Tarsadia Capital Believes Proposed Acquisition of Extended Stay America by Blackstone and Starwood Severely Undervalues STAY and Is Opportunistically Timed

Tarsadia Capital Believes Proposed Acquisition of Extended Stay America by Blackstone and Starwood Severely Undervalues STAY and Is Opportunistically Timed

Tarsadia Had Privately Nominated Three Independent, World-Class Director Candidates for Election to Company’s Underqualified Board

Tarsadia Opposes Transaction and Sends Letter to Extended Stay America Shareholders

NEW YORK--(BUSINESS WIRE)--Tarsadia Capital, LLC, together with certain of its affiliates and the funds it manages (“Tarsadia” or “we”), is one of the largest shareholders of Extended Stay America, Inc. (NYSE: STAY) (“ESA” or the “Company”), beneficially owning an aggregate of approximately 3.9% of ESA’s outstanding shares. Tarsadia and various of its affiliates have been investors in the hospitality and lodging industry for over four decades.

Tarsadia believes the Company’s proposed sale to Blackstone Real Estate Partners (“Blackstone”) and Starwood Capital Group (“Starwood”) is not in the best interests of ESA shareholders for two primary reasons: first, because it undervalues the Company and, second, because it comes just as ESA and the entire lodging industry emerges from the COVID-19 pandemic to embark on a significant, multi-year recovery in RevPAR and earnings. Tarsadia will not vote in favor of the transaction.

Before the proposed sale was announced, Tarsadia nominated three, independent, world-class hospitality executives to the ESA Board of Directors to help ensure the Company was pursuing the right strategic path.

Today, Tarsadia sent a letter to its fellow ESA shareholders in which it demonstrates that the proposed transaction – in which public shareholders would receive only $19.50 per paired share – is an opportunistically timed purchase by private equity buyers at a valuation that is far below the Company’s intrinsic value. Tarsadia believes that a sale of the Company now would deprive public shareholders of participation in the recovery of the lodging sector and imminent asset sales worth hundreds of millions of dollars.

The full text of Tarsadia’s letter is below.

March 22, 2021

Dear Fellow Shareholders:

Tarsadia Capital, LLC, together with certain of its affiliates and the funds it manages (“Tarsadia,” “our,” “us” or “we”), beneficially own an aggregate of approximately 3.9% of the shares of Extended Stay America, Inc. (“ESA” or the “Company”), making us one of ESA’s largest shareholders. We are the public investment management arm of a family office that has significant expertise owning, operating and investing in the lodging and hospitality sector.

ESA has been a big disappointment to public market investors since its IPO. In its seven years as a public Company, it has cycled through executive teams, operational strategies, and strategic reviews, all while significantly underperforming peers.

We do not believe the Company’s underperformance was inevitable or that it must persist. ESA owns some of the best hospitality assets in the country and should generate excellent shareholder returns from those assets.

That is why, several months ago, we began to engage with the Company and sought to help it optimize its strategy, corporate structure and ESA Board of Directors (the “Board”). Weeks ago, we nominated three, independent, world-class hospitality executives to the Board to help ESA fulfill its potential. These nominees are:

- Stephen Joyce – Former CEO of Choice Hotels (NYSE: CHH) and Dine Brands Global, Inc. (NYSE: DIN). Board member at Hospitality Investors Trust, Inc. (OTC: HPIT) and RE/MAX Holdings, Inc. (NYSE: RMAX).

- Ross Bierkan – Former CEO of RLJ Lodging Trust (NYSE: RLJ), where he oversaw over $8 billion of real estate acquisitions, and $2.5 billion of dispositions. Currently Principal of Wellfleet Equity, a private investment company with a hospitality industry focus.

- Michael Leven – Former President and Chief Operating Officer of Las Vegas Sands (NYSE: LVS). Member of the Board of Trustees of Hersha Hospitality Trust (NYSE: HT). Formerly President and Chief Operating Officer of Holiday Inn Worldwide.

The Announced Transaction is Not in the Interests of Shareholders.

