Bradley L. Radoff Sends Letter to the Board of Directors of Newpark Resources Regarding the Need to Separate the Company’s Disparate Businesses

Bradley L. Radoff Sends Letter to the Board of Directors of Newpark Resources Regarding the Need to Separate the Company’s Disparate Businesses

HOUSTON--(BUSINESS WIRE)--Bradley L. Radoff, who together with his affiliates holds approximately 4.9% of the outstanding common shares of Newpark Resources, Inc. (NYSE: NR) (the "Company"), today sent the below letter to the Company’s Board of Directors.

November 23, 2021

Newpark Resources, Inc.

9320 Lakeside Boulevard, Suite 100

The Woodlands, Texas 77381

Attention: Board of Directors

Dear Members of the Board of Directors:

As you know, I am one of Newpark Resources, Inc.’s (“Newpark” or the “Company”) top five largest shareholders. I appreciate that several of you recently took time to meet with me following my previous calls with management. I left our meeting believing that we are closely aligned when it comes to wanting Newpark to evolve into a more focused, streamlined business that produces enhanced value for shareholders and stakeholders. With that said, I also walked away with the impression that the Board of Directors (the “Board”) does not yet share my sense of urgency.

I believe Newpark will remain significantly undervalued for as long as the market believes the Company will continue to house the Industrial Solutions and Fluid Systems segments under one roof. The Company’s own disclosures and investor presentations highlight that the Industrial Solutions segment is a high-margin business on a growth trajectory, while the Fluid Systems segment is an unprofitable business operating at the opposite end of the energy transition spectrum. As previously noted, this outdated structure is increasingly problematic for several reasons, including:

- The two segments possess no meaningful synergies;

- The two segments appeal to two distinctly different investor bases;

- The analyst community and relevant databases categorize Newpark as a legacy oilfield service business;

- Continuing to pair the two segments undermines Newpark’s ability to have a credible environmental, social and governance story, and;

- Continuing to pair the two segments is encouraging Newpark to incur significant overhead (although the Fluid Systems segment produces significant revenue, it has no profitability or perceived value – resulting in the Company operating as a high-overhead conglomerate instead of a focused operating business).

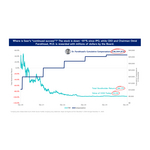

While I understand the Board may want to move at a deliberate pace, the market is sending Newpark a loud and clear message about the need to evolve more quickly. I see no valid reason for ignoring this message after a five-year period in which the Company’s share price has declined approximately 65%. I believe 100% upside value relative to the current share price could be unlocked by splitting the businesses. I see additional significant upside value potential as the Industrial Solutions business continues to benefit from its strong product offering and secular growth tailwinds.

Rather than continuing to oversee an unjustifiable structure that is punishing shareholders, the Board should publicly commit to splitting up the Company right away. The Board has a tremendous opportunity in front of it that it should want to promptly embrace. If the Board publicly commits to separating the businesses, this can allow for the creation of focused businesses that yield significant long-term benefits for Newpark’s shareholders, employees, customers and other societal stakeholders. Notably, the Industrial Solutions segment can be the foundation of a world-class infrastructure services business with the potential to be a market leader and trade at a significant premium.

Thank you for your ongoing engagement. While I welcome the ongoing dialogue with you, I hope your next communication pertaining to my suggestions is a public commitment that all of my fellow shareholders can assess.

Sincerely,

Bradley L. Radoff

Contacts

Fondren Management, LP

Greg Lempel

greg@fondrenlp.com