Newsroom

Sorted by: Latest

-

CRH plc UK Regulatory Announcement: CRH Completes Cancellation of Preference Shares

NEW YORK--(BUSINESS WIRE)-- Further to the announcement made on March 13, 2026, CRH (NYSE: CRH) today announces that the separate schemes of arrangement to cancel the Company’s 5% preference shares and 7% preference shares became effective today, June 25, 2026, and that the preference shares have been cancelled. Cancellation of the admission of the 5% preference shares to trading on Euronext Growth Dublin is expected to occur with effect from 7:00 a.m. (BST) tomorrow, Friday June 26, 2026. Abo...

-

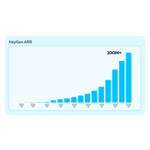

HeyGen Doubles to $200M ARR in Eight Months on the Rise of Identity-First AI Video

LOS ANGELES--(BUSINESS WIRE)--HeyGen, the identity-first AI video platform, today announced it has surpassed $200 million in annual recurring revenue, doubling in eight months. The milestone reflects a rapid shift in how individuals, small businesses, and enterprises adopt AI video: as a scalable layer for human communication across languages, formats, and audiences. HeyGen's community now spans more than 30 million users in 196 countries and 175+ languages & dialects, from solopreneurs cre...

-

HealthierHere, Ready Computing, and Unite Us Announce the Connect2 Impact Alliance to Improve Care Coordination Across WA State and Beyond

SEATTLE--(BUSINESS WIRE)--HealthierHere today launched the Connect2 Impact Alliance, a new partnership with Ready Computing and Unite Us designed to streamline how community organizations, health and social care providers, and government agencies collaborate to improve community well-being. Built with and for local communities and already used around Washington State, Connect2 Technology enables partners to securely share information, coordinate referrals, and support whole-person care. The new...

-

CRH Completes Cancellation of Preference Shares

NEW YORK--(BUSINESS WIRE)--Further to the announcement made on March 13, 2026, CRH (NYSE: CRH) today announces that the separate schemes of arrangement to cancel the Company’s 5% preference shares and 7% preference shares became effective today, June 25, 2026, and that the preference shares have been cancelled. Cancellation of the admission of the 5% preference shares to trading on Euronext Growth Dublin is expected to occur with effect from 7:00 a.m. (BST) tomorrow, Friday June 26, 2026. About...

-

First Trust Global Funds PLC UK Regulatory Announcement: Net Asset Value(s)

LONDON--(BUSINESS WIRE)-- Funds Date TIDM ISIN Code Shares in Issue Currency Net Asset Value NAV/per Share First Trust US Equity Income UCITS ETF 24.06.2026 UINC IE00BZBW4Z27 10,227,676.00 USD 402,333,756.66 39.338 ...

-

Deadline Alert: Nano-X Imaging Ltd. (NNOX) Shareholders Who Lost Money Urged to Contact Glancy Prongay Wolke & Rotter LLP About Securities Fraud Lawsuit

LOS ANGELES--(BUSINESS WIRE)--Glancy Prongay Wolke & Rotter LLP reminds investors of the upcoming August 11, 2026 deadline to file a lead plaintiff motion in the class action filed on behalf of investors who purchased or otherwise acquired Nano-X Imaging Ltd. (“Nano-X” or the “Company”) (NASDAQ: NNOX) securities between March 31, 2025 and April 17, 2026, inclusive (the “Class Period”).IF YOU SUFFERED A LOSS ON YOUR NANO-X INVESTMENTS, CLICK HERE TO INQUIRE ABOUT POTENTIALLY PURSUING CLAIMS T...

-

Zenlayer Named Digital Realty APAC Partner of the Year 2025

LOS ANGELES--(BUSINESS WIRE)--The distributed cloud for AI named Digital Realty’s APAC Partner of the Year for a second year for its leadership in AI infrastructure delivery....

-

T-Mobile to Host Q2 2026 Earnings Call on July 23, 2026

BELLEVUE, Wash.--(BUSINESS WIRE)--T-Mobile US, Inc. (NASDAQ: TMUS) looks forward to discussing second quarter 2026 financial and operational results on Thursday, July 23, 2026, at 7:30 a.m. Eastern Time (ET). The call will be accessible via dial-in with pre-registration as well as a webcast link on the Company’s Investor Relations website at https://investor.t-mobile.com. The earnings release, Investor Factbook, and other related materials will be available at approximately 6:30 a.m. ET on Thur...

-

Tomo is the AI Champion Helping People Bet on Themselves, Emerging from Stealth with $5 Million

SAN FRANCISCO--(BUSINESS WIRE)--Tomo, the personal AI champion that lives in your text messages, today announced a $5 million seed round led by Bain Capital Ventures (BCV), with participation from Accel, Align Fund, Basis Set, Conviction and Pear VC, along with angel investors. The funding will be used to grow the team and expand its recently launched companion app. Tomo is deceptively simple: it's a phone number you text. It learns who you want to become, remembers what matters to you and help...

-

Deadline Approaching: Embecta Corp. (EMBC) Shareholders Who Lost Money Urged To Contact Law Offices of Howard G. Smith

BENSALEM, Pa.--(BUSINESS WIRE)--Law Offices of Howard G. Smith reminds investors of the upcoming August 17, 2026 deadline to file a lead plaintiff motion in the case filed on behalf of investors who purchased Embecta Corp. (“Embecta” or the “Company”) (NASDAQ: EMBC) common stock between November 25, 2025 and May 4, 2026, inclusive (the “Class Period”).IF YOU ARE AN INVESTOR WHO SUFFERED A LOSS IN EMBECTA CORP. (EMBC), CONTACT THE LAW OFFICES OF HOWARD G. SMITH TO PARTICIPATE IN THE ONGOING SECUR...