Griffon Corporation Sends Letter to Shareholders Highlighting Strategic and Financial Benefits of Acquisition of Hunter Fan Company

Griffon Corporation Sends Letter to Shareholders Highlighting Strategic and Financial Benefits of Acquisition of Hunter Fan Company

Hunter acquisition will be immediately accretive to earnings and cash flow, creating both immediate and long-term value for shareholders

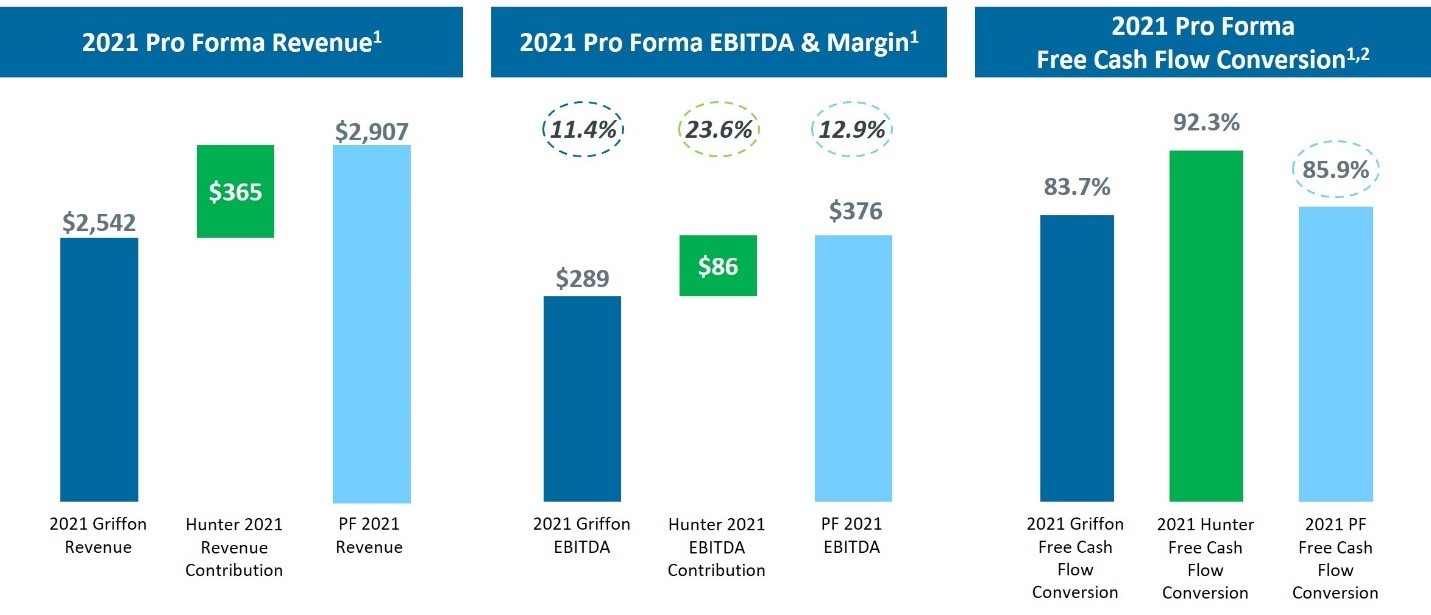

Indexed Stock Price Performance Between 20-Dec-21 and 24-Dec-21. 1. Financial profile figures based on FY2021 figures. For Griffon, FY2021 ended 9/30/2021 and includes Telephonics. For Hunter, FY2021 ended 10/29/21. See the reconciliation of Pro Forma EBITDA to Income before taxes from continuing operations or Net income, as appropriate, at the end of this release. 2. FCF Conversion defined as EBITDA less Capex divided by EBITDA. (Graphic: Business Wire)

NEW YORK--(BUSINESS WIRE)--Griffon Corporation (“Griffon” or the “Company”) (NYSE: GFF) today sent a letter to shareholders highlighting the strategic and financial benefits of its proposed acquisition of Hunter Fan Company (“Hunter”).

Griffon’s Board of Directors urges shareholders to protect the future of the Company and the value of their investment by voting the WHITE proxy card today “FOR” all four of the Company’s highly qualified director nominees. The Company's Annual Meeting of Shareholders (the "Annual Meeting") will be held on February 17, 2022 at 10:00 a.m., ET at the offices of Dechert LLP, located at 1095 Avenue of the Americas, New York, NY 10036. Shareholders of record as of close of business on December 28, 2021 will be entitled to vote at the meeting.

