")

BOSTON--(BUSINESS WIRE)--When it comes to saving and investing one’s hard earned money, who has greater overall success: men or women? If your immediate reaction was “men,” then a new study from Fidelity Investments® may come as something of a surprise—and you wouldn’t be alone. In fact, when asked who they believed made the better investor this past year, a mere nine percent of women thought they would outperform men1. And yet, a growing body of evidence, including an analysis of more than eight million clients from Fidelity2, shows that women actually tend to outperform men when it comes to generating a return on their investments.

With this in mind, it’s concerning that so many women have such a dim view of their money management capabilities. Regardless of education levels, personal or professional achievements, many women still have doubts about their ability to invest effectively. In fact, when asked what financial life skills they wished they learned earlier, the number one answer was “how to invest and make the most of my money.” But perhaps women have learned far more than they realize, considering these findings:

- Women Earn Higher Returns: Fidelity Investments client data analysis3 shows on average, women performed better than men when it comes to investing by 40 basis points, or 0.4 percent. At first glance this may appear to be a minor difference, but can have a significant impact over time.

-

Women Save More: Fidelity’s analysis also

found that when comparing annual savings rates, women come out on top:

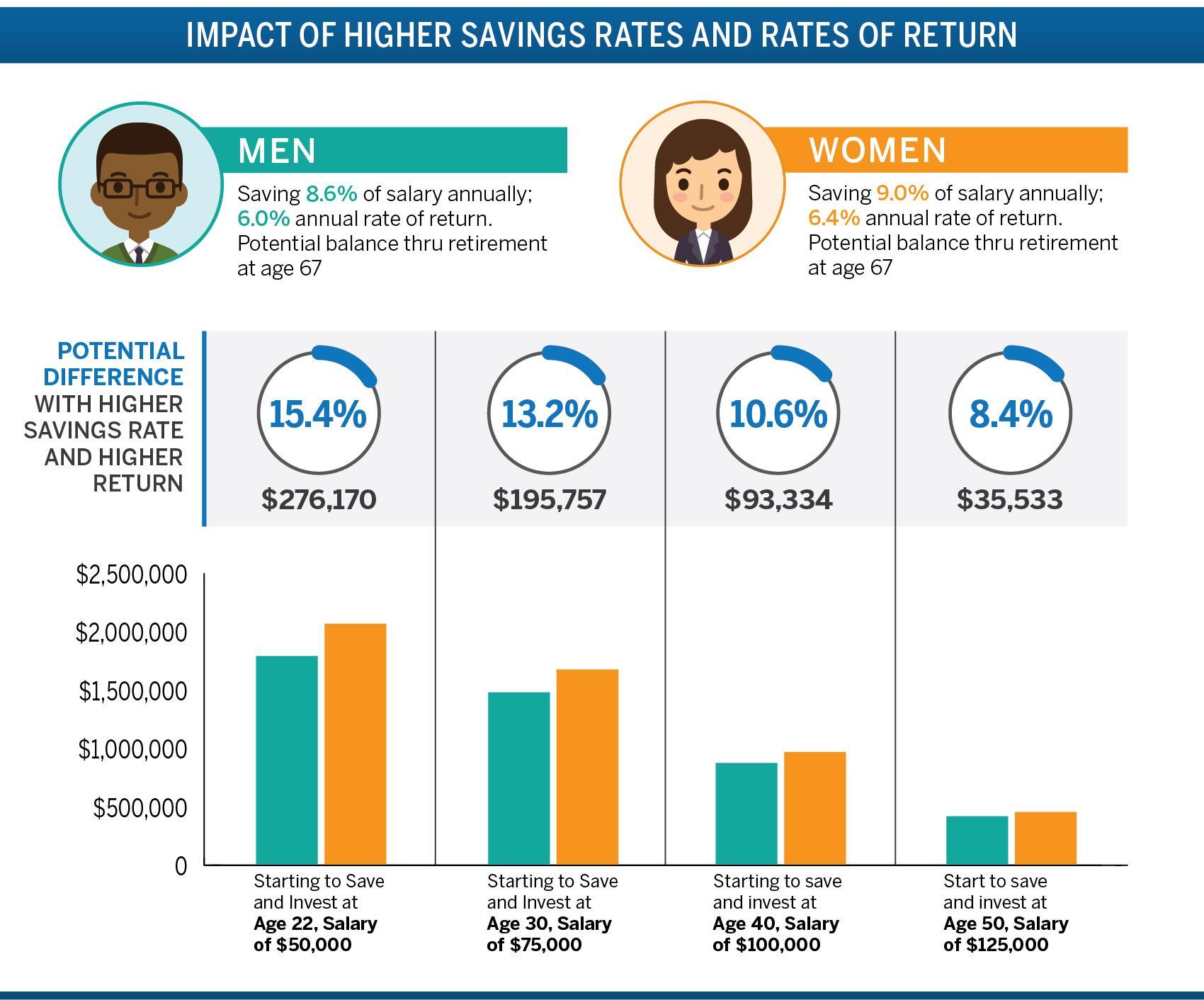

- Looking specifically at workplace retirement accounts4, women consistently saved a higher percentage of their paychecks than their male counterparts at every salary level. Women saved an annual average of 9.0 percent of their paychecks, compared to an average of 8.6 percent saved by their male counterparts.

