Omdia: Middle East Smartphone Market up 23% in 3Q25; Supply Issues to Rein in 2026 Growth to 1%

Omdia: Middle East Smartphone Market up 23% in 3Q25; Supply Issues to Rein in 2026 Growth to 1%

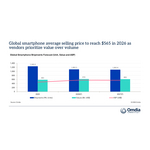

LONDON--(BUSINESS WIRE)--New data from Omdia reveals a strong rebound in the Middle East smartphone market (excluding Turkey) in 3Q25, with shipments rising 23% year on year to 15.1 million units. The growth was primarily driven by rising demand in key mass-market segments, where consumers are upgrading from older or entry-level devices to more capable mid-tier 4G and affordable 5G smartphones. Vendors capitalized on this momentum by focusing on value-for-money portfolios and expanding their presence in emerging markets, where affordable 4G models continue to drive high-volume adoption.

“Although the region posted strong growth, ASP softness persisted as vendors prioritized volume through expanded entry-level portfolios,” said Manish Pravinkumar, Principal Analyst at Omdia.

Share

Market performance varied across the region. Saudi Arabia, the Middle East’s largest market, recorded a modest 2% decline as prolonged summer holidays softened retail activity and delayed upgrade cycles. The UAE grew 13% year on year, supported by strong promotional activity from major retailers such as Sharaf DG, Carrefour and Emax, along with seasonal demand from Dubai Summer Surprises and a series of high-profile product launches. Iraq and the Rest of Middle East maintained strong momentum with 41% and 70% growth respectively. This was due to intensified vendor activity, stronger channel incentives and improved coordination with distributors, alongside steady replacement demand in entry-level segments.

“Although the region posted strong growth, ASP softness persisted as vendors prioritized volume through expanded entry-level portfolios,” said Manish Pravinkumar, Principal Analyst at Omdia. “Samsung retained its leadership with 22% growth, supported by the early push behind its Galaxy A17 4G/5G lineup and sustained contributions from high-volume A-series models. TRANSSION recorded a notable 47% rebound, driven by TECNO’s expanding footprint in lower-ASP markets and its strong resonance among Asian and African expatriate communities across key Gulf hubs.”

“Xiaomi delivered 35% growth as it restructured its channel relationships and deepened regional investments. The opening of its first flagship store at Dubai’s Ibn Battuta Mall marks its increasing shift toward direct-to-consumer engagement. HONOR posted the highest year-on-year growth at 128%, supported by portfolio expansion, stronger operator and retail partnerships, and broader ecosystem positioning. Apple returned to double-digit growth at 14%, following six quarters of uneven performance, with early sell-through of the iPhone 17 series reinforcing its premium leadership.”

“Omdia expects the Middle East smartphone market growth to slow to a modest 1% in 2026, down from 13% in 2025, as 1H26 faces headwinds from rising component costs and supply constraints,” said Pravinkumar. “These challenges will be felt most in lower-ASP markets, where strengthening channel engagement and deploying focused incentives across mass-market tiers will be essential to maintaining momentum. Meanwhile, the mid-to-premium segment is expected to remain resilient, with upgrade activity led by Apple and Samsung, supported by stronger ecosystem value and brand stickiness. To sustain demand, channels will need to expand financing options, trade-in schemes and targeted promotions, while vendors who balance cost discipline, portfolio optimization and service-led differentiation will be best positioned to capture the region’s gradual return to growth.”

Middle East* smartphone shipment and annual growth |

|||||

Omdia Smartphone Market Pulse: 3Q25 |

|||||

Vendor |

3Q25 |

3Q25 |

3Q24 |

3Q24 |

Annual |

shipments |

market |

shipments |

market |

growth |

|

(million) |

share |

(million) |

share |

|

|

Samsung |

5.2 |

34% |

4.2 |

35% |

22% |

TRANSSION |

2.7 |

18% |

1.8 |

15% |

47% |

Xiaomi |

2.3 |

15% |

1.7 |

14% |

35% |

HONOR |

1.6 |

10% |

0.7 |

6% |

128% |

Apple |

1.4 |

9% |

1.2 |

10% |

14% |

Others |

1.9 |

13% |

2.5 |

21% |

-23% |

Total |

15.1 |

100% |

12.2 |

100% |

23% |

|

|||||

Note: OPPO includes OnePlus. Vivo includes iQOO. Xiaomi includes POCO |

|

||||

Percentages may not add up to 100% due to rounding. *Excluding Turkey |

|||||

Source: Omdia Smartphone Horizon Service (sell-in shipments), November 2025 |

|||||

ABOUT OMDIA

Omdia, part of Informa TechTarget, Inc. (Nasdaq: TTGT), is a technology research and advisory group. Our deep knowledge of tech markets, grounded in real conversations with industry leaders and hundreds of thousands of data points, make our market intelligence our clients’ strategic advantage. From R&D to ROI, we identify the greatest opportunities and move the industry forward.

Contacts

Fasiha Khan – fasiha.khan@omdia.com