The proxy statement and other important information related to the Annual Meeting can be found at ir.griffon.com.

The full text of the letter follows:

January 10, 2022

Dear Fellow Shareholder,

Ahead of our 2022 Annual Meeting of Shareholders, we wanted to provide you with some additional information about our proposed acquisition of Hunter. We entered 2022 from a position of strength and are aggressively moving forward with our previously announced repositioning strategy with the next step being the closing of the Hunter acquisition.

- Hunter acquisition will create both immediate and long-term value for shareholders; the transaction will be immediately accretive to earnings and cash flow

- Hunter acquisition has already received strong support from investment and financial community

- Griffon urges all shareholders to vote "FOR" the 4 highly qualified Griffon directors on WHITE proxy card

We are extremely pleased with our progress in the financing markets to acquire this iconic market leader in residential ceiling, commercial, and industrial fans. Hunter has a 135-year heritage with a strong reputation for innovation and superior quality. Hunter has an impressive customer roster, with top customers including The Home Depot, Lowe’s, Menards, Costco, and Amazon. Hunter also has a direct relationship with consumers through its robust e-commerce business.

The Hunter acquisition continues our long-standing, disciplined M&A strategy. We remain enthusiastic about Griffon’s significantly improved prospects with the addition of Hunter. The acquisition meets all our criteria for a value-enhancing transaction for Griffon shareholders:

Griffon M&A Criteria

|

Hunter

|

|

Accretive to earnings |

✓ |

|

Attractive purchase price |

✓ |

|

Strengthens portfolio |

✓ |

|

Cross-selling opportunities |

✓ |

|

Ability to execute |

✓ |

|

In addition to being immediately accretive in fiscal 2022 to Griffon’s earnings per share, we expect Hunter will contribute at least $0.50 per share to Griffon’s EPS in fiscal 2023. Furthermore, the acquisition will complement our existing portfolio of iconic consumer and professional brands and allow us to further diversify our channels to market and expand our opportunities for revenue growth. We expect this deal to close before the end of January.

Hunter has several strategic and financial benefits.

Hunter has attractive end markets with steady growth and beneficial secular trends along with low cyclicality and volatility. Hunter is the leading North American brand of residential ceiling fans and has a strong track record of successful new product launches. In addition, with EBITDA margins north of 20%, the acquisition clearly improves Griffon’s EBITDA and gross margins. Finally, its committed and experienced management team has a track record of value creation and will be a valuable asset to our team.

Investors have reacted positively, as evidenced by the market’s reaction to the announcement. In the week after announcement, Griffon’s stock clearly outperformed the relevant market indices.

The acquisition also received support from the analyst community – pointing to the deal’s attractive margins, healthy growth and asset-light business model, which supports value creation. We are pleased to have received support from the investment and analyst community following our announcement. On December 21, 2021, Sidoti wrote:

“Our first impressions of the deal are positive, as Hunter adds a high-margin, innovative and asset-light business that can accelerate the CPP segment’s growth profile and ecommerce channel penetration.”

Additionally, CJS Securities wrote:

“While no synergies are contemplated in the $0.50+ accretion, the combination of the two companies is very attractive. In addition to potential cost synergies, Hunter’s integration into Griffon’s US distribution footprint, plus the upgraded systems in process under the Ames initiative could meaningfully help the brand. Additionally, Ames can learn and advance its omni-channel marketing and fulfillment from Hunter’s strong knowledge in this area.”

With a similarly positive view, Deutsche Bank wrote:

“We think the acquisition has solid strategic merits given the end-markets it serves have significant overlap with the existing businesses within CPP. There are also likely to be cost (i.e. distribution, overheads) and revenue (i.e. non-US based markets, and nascent product verticals) synergies which have not been included in the metrics provided by management. Additionally, we do not sense the management team will deviate from prioritizing debt reduction with not only expected proceeds from the likely sale of Telephonics - our estimates are up to $250mn - but also from significant free cash flow the legacy and Hunter will generate.”

Despite a positive reaction from Wall Street analysts and investors, Voss Capital LLC, an approximately $300 million hedge fund run by 34 year-old Travis Cocke, has publicly opposed the Hunter acquisition and is waging a proxy contest to replace two of Griffon’s directors. Mr. Cocke’s fund first became a shareholder of Griffon in August of 2021.