- Looking at accounts outside of workplace savings5, such as IRAs and brokerage, the data showed that in proportion to their account balances, women saved more. Women added an average of 12.4 percent to their account balance, compared to 11.6 percent for men.

What can saving at a higher rate and earning a higher return mean over time? The impact can be significant, and amplified even more so for younger investors. Using current workplace savings rates, consider these hypothetical examples6:

Over the past three years, Fidelity has seen the number of women investing their money with the firm grow significantly – by 19 percent, to more than 12 million. “The good news is many women are putting themselves in the financial driver’s seat, taking positive steps to save and invest effectively for their future,” said Kathleen Murphy, president of personal investing at Fidelity. “But there are still many who need to do more. The reality is that saving alone is not enough to even keep pace with inflation, so if you’re not investing, you’re likely losing money. Taking the next step to ensure that savings are invested properly and generating growth is critical to helping women progress toward their financial goals and live the lives they deserve.”

Breaking it Down: Women’s Skills and Strengths

Despite their own perceptions that they may not be prepared to manage their personal finances, when women invest, Fidelity’s customer analysis shows many of the characteristics some view as being inherently female are actually factors that may be helping women see strong returns on their investments.

- Plan with purpose, think holistically. Women often build financial plans in terms of life goals for themselves or their families, rather than focusing on performance alone. Women tend to hold a more long term, conservative view with their investments, tending to buy and hold stocks, versus taking quick action during market fluctuations.

- Take on less risk. Women are more likely to have their savings allocated in a more age-based allocation of investments than their male counterparts. In fact, looking specifically at Fidelity retirement savings accounts over the last three years, the percentage of women allocated appropriately for their age has increased by approximately 40 percent. Furthermore, fewer women have their savings fully invested in equities than men (which could represent too much risk and not enough diversification); and women are more likely to invest in target date funds, ensuring they are well diversified.

- Practice patience. When comparing likelihood to buy/sell stocks, Fidelity’s client data revealed that men are 35 percent more likely to make trades than women. Furthermore, men who trade made an average of 55 percent more trades in 2016 than their female counterparts7.

- Education spurs action. Fidelity’s experience has shown that taking part in live and digital events designed as part of the firm’s women’s education program can be a catalyst to taking action. Fidelity has seen a 25 percent increase year-over-year in the number of guidance interactions among women participating in these opportunities.

“The results of Fidelity’s latest analysis reinforces that women too often underestimate their strengths as savers and investors,” added Alexandra Taussig, senior vice president of women investors at Fidelity. “It’s time to celebrate our abilities and maximize them by making a commitment to get more involved with our money.”

Women Eager to Catch Up: More Financial Education Wanted

Fidelity research among professional women across the country shows there’s no shortage of interest in learning more about financial management and investment choices, with over 90 percent saying they want to learn more about financial planning8. For many, this stems from a need to play ‘catch up,’ with a majority reporting a lack of opportunity to learn financial skills earlier in life.

While parents remain the top source of financial advice for most women, only 20 percent said they felt well prepared by their parents to manage their finances as an adult. Even fewer said they learned about these topics in school. Only 24 percent learned about budgeting and setting financial goals; 14 percent said they learned about investing. Overall, only nine percent of women said their education through high school left them well prepared to manage personal finances as an adult. A slightly better 10 percent said this of their college education9.

Today, 88 percent of women say more financial education would provide them with greater confidence in managing their money. When asked what they would most like to learn with 60 minutes of professional financial advice, women across all generations listed ‘learning more about how to invest my money’ as their No. 1 choice10.

But many still hesitate to reach out for help. Women across all generations are less likely to reach out to an adviser than men, with six out of 10 saying they have never consulted with a financial professional. Among this group, the top reason why was feeling like they didn’t have enough money. Other barriers holding women back from addressing their finances: not knowing where to start and simply not making it a priority11.

“Taking just one step can break the inertia holding many women back,” said Taussig. “Whether you’re just getting started building a plan, looking to become more active in managing you investments, or determining how to make your savings last through retirement, commit to following through with one new step toward that goal. In most cases, you’ll find you’re off and running. And there is no shortage of resources to help.”