We are gravely disappointed to see the Board agreed to sell the Company for a grossly inadequate price. We have every confidence that ESA, with the right leadership and Board, can generate much better value for shareholders than the $19.50 per share the Board accepted after its seemingly hasty negotiations with Blackstone Real Estate Partners (“Blackstone”) and Starwood Capital Group (“Starwood”). The $6 billion transaction involving more than 560 properties appears to have come together in less than five weeks, right as the economy begins a recovery.

The timing and pricing of this transaction are wrong. This deal is not in the best interests of ESA’s public shareholders. We, therefore, oppose the deal.

The timing is wrong.

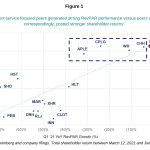

ESA and the lodging sector more generally are at an inflection point. Hotel companies are just emerging from the worst downturn the industry has ever seen. The tailwinds of COVID vaccine distribution, pent-up travel demand and fiscal stimulus create a massively positive backdrop for lodging companies over the next several years. April 2021 will mark the one-year anniversary since the U.S. hotel RevPAR troughed at a year-over-year decline of over 80%.

This year will be the first year of a new lodging cycle, which has historically been the most attractive time to invest in lodging stocks. In the prior 2001 and 2009 lodging recessions, after the one-year anniversary of a RevPAR trough, the three-year average lodging stock total shareholder returns were +124% (2002 to 2005) and +59% (2010 to 2013).1 With a clear economic and earnings recovery trajectory, the Company’s stock is highly likely to participate in this cyclical updraft.

The opportunities at ESA go beyond cyclical forces. With capital returns from imminent asset sales and an under-levered balance sheet compared to industry peers, ESA is ideally positioned for above-market returns. In fact, we believe there are operational, structural and capital structure adjustments that could be made that would produce materially stronger results and create significant value for shareholders in the years to come.

Less than two weeks ago, for example, the Company indicated that it had assets under contract for sale at highly accretive multiples that would generate hundreds of millions of dollars of potential capital returns. The current policy and macroeconomic backdrop create a unique opportunity for the Company to sell a significant portion of the portfolio for multi-family and affordable housing conversions at a material premium to the $92,000/key price in the Blackstone and Starwood transaction. We also believe there is a meaningful opportunity to increase unit growth and profits through more aggressive franchising efforts. Furthermore, with an under-levered balance sheet, there is an opportunity to further increase capital returns to shareholders.

In short, selling now, before the cyclical upturn and before these operating, asset sale, balance sheet optimization and capital return opportunities are realized, is a massive mistake unless the buyer is paying a significant premium to account for these inherent opportunities.

Our alternative Board candidates have confidence that significant value could be created for public shareholders at ESA and we are prepared to help the Company achieve its strategic plan and extend its horizons through these operating and strategic opportunities. The incumbent Board, however, has chosen to throw in the towel – first refusing to actively engage with our ideas and our exceptional candidates and now, worse, selling at the beginning of a cyclical recovery.

Perhaps this disappointing transaction is the result of the incumbent Board attempting to sidestep accountability for the Company’s many years of underperformance right before the start of a proxy contest. Regardless, one thing is clear: with clear line of sight to greater results and a bright future, selling for a paltry price is not the best outcome for shareholders.

The price is wrong.

The sale to Blackstone and Starwood, if completed, would conclude ESA’s more than seven years as a public Company at a price below its original IPO price. Over this period, the Company has underperformed for shareholders on an absolute basis, but also compared to all relevant peer groups and indexes.

The proposed transaction price of $19.50 per share values ESA at a 11.6x 2022E EBITDA, a 37% discount to the current average trading multiple of its lodging peers (18.5x) and a 24% discount to the next lowest peer, Apple Hospitality REIT.2 On a forward EBITDA basis, the proposed price is the lowest transaction multiple in the U.S. lodging space in more than five years.3

Given the strategic value of ESA to Blackstone and Starwood – both of whom own assets that can be readily combined with ESA’s lodging assets – and the potential cost savings and revenue synergies, a transaction with these parties should come in-line or at a premium to multiples observed in the lodging M&A market, not at a material discount.

