")

")

")

")

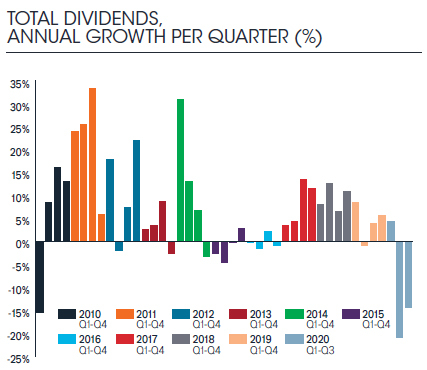

DENVER--(BUSINESS WIRE)--As the pandemic continues to reshape the economic landscape, its impact on the dividend-paying capacity of the world’s companies has become clearer. According to the latest edition of the Janus Henderson Global Dividend Index, US dividends have proven to be resilient amid recent economic headwinds. However, after remaining unchanged in Q2, the US picture deteriorated in Q3, as dividend payments fell 5.4% on a headline basis to $117.7bn, equivalent to a 3.9% underlying decline. During the quarter, one in six US companies cancelled their dividends.

Globally, total dividend payouts made by the world’s largest 1,200 firms fell by $55bn to $329.8bn in the third quarter, their lowest level since 2016. The 14.3% headline decline was equivalent to a fall of 11.4% on an underlying basis, far better than Q2’s 18.3%1 decline.

Matt Peron, Director of Research at Janus Henderson said: “Despite falling in the third quarter, US stock dividends have remained firm in the face of a global pandemic thanks in large part to share buy-backs, which have been trimmed to preserve cash. The fourth quarter will be critical for income investors, as many US companies are determining their 2021 dividends. We expect payouts in the US and worldwide to grow again next year, particularly after we get past Q1 2021.”

In April, in the midst of the greatest pandemic-induced uncertainty, Janus Henderson calculated that global dividends could fall at least 15% this year, but by as much as 35% on an underlying basis. In July the team narrowed this range to -19% to -25%. Janus Henderson is now confident that the final figure will come in towards the top end of our expectations. The best case now sees a fall of -17.5% to $1.20 trillion on an underlying basis, equivalent to a headline drop of -15.7%. Our worst case sees underlying dividends declining -20.2% to $1.16 trillion, a headline drop of -18.5%. The best case would eradicate more than three years of dividend growth, costing investors $224bn in lost income this year.

Additional Highlights From The Janus Henderson Global Dividend Index

- Globally, the worst dividend declines in Q3 came from consumer discretionary companies, down 43% in underlying terms, with car manufacturers and leisure companies making the deepest cuts. Media, aerospace and banks were also severely impacted. The most resilient sectors were classically defensive pharmaceuticals, food producers and food retailers, which all saw higher payouts on an underlying basis.

- Q3 is China’s big dividend season and payouts there were 3.3% higher year-on-year. Three quarters of Chinese companies raised payouts or held them steady. Canada and Hong Kong were among the few major countries to see dividends rise too. The weakest results came from the UK, Australia, and the Netherlands.

- Australian dividends have been among the hardest hit in the world. They fell 40.3% on an underlying basis, down to just $9.6bn, the lowest third-quarter total in at least 11 years, with cuts from the banks making a particularly large impact. UK payouts were 41.6% lower, while the cancellation of banking and brewing dividends impacted the Netherlands severely.

- Excluding Australia, dividends from Asia-Pacific ex Japan were exactly flat year-on-year, reflecting the milder impact of the pandemic both on the population and on the economy, stronger balance sheets, lower payout ratios and because many of this quarter’s payouts relate to 2019 earnings and were fixed several months ago. Hong Kong enjoyed the fastest dividend growth in the developed world in Q3, with payouts rising 9.9% on an underlying basis to $21.7bn, the second highest quarterly total on record from the territory.

Past performance is no guarantee of future results. International investing involves certain risks and increased volatility not associated with investing solely in the UK. These risks included currency fluctuations, economic or financial instability, lack of timely or reliable financial information or unfavourable political or legal developments.

Notes to editors

Janus Henderson Group (JHG) is a leading global active asset manager dedicated to helping investors achieve long-term financial goals through a broad range of investment solutions, including equities, fixed income, quantitative equities, multi-asset and alternative asset class strategies.

As of September 30, 2020, Janus Henderson had approximately US$358 billion in assets under management, more than 2,000 employees, and offices in 27 cities worldwide. Headquartered in London, the company is listed on the New York Exchange (NYSE) and the Australian Securities Exchange (ASX).

Methodology

Each year Janus Henderson analyse dividends paid by the 1,200 largest firms by market capitalisation (as at 31/12 before the start of each year). Dividends are included in the model on the date they are paid. Dividends are calculated gross, using the share count prevailing on the pay date (this is an approximation because companies in practice fix the exchange rate a little before the pay date), and converted to US$ using the prevailing exchange rate. Where a scrip dividend is offered, investors are assumed to opt 100% for cash. This will slightly overstate the cash paid out, but we believe this is the most proactive approach to treat scrip dividends. In most markets it makes no material difference, though in some, particularly European markets, the effect is greater. Spain is a particular case in point. The model takes no account of free floats since it is aiming to capture the dividend paying capacity of the world’s largest listed companies, without regard for their shareholder base. We have estimated dividends for stocks outside the top 1,200 using the average value of these payments compared to the large cap dividends over the five-year period (sourced from quoted yield data). This means they are estimated at a fixed proportion of 12.7% of total global dividends from the top 1,200, and therefore in our model grow at the same rate. This means we do not need to make unsubstantiated assumptions about the rate of growth of these smaller company dividends. All raw data was provided by Exchange Data International with analysis conducted by Janus Henderson Investors.

This press release is solely for the use of members of the media and should not be relied upon by personal investors, financial advisers or institutional investors. We may record telephone calls for our mutual protection, to improve customer service and for regulatory record keeping purposes.

Issued by Janus Henderson Investors. Janus Henderson Investors is the name under which investment products and services are provided by Janus Capital International Limited (reg no. 3594615), Henderson Global Investors Limited (reg. no. 906355), Henderson Investment Funds Limited (reg. no. 2678531), AlphaGen Capital Limited (reg. no. 962757), Henderson Equity Partners Limited (reg. no.2606646), (each registered in England and Wales at 201 Bishopsgate, London EC2M 3AE and regulated by the Financial Conduct Authority) and Henderson Management S.A. (reg no. B22848 at 2 Rue de Bitbourg, L-1273, Luxembourg and regulated by the Commission de Surveillance du Secteur Financier). Henderson Secretarial Services Limited (incorporated and registered in England and Wales, registered no. 1471624, registered office 201 Bishopsgate, London EC2M 3AE) is the name under which company secretarial services are provided. All these companies are wholly owned subsidiaries of Janus Henderson Group plc. (incorporated and registered in Jersey, registered no. 101484, with registered office at 47 Esplanade, St Helier, Jersey JE1 0BD).

[Janus Henderson, Janus, Henderson, Perkins, Intech, Alphagen, VelocityShares, Knowledge Shared, Knowledge. Shared and Knowledge Labs] are trademarks of Janus Henderson Group plc or one of its subsidiaries. © Janus Henderson Group plc.

_________________________

1 Revised upwards from -19.1% - see report for more details