Three Financial Action Steps

Whether you’re looking to go from saver to investor, address a specific financial task on your personal to do list or generally learn more about women and money, here are three things to do today to get the ball rolling:

1. Commit. Set a personal deadline to take just one step toward a financial goal. Not sure where to start? Fidelity has developed a checklist that provides fundamental steps for women at each stage of their career, and for the life events that can take place throughout our financial lives.

2. Check. Make sure you know what you own, what you owe, and the status of those accounts. Are your investments working to help you reach your goals?

3. Communicate. If you have questions, your friends and family probably do too. Not only is it time for money to stop being a taboo conversation topic, but ensuring you’re on the same page with your loved ones about financial goals and responsibilities can be critical. Fidelity has numerous resources to help have these conversations with parents, partners and kids.

Additional Resources

- Free tools designed for women. Fidelity.com/itstime was designed to provide insights and next steps around the life events that matter most to women, whether you’re about to get married, changing careers or caring for aging parents. Available here are talks and workshops, articles, checklists, and other guidance targeted to help navigate financial challenges.

- Opportunities to learn at your own pace. There are many free seminars, webcasts and other educational opportunities available to fit into busy lifestyles and help guide you to your best next financial step, whether through your workplace, investment companies like Fidelity, or other sources online.

- Experts are readily available. Don’t hold back from asking for guidance. Few have all the answers on their own. Just like you visit a doctor for medical advice, why wouldn’t your take advantage of a financial professional for investment advice? Fidelity professionals are available 24 hours day at 1-800-Fidelity, or online at Fidelity.com – whether you’re a current client or not.

About Fidelity’s Women and Money Survey

Results of this

survey are based on an online omnibus conducted among a demographically

representative U.S. sample of 2,995 adults comprising 1,496 men and

1,499 women 18 years of age and older. The survey was completed during

the period December 1-11, 2016 by ORC International, an independent

research firm. The results of this survey may not be representative of

all adults meeting the same criteria as those surveyed for this study.

About Fidelity Investments

Fidelity’s

mission is to inspire better futures and deliver better outcomes for the

customers and businesses we serve. With assets under administration of

$6.1 trillion, including managed assets of $2.2 trillion as of April 30,

2017, we focus on meeting the unique needs of a diverse set of

customers: helping more than 26 million people invest their own life

savings, 23,000 businesses manage employee benefit programs, as well as

providing more than 12,500 financial advisory firms with investment and

technology solutions to invest their own clients’ money. Privately held

for 70 years, Fidelity employs 45,000 associates who are focused on the

long-term success of our customers. For more information about Fidelity

Investments, visit https://www.fidelity.com/about.

Investing involves risk including the risk of loss.

Fidelity

Investments and Fidelity are registered service marks of FMR LLC.

Fidelity Brokerage Services LLC, Member NYSE, SIPC

900 Salem

Street, Smithfield, RI 02917

Fidelity Investments Institutional Services Company, Inc.

500 Salem

Street, Smithfield, RI 02917

National Financial Services LLC, Member NYSE, SIPC

200 Seaport

Boulevard, Boston, MA 02110

801879.1.0

© 2017 FMR LLC. All rights reserved.

1 ORC Caravan Survey of 514 men, 511 women, 18 years

and older who indicated they had some type of investment account, Jan

5-8, 2017

2 Comparing the investing behavior of eight

million retail customers from Jan 2016 – Dec 2016; measures average of

monthly annualizing returns over 12 months from Jan 2016 – Dec 2016

3

Ibid

4 Comparing the savings behavior of 14 million

workplace customers from Jan 2016 – Dec 2016

5 Comparing

the savings behavior of eight million retail customers from Jan 2016 –

Dec 2016

6 Impact of higher savings is calculated using

fixed monthly returns with contributions made at the beginning of the

period. Beginning balances are assumed to be zero. The potential

difference is calculated by comparing ending balances at retirement for

each hypothetical example. The ending values do not reflect taxes, fees

or inflation. If they did, amounts would be lower. Earnings and pre-tax

contributions are subject to taxes when withdrawn. Distributions before

age 59 1/2 may also be subject to a 10% penalty. Contribution amounts

are subject to IRS and Plan limits. Systematic investing does not ensure

a profit or guarantee against a loss in a declining market. This example

is for illustrative purposes only and does not represent the performance

of any security. Consider your current and anticipated investment

horizon when making an investment decision, as the illustration may not

reflect this. The assumed rate of return used in this example is not

guaranteed. Investments that have potential for the assumed annual rate

of return also come with risk of loss.

7 Fidelity retail

customer analysis of men and women who made at least one trade in 2016.

8

Fidelity Investments Money FIT Women Study, Feb 2015

9

Fidelity Women and Money Survey, Dec 2016

10 Ibid

11

Ibid