Mr. Cocke’s criticisms of the Hunter acquisition show his fundamental misunderstanding of our business and his lack of alignment with our other shareholders. Furthermore, Mr. Cocke’s criticisms of the deal are misleading and baseless. Mr. Cocke claims that the transaction poses execution risk when Griffon’s management team has a clear track record of successful M&A execution and integration. Voss also alleges that the transaction has an unattractive valuation. In reality, the Hunter acquisition is at an attractive valuation compared to current transaction multiples. Mr. Cocke claims that the acquisition poses a conflict of interest for director Kevin Sullivan. Nothing could be further from the truth as the transaction was negotiated at arm’s length, a process from which Mr. Sullivan was excluded.

We believe that Mr. Cocke’s opposition to the Hunter acquisition is driven by his short-term focus and that Voss completely ignores the strategic and financial benefits of the acquisition and the potential for value creation for shareholders. Voss disregards the positive reaction that the transaction has received from the investment and analyst community.

We are a strategic, focused buyer and builder of businesses with a proven track record of shareholder value-creation, including value-enhancing acquisitions and divestitures. Our corporate structure also allows us to act as a smart buyer, consolidating businesses that fit together and fueling their growth, while maintaining a disciplined approach to evaluating opportunities. Over the years Griffon has demonstrated this discipline and its ability to successfully integrate and improve the businesses it has acquired, from AMES in 2010, to ClosetMaid in 2017 and CornellCookson in 2018.

Not only do we create value by adding businesses, but also by selling them, returning cash to shareholders and investing in organic growth. Our management team and Board continue to drive Griffon’s evolution, creating a more streamlined, profitable portfolio, through the sale of legacy businesses like Clopay Plastics and executing on value enhancing acquisitions. The next phase of this evolution includes the review of strategic alternatives and sale process underway for our Defense Electronics business, which we announced in September 2021, and the acquisition of Hunter. We remain excited about continuing to build value for our shareholders.

A top priority of the Board of Directors is to ensure the Board is composed of directors who bring diverse viewpoints and perspectives, exhibit a variety of skills, have professional experience and a variety of backgrounds, and will continue to effectively represent the long-term interests of shareholders. As part of our plan to reach these objectives, our director slate includes a new nominee, Ms. Michelle L. Taylor. Michelle brings a broad range of industrial experience, particularly in the areas of manufacturing, supply chain management and quality, critically important areas of focus for Griffon and its businesses.

We strongly urge shareholders to vote the WHITE proxy card FOR all our highly qualified and experienced director nominees and FOR all our other proposals, including the important corporate governance enhancements recommended unanimously by the full Griffon Board of Directors.

Your vote is important! Please vote today by internet or mail. The Company's Annual Meeting of Shareholders will be held on Thursday, February 17, 2022 at 10:00 a.m., ET at the offices of Dechert LLP, located at 1095 Avenue of the Americas, New York, NY 10036. Shareholders of record as of close of business on December 28, 2021 will be entitled to vote at the meeting.

We look forward to engaging with you further as the Annual Meeting approaches and, as always, we appreciate your investment in Griffon and ask for your continued support.

Sincerely,

|

||

/s/ Henry A. Alpert

|

/s/ Thomas J. Brosig |

/s/ Jerome L. Coben |

/s/ Louis J. Grabowsky |

/s/ Rear Admiral Robert G. Harrison (USN Ret.)

|

/s/ Lacy M. Johnson |

/s/ Ronald J. Kramer |

/s/ Robert F. Mehmel |

/s/ General Victor E. Renuart (USAF Ret.)

|

/s/ James W. Sight |

/s/ Samanta Hegedus Stewart

|

/s/ Kevin F. Sullivan |

/s/ Cheryl L. Turnbull

|

/s/ William H. Waldorf |

|

The Griffon Board of Directors |

||

About Griffon Corporation

Griffon Corporation is a diversified management and holding company that conducts business through wholly-owned subsidiaries. Griffon oversees the operations of its subsidiaries, allocates resources among them and manages their capital structures. Griffon provides direction and assistance to its subsidiaries in connection with acquisition and growth opportunities as well as divestitures. In order to further diversify, Griffon also seeks out, evaluates and, when appropriate, will acquire additional businesses that offer potentially attractive returns on capital.

Griffon conducts its operations through two reportable segments:

- Consumer and Professional Products (“CPP”) conducts its operations through The AMES Companies, Inc. (“AMES”). Founded in 1774, AMES is the leading North American manufacturer and a global provider of branded consumer and professional tools and products for home storage and organization, landscaping, and enhancing outdoor lifestyles. CPP sells products globally through a portfolio of leading brands including True Temper, AMES, and ClosetMaid.

