Irenic Sends Letter to Theravance Biopharma Regarding the Urgent Need for a Governance Overhaul, Capital Return and Strategic Review

Irenic Sends Letter to Theravance Biopharma Regarding the Urgent Need for a Governance Overhaul, Capital Return and Strategic Review

Despite Months of Private Engagement From Irenic and Presumably Other Investors, Chairman & CEO Rick E. Winningham and Theravance’s Board Refuse to Act in Shareholders’ Best Interests

Notes Theravance’s Total Shareholder Returns are -50% Since Its 2014 Separation and the Company Trades at a Massive Discount Due to Investors’ Lack of Confidence in Leadership

Encourages the Board to Reconsider Irenic’s Suggested Actions, Including Appointing a Shareholder Representative, Modernizing Entrenching Governance Policies and Returning ~$300 Million in Excess Cash

Sees Clear Path to Unlock Nearly $21 Per Share in Value if the Board Adopts Irenic’s Suggestions

NEW YORK--(BUSINESS WIRE)--Irenic Capital Management, LP, a top shareholder of Theravance Biopharma, Inc. (NASDAQ: TBPH), today released the below letter.

***

February 27, 2023

Theravance Biopharma, Inc.

901 Gateway Boulevard

South San Francisco, CA 94080

Attn: The Board of Directors

Subject: The Need for Governance and Strategic Change Following Years of Losses and Underperformance

Dear Members of the Board of Directors (the “Board”),

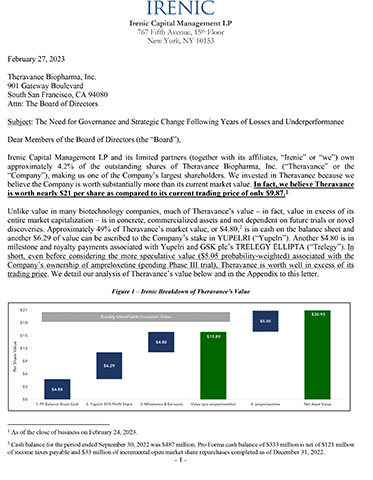

Irenic Capital Management LP and its limited partners (together with its affiliates, “Irenic” or “we”) own approximately 4.2% of the outstanding shares of Theravance Biopharma, Inc. (“Theravance” or the “Company”), making us one of the Company’s largest shareholders. We invested in Theravance because we believe the Company is worth substantially more than its current market value. In fact, we believe Theravance is worth nearly $21 per share as compared to its current trading price of only $9.87.1

Unlike value in many biotechnology companies, much of Theravance’s value – in fact, value in excess of its entire market capitalization – is in concrete, commercialized assets and not dependent on future trials or novel discoveries. Approximately 49% of Theravance’s market value, or $4.80,2 is in cash on the balance sheet and another $6.29 of value can be ascribed to the Company’s stake in YUPELRI (“Yupelri”). Another $4.80 is in milestone and royalty payments associated with Yupelri and GSK plc’s TRELEGY ELLIPTA (“Trelegy”). In short, even before considering the more speculative value ($5.05 probability-weighted) associated with the Company’s ownership of ampreloxetine (pending Phase III trial), Theravance is worth well in excess of its trading price. We detail our analysis of Theravance’s value below and in the Appendix to this letter.

As we have conveyed during our months of private engagement, the substantial disconnect between Theravance’s intrinsic value and its trading price reflects an absence of investor confidence in management and the Board. Investors have substantial concerns with Theravance’s capital allocation, approach to executive compensation and operating costs, and management’s choice of ultimate strategic direction. The lack of confidence is exacerbated by a lack of trust. Shareholders simply do not believe Theravance’s Board and management team are properly aligned with shareholders, and do not have confidence that Theravance leadership will take the necessary steps to maximize shareholder value.3 Moreover, the Company’s leadership does not have a history of value creation. Under Rick Winningham, since the separation of Theravance from Innoviva, Inc. (“Innoviva”), the Company has produced a total shareholder return (“TSR”) of negative 49%.4 A dollar invested in Theravance in 2014 is worth just roughly $0.50 today.5 Meanwhile, Mr. Winningham has received more than $48 million from Theravance in cash and share-based compensation during this period in which shareholders have endured substantial losses.6