Better Alternatives Exist.

The Company has plenty of opportunities to succeed for shareholders. Our Board candidates are enthusiastic about helping the Company create value as an independent public company. We are convinced the value of ESA on a standalone basis far exceeds $19.50 per share.

We believe shareholders should oppose the transaction, insist on a new Board and reap the full benefits of a better plan and better business structure.

There is, in our view, no reason to sell now and no reason to sell at this price.

We look forward to communicating further with our fellow shareholders about the best path to generate maximum value for shareholders at ESA.

Sincerely,

Tarsadia Capital

About Tarsadia Capital, LLC

Tarsadia Capital, LLC is the New York-based investment management company of a family office. Tarsadia Capital, LLC has a flexible and long-duration investment mandate that focuses on equities and commodities globally. Our investment process employs deep fundamental research on secular inflections to identify and build conviction around asymmetric risk/reward opportunities that will play out over multi-year time horizons.

Disclaimer

This material does not constitute an offer to sell or a solicitation of an offer to buy any of the securities described herein in any state to any person. In addition, the discussions and opinions in this letter and the material contained herein are for general information only, and are not intended to provide investment advice. All statements contained in this letter that are not clearly historical in nature or that necessarily depend on future events are “forward-looking statements,” which are not guarantees of future performance or results, and the words “anticipate,” “believe,” “expect,” “potential,” “could,” “opportunity,” “estimate,” and similar expressions are generally intended to identify forward-looking statements.

The projected results and statements contained in this letter and the material contained herein that are not historical facts are based on current expectations, speak only as of the date of this letter and involve risks that may cause the actual results to be materially different. Certain information included in this material is based on data obtained from sources considered to be reliable. No representation is made with respect to the accuracy or completeness of such data, and any analyses provided to assist the recipient of this material in evaluating the matters described herein may be based on subjective assessments and assumptions and may use one among alternative methodologies that produce different results. Accordingly, any analyses should also not be viewed as factual and also should not be relied upon as an accurate prediction of future results.

All figures are unaudited estimates and subject to revision without notice. Tarsadia Capital disclaims any obligation to update the information herein and reserves the right to change any of its opinions expressed herein at any time as it deems appropriate. Past performance is not indicative of future results. Tarsadia Capital has neither sought nor obtained the consent from any third party to use any statements or information contained herein that have been obtained or derived from statements made or published by such third parties. Except as otherwise expressly stated herein, any such statements or information should not be viewed as indicating the support of such third parties for the views expressed herein.

_____________________________

1 Source: Bloomberg. Returns from September 20, 2002 through September 20, 2005 are an average of MAR, HST, RHP and CHH. Returns from March 14, 2010 to March 14, 2013 are an average of MAR, HST, RHP, CHH and SHO.

2 Source: Bloomberg as of March 15, 2021. Lodging peers include: APLE, CHH, DRH, HLT, HST, INN, MAR, PEB, PK, RHP, SHO, WH, XHR. The same massive discount pertains if one looks at expected recovery-level EBITDA for ESA and its peers by analyzing current enterprise value compared to 2019 EBITDA.

3 Source: Belmond Proxy statement filed on January 8, 2019 and public filings. Other transactions and multiples include: Strategic Hotels-Blackstone (16.5x); Strategic Hotels-Anbang (17.8x), Starwood Hotels-Marriott (13.3x), Morgans Hotel Group-SBE Ent. Group (17.6x), Hyatt Portfolio-Host Hotels (16.0x), LaSalle Hotel Properties-Pebblebrook Hotel Trust (16.2x), Two Roads Hospitality-Hyatt Hotels (20.1x), Belmond Ltd-LVMH (17.7x).

Contacts

Media Contact

Sloane & Company

Dan Zacchei / Joe Germani

dzacchei@sloanepr.com / jgermani@sloanepr.com

Investor Contact

Tarsadia Capital, LLC

Michael Ching / Ravi Bellur / Vikram Patel

michaelc@tarsadiacapital.com / ravib@tarsadiacapital.com / vikramp@tarsadiacapital.com