Emotional Stress of Elder Fraud Outweighs Financial Impact: AICPA Survey

Emotional Stress of Elder Fraud Outweighs Financial Impact: AICPA Survey

- Phone and internet scams top the list of most common types of financial abuse or fraud targeting elderly.

- CPAs are seeing their clients victimized by many common scams at lower levels than they were in 2015.

- In the past year nearly half of CPA financial planners had a client show signs of dementia for the first time.

- Ensuring that power of attorney and health care proxies are in place top the list of most common plan components to address potential diminished capacity.

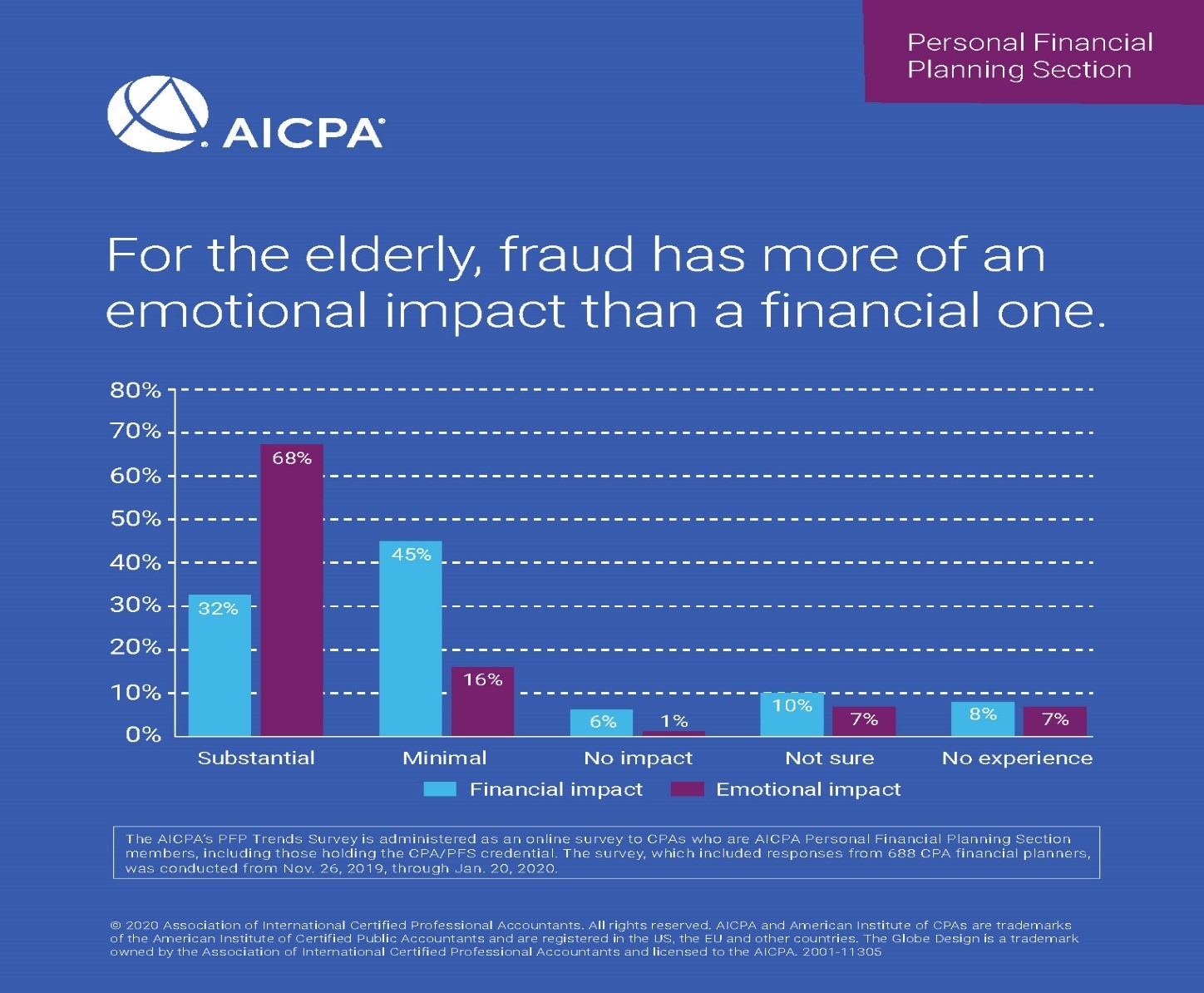

NEW YORK--(BUSINESS WIRE)--A new survey from the American Institute of CPAs (AICPA) found that falling victim to fraud is much more likely to have a substantial emotional impact (68 percent) on the elderly than a substantial financial impact (32 percent). And phone and internet scams top the list of ways financial fraud is perpetrated against the elderly. This according to the AICPAs Personal Financial Planning (PFP) Trends Survey, which includes responses from 688 CPA financial planners.

Impact of Fraud Upon the Elderly is More Emotional than Financial

CPAs have found that the stress and emotional impact of fraud outweighs the actual financial impact. By more than a 4 to 1 margin (68 percent vs. 16 percent), CPA financial planners said the emotional impact was substantial compared to minimal. Only 1 percent said it had no impact. Whereas, CPA financial planners said that the financial impact of fraud is more likely to be minimal (45 percent) than substantial (32 percent).

For the elderly, fraud has more of an emotional impact than a financial one. |

||||||||||||||||

Type of impact |

Substantial |

Minimal |

No impact |

Not Sure |

No experience |

|||||||||||

Emotional impact (stress) |

68% |

|

|

16% |

|

|

1% |

|

|

7% |

|

|

7% |

|||

Financial impact |

32% |

|

|

45% |

|

|

6% |

|

|

10% |

|

|

8% |

|||

Most Common Types of Elder Abuse or Fraud

The survey asked CPA financial planners what types of financial abuse or fraud they’ve seen perpetrated on their elderly clients, with phone or internet scams (75 percent) cited most frequently. This was followed by the inability to say ‘no’ to relatives (60 percent) and identity theft (49 percent). Additional common scams or abuse observed include support for non-disabled adult children (43 percent), credit card theft (30 percent) and being taken advantage of by an in-home caregiver (26 percent).