Shareholders’ concerns are compounded by Theravance’s outdated and Board-entrenching governance provisions and features. The Company maintains a staggered Board. It has failed to separate the Chairman and Chief Executive Officer roles. The Board is long-tenured and lacks mandatory retirement provisions. It includes directors with substantial over-boarding (contrary to the Company’s own Corporate Governance Guidelines).7 The Board is also rife with potential conflicts and apparent interlocks.8 Over the past few months, we have privately shared these concerns with you and proposed a series of steps to restore shareholder confidence and close the gap between Theravance’s intrinsic value and its market price. We have also proposed entering into a formal cooperation agreement in order to assist in unlocking Theravance’s value and improving governance and oversight. You have rejected our efforts to collaborate.

As a reminder, we have proposed the following:

1. Immediate special dividend of Theravance’s excess cash, totaling ~$300 million.

Theravance ended Q3 2022 with $487 million in cash and $0 of debt. Of the $487 million in cash, $121 million is reserved for taxes payable from the Trelegy sale and $25 million is earmarked to fund the ampreloxetine Phase-III trial. Additionally, $33 million was used for open market repurchases in Q4 2022. As such, the Company has an estimated $308 million of cash on its balance sheet as of year-end. The Company has committed to return just an additional $122 million by year-end 2023 via open market repurchases. This leaves an excess of $186 million in cash which must be returned to shareholders. Given the limited trading liquidity of Theravance, a significant balance of cash should be immediately returned to shareholders via a one-time special dividend as a supplement to or in lieu of further repurchases.

2. Immediate reduction in Theravance’s overhead costs, including the reduction of excessive share-based compensation.

Theravance disclosed that 106 employees remain as part of the new structure. Of the 106 employees, it is our understanding that 15 employees support the sales and marketing efforts of Yupelri. For 2022, Theravance has guided for total operating expenses of $90 million to $100 million, before share-based compensation ($33 million of which was expensed through Q3 2022) and excluding $11 million in ‘one-time’ restructuring-related expenses. Including these ‘non-cash’ and ‘non-recurring’ expenses, the total operating costs will likely exceed $150 million. It is unclear to us why costs are so high. During 2022, Theravance was responsible for just 35% of the costs associated with both the PIFR-2 study and sales efforts supporting Yupelri. The Company has no additional required commercial responsibilities, significant expenditures, or meaningful trials in process. The excessive level of spending is not justifiable.

Theravance’s approach to share-based compensation is particularly concerning. Share-based compensation is a real economic expense borne by shareholders. For the prior three fiscal years (FY2019-FY2021), Theravance has expensed $60 million, $63 million, and $62 million in share-based compensation, respectively. Despite a 75% headcount reduction this year, through Q3 2022, the Company had already expensed $33 million in share-based compensation. Share-based compensation should come down commensurate with the reduction in headcount and incremental dilution should be extremely limited.9

Moreover, management has repeatedly stated that Theravance trades at a material discount to intrinsic value. If this is the case (which we agree it is), the cost of share-based compensation is, in effect, substantially higher than reported.10

3. The announcement of a firm commitment to return all future cash generated by the Company (from milestone payments, asset sales, and earnings) to its shareholders.

Theravance should generate significant cash flows from royalties and milestone payments associated with Trelegy and Yupelri. Given past performance, shareholders are concerned these funds will be wasted. What is needed is a clear and unambiguous commitment from management that all excess cash will be returned to shareholders immediately upon receipt. The lack of clarity regarding go-forward capital allocation represents an unnecessary overhang on Theravance’s value.

4. The announcement of a formal strategic review.

Theravance’s collection of assets exceeds $1.4 billion in value. As management agrees, the current market valuation does not reflect the Company’s intrinsic value (expanded upon further in the appendix of this letter). With just one late-stage drug remaining in the Company’s pipeline, it is now appropriate to proactively consider a broad range of value-maximizing transactions. Were the Company to conduct a proper strategic review with independent financial advisors, we strongly believe that there are buyers for all of the Company and/or individual assets at a substantial premium to Theravance’s trading price.