- Home and Building Product conducts its operations through Clopay Corporation (“Clopay”). Founded in 1964, Clopay is the largest manufacturer and marketer of garage doors and rolling steel doors in North America. Residential and commercial sectional garage doors are sold through professional dealers and leading home center retail chains throughout North America under the brands Clopay, Ideal, and Holmes. Rolling steel door and grille products designed for commercial, industrial, institutional, and retail use are sold under the CornellCookson brand.

Classified as a discontinued operation, Defense Electronics conducts its operations through Telephonics Corporation (“Telephonics”), founded in 1933, a globally recognized leading provider of highly sophisticated intelligence, surveillance and communications solutions for defense, aerospace and commercial customers.

For more information on Griffon and its operating subsidiaries, please see the Company’s website at www.griffon.com.

Important Additional Information Regarding Proxy Solicitation

Griffon filed its proxy statement and associated WHITE proxy card with the U.S. Securities and Exchange Commission (the “SEC”) on December 30,2021 in connection with the solicitation of proxies for Griffon’s 2022 Annual Meeting (the “Proxy Statement”). Shareholders as of the record date of December 28, 2021, are eligible to vote at the 2022 Annual Meeting. Griffon, its directors and certain of its executive officers will be participants in the solicitation of proxies from shareholders in respect of the 2022 Annual Meeting. Details concerning the nominees of Griffon’s Board of Directors for election at the 2022 Annual Meeting and information regarding the names of Griffon’s directors and executive officers and their respective interests in Griffon by security holdings or otherwise is set forth in Griffon’s Proxy Statement. BEFORE MAKING ANY VOTING DECISION, INVESTORS AND SHAREHOLDERS OF THE COMPANY ARE URGED TO READ ALL RELEVANT DOCUMENTS FILED WITH THE SEC, INCLUDING THE PROXY STATEMENT AND ACCOMPANYING WHITE PROXY CARD, AND ANY SUPPLEMENTS THERETO, BECAUSE THEY CONTAIN IMPORTANT INFORMATION. Investors and shareholders may obtain a copy of the Proxy Statement and other relevant documents filed by Griffon with the SEC free of charge from the SEC’s website, www.sec.gov, or by directing a request by mail to Griffon Corporation, Attention: Corporate Secretary, at 712 Fifth Avenue, New York, NY 10019, or by visiting the investor relations section of Griffon’s website, www.griffon.com.

Forward-looking Statements

“Safe Harbor” Statements under the Private Securities Litigation Reform Act of 1995: All statements related to, among other things, income (loss),earnings, cashflows, revenue, changes in operations, operating improvements, the effects of the Hunter Fan transaction, industries in which Griffon operates and the United States and global economies that are not historical are hereby identified as “forward-looking statements” and may be indicated by words or phrases such as “anticipates,” “supports,” “plans,” “projects,” “expects,” “believes,” “should,” “would,” “could,” “hope,” “forecast,” “management is of the opinion,” “may,” “will,” “estimates,” “intends,” “explores,” “opportunities,” the negative of these expressions, use of the future tense and similar words or phrases. Such forward-looking statements are subject to inherent risks and uncertainties that could cause actual results to differ materially from those expressed in any forward-looking statements. These risks and uncertainties include, among others: current economic conditions and uncertainties in the housing, credit and capital markets; Griffon’s ability to achieve expected savings from cost control, restructuring, integration and disposal initiatives; the ability to identify and successfully consummate, and integrate, value-adding acquisition opportunities; failure to consummate or a delay in consummating the Hunter Fun transaction; increasing competition and pricing pressures in the markets served by Griffon’s operating companies; the ability of Griffon’s operating companies to expand into new geographic and product markets, and to anticipate and meet customer demands for new products and product enhancements and innovations; reduced military spending by the government on projects for which Griffon’s Telephonics Corporation supplies products, including as a result of defense budget cuts or other government actions; the ability of the federal government to fund and conduct its operations; increases in the cost or lack of availability of raw materials such as resin, wood and steel, components or purchased finished goods, including any potential impact on costs or availability resulting from tariffs; changes in customer demand or loss of a material customer at one of Griffon’s operating companies; the potential impact of seasonal variations and uncertain weather patterns on certain of Griffon’s businesses; political events that could impact the worldwide economy; a downgrade in Griffon’s credit ratings; changes in international economic conditions including interest rate and currency exchange fluctuations; the reliance by certain of Griffon’s businesses on particular third party suppliers and manufacturers to meet customer demands; the relative mix of products and services offered by Griffon’s businesses, which impacts margins and operating efficiencies; short-term capacity constraints or prolonged excess capacity; unforeseen developments in contingencies, such as litigation, regulatory and environmental matters; unfavorable results of government agency contract audits of Telephonics Corporation; our strategy, future operations, prospects and the plans of our businesses, including the exploration of strategic alternatives for Telephonics Corporation; Griffon’s ability to adequately protect and maintain the validity of patent and other intellectual property rights; the cyclical nature of the businesses of certain of Griffon’s operating companies; and possible terrorist threats and actions and their impact on the global economy; the impact of COVID-19 on the U.S. and the global economy, including business disruptions, reductions in employment and an increase in business and operating facility failures, specifically among our customers and suppliers; Griffon’s ability to service and refinance its debt; and the impact of recent and future legislative and regulatory changes, including, without limitation, changes in tax law. Such statements reflect the views of the Company with respect to future events and are subject to these and other risks, as previously disclosed in the Company’s Securities and Exchange Commission filings. Readers are cautioned not to place undue reliance on these forward-looking statements. These forward-looking statements speak only as of the date made. Griffon undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