“Everyone is vulnerable to financial abuse and exploitation. However, the elderly are highly susceptible because companionship is an enticing allure for them. This can be due to the disintegration of the traditional nuclear family, death of spouse or friends, and the isolation that accompanies declining health,” said Susan Tillery, CPA/PFS, Chair of the AICPA’s PFP Executive Committee. “Financial exploitation of the elderly impacts much more than their finances. When someone they depend on for companionship abuses that trust, they can be emotionally distraught and withdraw from family and friends. One of the challenges specific to working with the elderly that CPA financial planners encounter is assessing their elderly client's desire to provide financial help for a family member, against their own continuing financial needs.”

Silver Lining: Overall, Scams Down Slightly From 2015

While any fraud and abuse against the elderly is concerning, the survey found that CPAs are seeing their clients victimized by many of these scams at lower levels than they were in 2015.

Fraud and abuse against the elderly is prevalent but trending downward. |

|||||||

Type of Financial Abuse or Fraud |

Percent of CPAs who have encountered each scam

|

||||||

2020 Results |

|

|

2015 Results |

||||

Phone or Internet |

75% |

|

|

79% |

|||

Inability to say ‘no’ to relatives |

60% |

|

|

72% |

|||

Identity Theft |

49% |

|

|

57% |

|||

Support for Non-disabled Adult Children |

43% |

|

|

50% |

|||

Credit Card Theft |

30% |

|

|

27% |

|||

Taken advantage of by in-home caregiver |

26% |

|

|

25% |

|||

Mistaken Charity Request for Bill |

12% |

|

|

20% |

|||

Other |

6% |

|

|

3% |

|||

Diminished Capacity Concerns Need to be Addressed

Many financial planners would agree that one of the most emotional aspects of retirement planning is the potential for diminished capacity. As Americans continue to live longer, diminished capacity issues will in all likelihood become more prevalent. In fact, the survey found that nearly half (48 percent) of all CPA financial planners had a client exhibit signs of dementia or diminished capacity for the first time in the past year alone. This underscores the need for Americans and their financial planners to understand how to address these issues together.

