Newsroom

Sorted by: Latest

-

Northern Trust Appointed to Support Invesco’s New Index-Tracking Mutual Fund Range

DUBLIN--(BUSINESS WIRE)--Northern Trust (Nasdaq: NTRS) today announced it has been appointed by Invesco to provide administration, custody and depositary services for its new Irish-domiciled index tracking mutual fund range, Invesco Markets V ICAV. Invesco is a U.S. asset management company serving clients in more than 120 countries. Headquartered in Atlanta, Georgia, the firm has US$2.45 trillion in assets under management across public, private, active, and passive investments (as of 31 May 2...

-

Media Release: Financial Worries Rise and Match Health Concerns as Cost-of-Living Pressures Mount in 2026

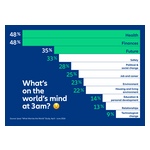

MUNICH--(BUSINESS WIRE)--Households around the world are feeling the strain of the rising cost of living, with financial pressure increasingly shaping everyday choices and long-term confidence. Finances and health are now tied as the top global worries, at 48% each, followed by concerns about the future at 35%, according to consumer surveys in 10 countries published in “The Allianz 3am Report 2026.” Financial worries, which include concerns about “rising cost of living” (71%) and “insufficient...

-

ID Logistics : Information mensuelle relative au nombre total des droits de vote et d’actions

ORGON, France--(BUSINESS WIRE)--Regulatory News: ID Logistics (Paris:IDL): Date d’arrêté des informations 30 juin 2026 Nombre total d’actions composant le capital social 6 550 826 Nombre total de droits de vote théoriques 9 813 242 Nombre total de droits de vote nets 9 801 082 Il est rappelé que les statuts d’ID Logistics Group SA comprennent une clause imposant une obligation de déclaration de franchissement de seuil complémentaire aux obligations légales. ID Logistics Group Société anonyme au...

-

ID Logistics: Information on Total Number of Voting Rights and Capital Stock Shares

ORGON, France--(BUSINESS WIRE)--Regulatory News: ID Logistics (Paris:IDL): Date June 30, 2026 Total number of capital stock shares 6 550 826 Total number of theoretical voting rights 9 813 242 Total number of effective voting rights 9 801 082 It is reminded that an obligation to disclose crossing of thresholds is included in ID Logistics Group’s bylaws in addition to the legal obligation. ID Logistics Group Société anonyme with share capital of € 3 275 413.00 Registered office : 55 chemin des E...

-

First Trust Global Funds PLC UK Regulatory Announcement: Net Asset Value(s)

LONDON--(BUSINESS WIRE)-- Funds Date TIDM ISIN Code Shares in Issue Currency Net Asset Value NAV/per Share First Trust IPOX Europe Equity Opportunities UCITS ETF 03.07.2026 IPXE.IM IE00BFD26097 50,002.00 EUR 1,315,875.27 26.316 ...

-

First Trust Global Funds PLC UK Regulatory Announcement: Net Asset Value(s)

LONDON--(BUSINESS WIRE)-- Funds Date TIDM ISIN Code Shares in Issue Currency Net Asset Value NAV/per Share First Trust Cloud Computing UCITS ETF 03.07.2026 CPQ IE00BFD2H405 6,750,002.00 USD 382,731,538.97 56.701 ...

-

First Trust Global Funds PLC UK Regulatory Announcement: Net Asset Value(s)

LONDON--(BUSINESS WIRE)-- Funds Date TIDM ISIN Code Shares in Issue Currency Net Asset Value NAV/per Share First Trust Dow Jones Internet UCITS ETF 03.07.2026 FDNU IE00BG0SSC32 1,200,002.00 USD 44,246,446.23 36.872 ...

-

Samenvatting: Ampowr en het Indonesische Ministerie van Dorpen ondertekenen een overeenkomst om gemeenschappen zonder betrouwbare stroomvoorziening aan elektriciteit te helpen

JAKARTA, Indonesië--(BUSINESS WIRE)--Ampowr heeft een intentieverklaring ondertekend met het Indonesische Ministerie van Dorpen en Ontwikkeling van Achtergestelde Regio’s (Kemendes PDT) voor het leveren van betrouwbare, schone elektriciteit aan dorpen met weinig of geen stroomvoorziening. De overeenkomst werd in Jakarta ondertekend door secretaris-generaal Taufik Madjid en de Indonesische dochteronderneming van Ampowr, PT Ampowr IES Indonesia. Het contract bouwt voort op de bestaande verkoopact...

-

Ampowr et le ministère indonésien des Villages signent un protocole d’entente visant à électrifier les collectivités dépourvues d’un approvisionnement électrique fiable

JAKARTA, Indonésie--(BUSINESS WIRE)--Ampowr a signé un protocole d’entente avec le ministère indonésien des Villages et du Développement des régions défavorisées (Kemendes PDT) afin d’apporter une électricité fiable et propre aux villages peu ou pas alimentés en électricité. L’entente a été signée à Jakarta par le secrétaire général Taufik Madjid et la filiale indonésienne d’Ampowr, PT Ampowr IES Indonesia, s’appuyant sur la présence commerciale existante de l’entreprise dans la ville. Selon le...

-

First Trust Global Funds PLC UK Regulatory Announcement: Net Asset Value(s)

LONDON--(BUSINESS WIRE)-- Funds Date TIDM ISIN Code Shares in Issue Currency Net Asset Value NAV/per Share First Trust Nasdaq Cybersecurity UCITS ETF 03.07.2026 NQCYBREN IE00BF16M727 27,148,343.00 USD 1,530,725,117.81 56.384 ...