Griffon Adjusted EBITDA Reconciliation |

|

($ in millions) |

|

|

20211 |

|

|

Income before taxes from continuing operations |

$111 |

Acquisitions Costs |

-- |

Cost of life insurance benefits |

-- |

Secondary equity offering costs |

-- |

Special dividend ESOP charges |

-- |

Acquisition contingent consideration |

-- |

Loss from debt extinguishment |

-- |

Restructuring Charges |

21 |

Depreciation & Amortization |

52 |

Net Interest Expense |

63 |

Reported Adj. EBITDA |

$248 |

Segment Adj. EBITDA: |

|

Consumer and Professional Products |

116 |

Home and Building Products |

181 |

Defense Electronics |

20 |

Subtotal |

$317 |

Less: Defense Electronics |

(20) |

Segment Adj. EBITDA: |

$297 |

Defense Electronics |

20 |

Stock and ESOP based Compensation |

20 |

Less: Corporate Expenses (less Depreciation) |

(48) |

Pro Forma Adjustments |

-- |

Compliance Adj. EBITDA |

$289 |

Less: Capital Expenditures |

47 |

Free Cash Flow2 |

$242 |

|

|

Note: Due to rounding, numbers presented may not add up precisely to the totals provided. |

|

1Griffon’s 2021 fiscal year ended 9/30/21. |

|

2Free Cash Flow defined as Diligence Adj. EBITDA minus Capital Expenditures. |

Hunter Adjusted EBITDA Reconciliation |

|||

($ in millions) |

|

||

|

|

|

20211 |

|

|

|

|

Net Income |

$3 |

||

Interest, net |

31 |

||

Income Taxes |

5 |

||

Depreciation and Amortization |

18 |

||

EBITDA, as reported |

$57 |

||

Adjustments: |

|||

Audit to internal variances |

1 |

||

Discontinued Ops and FY19 Pro-forma Items |

0 |

||

Management Fees, Distributions, and Refinancing |

29 |

||

Non-recurring Projects |

3 |

||

CFO Transition and M&A |

0 |

||

Run-rate Pension Costs |

0 |

||

Bonus Normalization |

(0) |

||

Diligence and Other Adjustments |

(5) |

||

Total Adjustments |

$29 |

||

EBITDA, Diligence Adjusted |

$86 |

||

Less: Capital Expenditures |

7 |

||

Free Cash Flow2 |

$80 |

||

Note: Due to rounding, numbers presented may not add up precisely to the totals provided. |

|||

1Hunter's 2021 fiscal year ended 10/29/21. |

|||

2Free Cash Flow defined as Diligence Adj. EBITDA minus Capital Expenditures. |

|||

Contacts

Griffon Corporation

Brian G. Harris

ir@griffon.com

SVP & Chief Financial Officer

(212) 957-5000

Media

Gladstone Place Partners

Lauren Odell / Patricia Figueroa

Griffon@gladstoneplace.com

212-230-5930

Investors

MacKenzie Partners

Dan Burch / Jeanne Carr

dburch@mackenziepartners.com

jcarr@mackenziepartners.com

1 800-322-2885