“As the trusted adviser to my clients, I am especially cognizant of mental capacity, and specifically with elderly clients, symptoms of the early signs of dementia,” added Tillery. “Managing cognitive decline is difficult for the client, their family and the CPA financial planner. At times such as this, it is essential to be proactive by having a plan in place to deal with the financial demands of long-term care and other medical expenses associated with diminished capacity. By having a plan in place, the family will be able to focus on quality of life and not on managing the financial need.”

Despite increased awareness about the impact of aging on cognitive function, nearly 3 in 10 (28 percent) CPA financial planners say their client’s plan to deal with diminished mental capacity in retirement on a reactionary basis, and 1 in 5 (20 percent) are ignoring the issue altogether. Only 17 percent are choosing to take steps proactively. While it is preferable to develop a plan before clients begin to exhibit signs of dementia, there are strategies CPA financial planners can take to protect a client’s assets in retirement after these issues come to light.

Proactive Plan Components to Manage the Potential of Diminished Capacity in Retirement

The survey found a vast majority (92 percent) of CPA financial planners dealt with diminished capacity in their clients by ensuring that powers of attorney and health care proxies were in place, while two-thirds (66 percent) arranged for themselves to contact their client’s other professionals and relatives. Additional measures taken include obtaining authorization to contact their client’s attorney (44 percent), moving money to a trust (37 percent), and automating their client’s annual required minimum distributions from their qualified retirement accounts (34 percent). Nearly a quarter (23 percent) had their clients move into a previously selected assisted care facility.

How CPA financial planners address dementia

|

|||

Ensure powers of attorney & health care proxies are in place |

92% |

||

Authorization to contact client’s other professionals & relatives |

66% |

||

Authorization to contact client’s attorney |

44% |

||

Money moved to a trust |

37% |

||

Automate yearly RMDs |

34% |

||

Moving to a previously selected assisted care facility |

23% |

||

Other |

5% |

||

Freeze the client’s accounts |

4% |

||

“As people are living longer and issues such as diminished capacity and elder financial abuse are becoming more prevalent, there is great demand for comprehensive financial planning,” said Andrea Millar, CPA/PFS, Association of International Certified Professional Accountants Director of Financial Planning. “A CPA financial planner serves as a trusted advisor who understands their client’s needs and priorities both from a financial and personal perspective by having open, and often difficult, discussions. They act as a ‘quarterback’-- calling the plays and making sure that everyone involved, including family members and other professionals employed by their client, play the role that they are supposed to.”

Members of the AICPA PFP Executive Committee put together the following proactive tips to help Americans handle issues that may arise from elder abuse and potential diminished capacity later in life:

-

Know a Good Scam When You See One

One of the best ways to protect against fraud is to learn about some of the most popular scams. With an awareness of what’s out there, you will be better positioned to recognize a scam before it’s too late. Do your own research, talk with friends about what they’re seeing or heard and consult with your financial team. Remember, if it sounds too good to be true or remotely strange, check the Federal Trade Commission list of scam alerts.

-

Identify Your Team & Establish Responsibilities

It is important to establish a trusted team of professionals, designees and loved ones who will always have your best interests in mind. Review your decisions with each them in advance so that should they be needed to act on your behalf, everyone will know their part. Team members should know and be formally authorized to communicate with one another, and they should all have copies of any relevant legal documents. This helps provide checks and balances, and, since elder financial abuse is often committed by a relative or trusted professional, checks and balances are important.

