Newsroom

Sorted by: Latest

-

YolTech Therapeutics Receives FDA Clearance to Initiate Phase 2/3 Study of In Vivo Gene-Editing Therapy YOLT-202 in Alpha-1 Antitrypsin Deficiency (AATD)

SHANGHAI--(BUSINESS WIRE)--YolTech Therapeutics, a late clinical-stage biotechnology company developing in vivo gene-editing therapies, today announced that the U.S. Food and Drug Administration (FDA) has approved the Investigational New Drug (IND) application for YOLT-202, the company’s investigational in vivo base-editing therapy for the treatment of Alpha-1 Antitrypsin Deficiency (AATD). The FDA approval enables the initiation of an open-label, single-dose expansion Phase 2/3 clinical study...

-

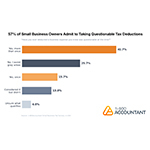

1-800Accountant Survey Finds: 57% of Small Business Owners Admit Taking Questionable Tax Deductions

NEW YORK--(BUSINESS WIRE)--A 1-800Accountant survey finds 57% of small business owners admit taking questionable tax deductions, highlighting confusion around common write-offs....

-

Dream Finders Homes named the Official Home Builder of the Tampa Bay Rays and Tampa Bay Rowdies

JACKSONVILLE, Fla.--(BUSINESS WIRE)--Today, the Tampa Bay Rays and Dream Finders Homes (NYSE: DFH) announced a new multi-year partnership that begins this season. Dream Finders Homes, the 2025 National Builder of the Year, will now serve as the Official Home Builder of the Tampa Bay Rays. This partnership will feature several marketing opportunities throughout the season designed to raise Dream Finders Homes’ profile and brand recognition in the Tampa Bay region. Inclusion at fan-facing events,...

-

Mattel Presents at 2026 UBS Global Consumer and Retail Conference to Discuss Strategy and Outlook

EL SEGUNDO, Calif.--(BUSINESS WIRE)--Mattel, Inc. (NASDAQ: MAT), a leading global play and family entertainment company and owner of one of the most iconic brand portfolios in the world, participated on Thursday, March 12, 2026 in a keynote presentation at the UBS Global Consumer and Retail Conference. Chairman and Chief Executive Officer Ynon Kreiz conducted broadcast interviews with Bloomberg and CNBC adjacent to the conference. Management discussed the company’s outlook for this year and bey...

-

INVESTOR DEADLINE: Trip.com Group Limited Investors with Substantial Losses Have Opportunity to Lead Class Action Lawsuit, Robbins Geller Rudman & Dowd LLP Announces

SAN DIEGO--(BUSINESS WIRE)--The case alleges that defendants recklessly understated the regulatory risk facing Trip.com as a result of its monopolistic business activities....

-

Accord Financial finalise la vente de ses actifs de portefeuille américains

TORONTO--(BUSINESS WIRE)--Accord Financial Corp. (TSX – ACD) (« Accord » ou la « Société ») a annoncé aujourd’hui la vente de certains prêts de sa filiale américaine, Accord Financial, Inc. (« AFIU »). Comme annoncé précédemment, la Société préparait cette transaction depuis mi-décembre 2025, conformément à une lettre d’intention signée avec un acheteur établi aux États-Unis. Cette vente constitue un élément essentiel du plan stratégique annoncé précédemment par la Société, visant à céder ses a...

-

CORRECTING and REPLACING Quirch Foods Announces Leadership Transition

MIAMI--(BUSINESS WIRE)--Quirch Foods Announces Leadership Transition...

-

INVESTOR ALERT: Securities Class Action Filed Against Soleno Therapeutics, Inc. – Investors Encouraged to Contact Kirby McInerney LLP

NEW YORK--(BUSINESS WIRE)--The law firm of Kirby McInerney LLP announces that a class action lawsuit has been filed on behalf of investors who acquired Soleno Therapeutics, Inc. (“Soleno” or the “Company”) (NASDAQ:SLNO) securities during the period of March 26, 2025 through November 4, 2025, inclusive (“the Class Period”). If you suffered a loss on your Soleno investments, you have until May 5, 2026 to request lead plaintiff appointment. Courts do not consider lead plaintiff applications submit...

-

Lieff Cabraser Files Federal Personal Injury Lawsuit Against Lyft Over Sexual Assault of Female Lyft Passenger

SAN FRANCISCO--(BUSINESS WIRE)--Lieff Cabraser Files Federal Personal Injury Lawsuit Against Lyft on behalf of Sexually Assaulted Female Lyft Passenger...

-

GDC Festival of Gaming 2026 Delivers Five Days of Transformative Connection and Insight for an Industry in Transition

SAN FRANCISCO--(BUSINESS WIRE)--GDC Festival of Gaming has concluded after uniting all facets of the international games industry for 5 days of inspiration, networking, celebration....