year (-0.23%). The decline in revolving balances provides clearer evidence of consumer deleveraging, suggesting households are paying down debt and moderating spending, supported in part by seasonal inflows such as tax refunds.

DELINQUENCIES DECLINE, LED BY EARLY-STAGE IMPROVEMENT IN MORTGAGE: In March 2026, overall credit delinquencies declined across all stages month-over-month, indicating improvement in borrowers catching up on payments. Year-over-year delinquency improvements were driven primarily by mortgages, which decreased due to unusually high refunds with the State and Local Tax (SALT) deduction increase, greatly benefiting mortgage holders.

CONTINUED CREDIT GROWTH DRIVEN BY UNSECURED LENDING AND YOUNGER BORROWERS: Originations in March 2026 remained elevated on a year-over-year basis. Originations for unsecured lending products, including credit cards and personal loans, increased compared to March 2025. Looking generationally, year-over-year credit card originations were led by Gen Z, while year-over-year personal loan originations rose the most for Millennials, as the younger generations spearheaded unsecured lending growth.

Follow VantageScore on LinkedIn and YouTube to watch CreditGauge LIVE, a monthly video series featuring our latest insights on consumer credit data and analysis.

CreditGauge is a monthly analysis highlighting the overall health of U.S. consumer credit. To download this month’s full CreditGauge report, visit the VantageScore website.

About VantageScore CreditGauge™

CreditGauge is provided both as a monthly analysis to industry stakeholders as well as through a series of interactive tools at VantageScore.com, which also includes Inclusion360®, RiskRatio™ and MarketGain™. Stakeholders can use the tools to execute additional queries on credit metrics and compare current levels to a pre-pandemic timeframe, starting with January 2020. CreditGauge solely represents the views and analysis of VantageScore and does not necessarily reflect or represent the views of the Nationwide Consumer Reporting Agencies (NCRAs) – Equifax, Experian, and TransUnion.

About VantageScore®

VantageScore is the fastest-growing credit scoring company in the U.S., and is known for the industry’s most innovative, predictive and inclusive credit score models. In 2024, usage of VantageScore increased by 55% to hit 42 billion credit scores. More than 3,700 institutions, including nine of the top 10 U.S. banks, use VantageScore credit scores and digital tools to provide consumer credit products or generate greater insights into consumer behavior. The VantageScore 4.0 credit scoring model scores 33 million more people than traditional models. With the FHFA allowing the immediate use of VantageScore 4.0 for Fannie Mae and Freddie Mac guaranteed mortgages, the company is also ushering in a new era for mortgage lending.

VantageScore is an independent joint venture company owned by Equifax, Experian and TransUnion.

Contacts

Ola Fadahunsi | VantageScore

Email: ola@vantagescore.com

Phone: +1 (415) 740-2559