Omdia: India’s smartphone shipments fell 5% in 1Q26 amid channel caution and pricing pressures

Omdia: India’s smartphone shipments fell 5% in 1Q26 amid channel caution and pricing pressures

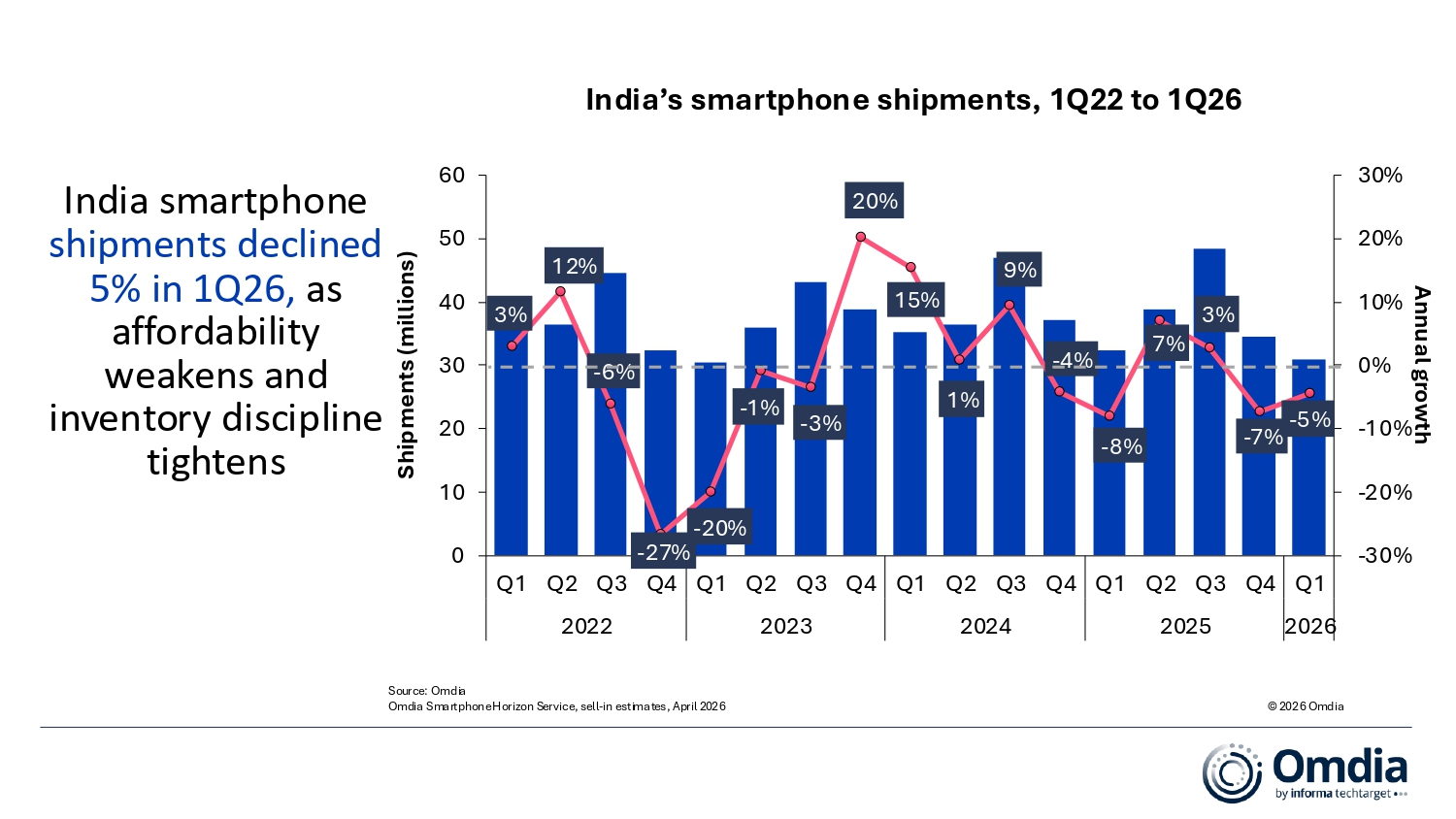

LONDON--(BUSINESS WIRE)--The latest Omdia research shows that India’s smartphone shipments fell by 5% year on year to 30.9 million units in 1Q26, reflecting seasonally weak demand compounded by cautious channel inventory strategies. Demand was pressured by macro headwinds, including rupee depreciation and rising inflation weighing on affordability and delayed consumer upgrades. Additionally, earlier front-loading ahead of expected price increases limited incremental channel intake.

“Amid growing supply-side pressures, the top vendors showed resilience as many long-tail vendors began to struggle,” said Sanyam Chaurasia, Principal Analyst at Omdia.