-

Use Your CPA Financial Planner as ‘the Bad Guy’

Get in the habit of saying ‘I run everything by my CPA financial planner; I'll get back to you’ before making financial commitments to others. That way you will not be caught off guard by scams or stories aimed to take advantage of you. And remember to never give personal or financial information to an unsolicited caller or salesperson.

-

Make Hard Decisions Now

Discuss the tough planning issues head on and proactively. Work with your CPA financial planner to determine all the difficult answers to questions that may arise later in retirement. Discuss housing options and long-term care preferences for a couple of different potential scenarios. This way, you will be prepared for all the roads ahead.

-

Get Your Plan in Place & Revisit it Regularly

A retirement plan is not a set-it and forget-it deal. Once you have a plan, set reminders for quarterly or semi-annual check-ins. Review estate planning documents to make sure they are in place and current. Review beneficiary designations, successor trustee, financial, and medical power of attorney. Regular financial plan check-ins are important during retirement to not only make sure there are enough assets but also to see if any adjustments need to be made due to changes in care or needs.

-

Set-up Protections

You can lessen the risk of elder abuse by establishing checks and balances for Power of Attorney, successor trustee, and key professionals. This way, abuse can be identified early and addressed. If you are worried about competency issues or just can't say no to relatives, consider putting your assets in a Revocable Living Trust and assign a co-trustee. Ensure that all checks – or checks over a certain dollar amount - require two signatures. This can reduce the chances that you give to an unscrupulous scammer.

PFP Trends Methodology

The AICPA’s PFP Trends Survey is administered as an online survey to CPAs who are members of the AICPA Personal Financial Planning Section, including those holding the CPA/PFS credential. The survey, which included responses from 688 CPA financial planners, was conducted from 11/26/2019 through 1/20/2020.

About the AICPA’s PFP Division

The AICPA’s Personal Financial Planning (PFP) Section is the premier provider of information, tools, advocacy, and guidance for CPAs and other professionals who specialize in providing estate, tax, retirement, risk management, and investment planning advice to individuals, families, and business owners. The primary objective of the PFP Section is to support its members by providing resources that enable them to perform valuable PFP services in the highest professional manner.

CPA financial planners are held to the highest ethical standards and are uniquely able to integrate their extensive knowledge of tax and business planning with all areas of personal financial planning to provide objective and comprehensive guidance for their clients. The AICPA offers the Personal Financial Specialist (PFS) credential exclusively to CPAs who have demonstrated their expertise in personal financial planning through testing, experience and learning, enabling them to gain competence and confidence in PFP disciplines.

About the American Institute of CPAs

The American Institute of CPAs (AICPA) is the world’s largest member association representing the CPA profession, with more than 429,000 members in the United States and worldwide, and a history of serving the public interest since 1887. AICPA members represent many areas of practice, including business and industry, public practice, government, education and consulting. The AICPA sets ethical standards for its members and U.S. auditing standards for private companies, nonprofit organizations, federal, state and local governments. It develops and grades the Uniform CPA Examination, offers specialized credentials, builds the pipeline of future talent and drives professional competency development to advance the vitality, relevance and quality of the profession.

About the Association of International Certified Professional Accountants

The Association of International Certified Professional Accountants (the Association) is the most influential body of professional accountants, combining the strengths of the American Institute of CPAs (AICPA) and The Chartered Institute of Management Accountants (CIMA) to power opportunity, trust and prosperity for people, businesses and economies worldwide. It represents 657,000 members and students across 179 countries and territories in public and management accounting and advocates for the public interest and business sustainability on current and emerging issues. With broad reach, rigor and resources, the Association advances the reputation, employability and quality of CPAs, CGMAs and accounting and finance professionals globally.

Contacts

Jonathan Lynch

212-596-6033

Jonathan.Lynch@aicpa-cima.com

James Schiavone

212-596-6119

James.Schiavone@aicpa-cima.com