Share

vivo retained its leadership position in 1Q26, shipping 6.3 million smartphones to reach 20% market share. Samsung followed in second place with 5.1 million units and 16% share, supported by new launches toward the end of the quarter. OPPO (excluding realme and OnePlus) strengthened its position, securing third place with 4.7 million units and 15% share, marking the strongest growth among the top five vendors. Xiaomi and Apple rounded out the top five with shipments of 3.8 million and 2.9 million units, respectively. For Apple, 1Q26 marks its first Q1 appearance in India’s top five.

“Amid growing supply-side pressures, the top vendors showed resilience as many long-tail vendors began to struggle,” said Sanyam Chaurasia, Principal Analyst at Omdia. “vivo retained the leadership position for a seventh consecutive quarter, boosted by strong sell-out visibility and traction from the V70 series. Samsung had a late-quarter boost driven by flagship Galaxy S26 and refreshed mid-range A-series, alongside strong volumes from entry-level A07 and A17 models. OPPO emerged as the fastest-growing vendor among the top 10, driven by robust momentum across the A6x, K14 and Reno 15 series. Reno 15’s performance was supported by a wider lineup with a broader SKU mix across mid-to-premium segments. In contrast, smaller vendors struggled to absorb rising costs and sustain channel confidence, leading to sharper declines after a period of expansion, with only a few players such as Motorola, iQOO and Google showing relative resilience.”

“In 1Q26, vendors took different approaches to pricing as cost pressures intensified,” added Chaurasia. “These shifts reflected diverging priorities across pricing, margins, launch cycles and channel inventory, exposing clear strategic differences. OPPO’s flat, portfolio-wide hikes signaled a rapid margin reset, effectively re-anchoring price ladders. Xiaomi’s tiered increases reflected a profit-optimising approach, selectively incentivising sales of higher-value SKUs. In contrast, Samsung and vivo adopted phased adjustments, aiming to protect demand and ensure smoother channel absorption. This divergence was most visible in the ₹10,000–₹20,000 segment, where uniform hikes eroded affordability. At the same time, overlapping old and new inventory made channel execution a key differentiator. As 2Q26 began with further price increases, the market is shifting from a tactical adjustment to a structural reset, where balancing margins and demand will define vendor performance.”

“Looking ahead, the Indian smartphone market is facing severe downside risk in 2026 with shipments forecast to decline by double digits. Price increases have accelerated into 2Q26, with entry-level devices already seeing steep increases of 18–20% as sustained memory inflation has forced a reset of price points. At the same time, macro headwinds will constrain discretionary spending. In this environment, vendors must balance margin recovery with demand sensitivity, while channels tighten inventory alignment to avoid disruption. Upgrade cycles are set to elongate as consumers delay purchases while entry-level demand increasingly shifts toward repairs, second-hand devices and financing-led options.”

“Although 2026 will test vendor discipline and tactics, vendors cannot afford to wait for conditions to improve, assuming supply-side pressures are short-term. The vendors best positioned in the long-term are those that adapt their business and revenue models for the long term, rather than simply focusing on short-term survival,” concluded Chaurasia.

India’s smartphone shipments and annual growth |

|||||

Omdia Smartphone Market Pulse: 1Q26 |

|||||

Vendor |

1Q26 shipments (million) |

1Q26

|

1Q25

|

1Q25

|

Annual

|

vivo |

6.3 |

20% |

6.3 |

20% |

0% |

Samsung |

5.1 |

16% |

5.1 |

16% |

0% |

OPPO |

4.7 |

15% |

3.9 |

12% |

21% |

Xiaomi |

3.8 |

12% |

4.0 |

12% |

-6% |

Apple |

2.9 |

9% |

3.2 |

10% |

-11% |

Others |

8.2 |

27% |

9.9 |

30% |

-16% |

Total |

30.9 |

100% |

32.4 |

100% |

-5% |

|

|

|

|||

Note: vivo excludes iQOO. OPPO excludes realme and OnePlus. Xiaomi estimates include sub-brand POCO. Percentages may not add up to 100% due to rounding. |

|||||

Source: Omdia Smartphone Horizon Service (sell-in shipments), April 2026 |

|||||

ABOUT OMDIA

Omdia, part of Informa TechTarget, Inc. (Nasdaq: TTGT), is a technology research and advisory group. Our deep knowledge of tech markets grounded in real conversations with industry leaders and hundreds of thousands of data points, make our market intelligence our clients’ strategic advantage. From R&D to ROI, we identify the greatest opportunities and move the industry forward.

Contacts

Fasiha Khan: fasiha.khan@omdia.com

Eric Thoo: eric.thoo@omdia.com