We encourage the Board to engage independent advisors and immediately initiate a strategic review. Given the continued growth of Yupelri (where Theravance maintains only a 35% profit share interest) and the lack of direct influence over future Trelegy earn-outs, we believe the structure of Theravance is no longer optimized in its current form.

5. Improvements to Theravance’s governance, including adding a shareholder representative as a director and adopting governance best practices.

|

|

To date, the Company has not committed to any of these steps. We believe our suggestions are reasonable and well-calibrated to restore shareholder confidence.15 We hope you reconsider.

Next Steps

We reiterate our desire to work constructively and privately with you to restore confidence and maximize value. Our investment in Theravance is substantial. It reflects our conviction that not only is the Company substantially undervalued but that there are clear, concrete steps that can be taken in short order to unlock that value. We hope this letter is a catalyst for cooperative action in these areas.

Adam Katz |

Andy Dodge |

Zack Fuss |

||

Co-Founder, CIO |

Co-Founder, Director of Research |

Senior Analyst |

Appendix

The combined value of the cash on hand ($333 million), the Yupelri 35% profit share ($436 million), the Trelegy/Yupelri milestones, earn-outs and royalties ($333 million), and the probability adjusted value of ampreloxetine ($350 million) exceeds $1.4 billion or $20.93 per share.16

(1) There is $333 million ($4.80 per share) of pro forma balance sheet cash.

Cash balance for the period ended September 30, 2022 was $487 million. Pro Forma cash balance is net of $121 million of income taxes payable and $33 million of incremental open market share repurchases completed as of December 31, 2022.

(2) The Yupelri 35% profit-share17 interest is worth $436 million ($6.29 per share).

For Q3 2022, Yupelri produced $53.4 million in sales (+36% y/y), an annualized run-rate of $214 million. Margins are estimated to be ~30% today and should exceed 60% at peak. We expect peak sales to exceed $400 million in line with management’s expectations.18

(3) High probability milestones for Yupelri and Trelegy are worth $333 million ($4.80 per share).

Theravance is entitled to a number of high probability earn-outs from Yupelri and Trelegy (plus a number of lower probability yet substantial milestone payments in the event that other former pipeline drugs are commercialized). There are three buckets of incremental value related to Yupelri and Trelegy: (a) Yupelri Global Milestones, (b) Trelegy Mid-Term Milestones and (c) Trelegy Long-Term Royalties. We estimate that the net present value of earn-outs, milestone payments and future royalties from just Yupelri and Trelegy are worth at least $333 million.

For the Yupelri Global Milestones, Theravance is eligible to receive up to $257.5 million in the aggregate from potential global development, regulatory, and sales milestone payments. Outside the U.S. (including China and adjacent territories), Viatris is responsible for development and commercialization and will pay Theravance a tiered royalty on net sales at percentage royalty rates ranging from low double-digits to mid-teens.

For the Trelegy Mid-Term Milestones, Theravance is eligible to receive up to $250 million from sales-based earn-outs through 2026 ($25 million to $100 million per year from 2023 to 2026 with the first threshold at $2.9 billion in sales19).

For the Trelegy Long-Term Royalties, the royalties sold to Royalty Pharma plc (“Royalty Pharma”) in July 2022, revert to Theravance beginning in July 2029. Royalties for ex-U.S. sales revert in July 2029 and for U.S. sales in January 2031. Based upon sell-side consensus and management estimates for Trelegy we value this future royalty stream at $140 million.20

Notably, we assign zero value to potential payouts from other economic interests. Theravance is eligible to receive up to $237.5 million from Pfizer Inc. for its preclinical skin-selective, locally-acting pan-JAK inhibitor program (plus a tiered royalty on worldwide net sales of any potential products) and up to $105 million from Alfasigma for velusetrag, an oral, investigational medicine developed for gastrointestinal motility disorders. Theravance plays little to no role in the achievement of these milestones.

(4) The probability-weighted value of ampreloxetine is $5.05 per share and is worth $20.18 per share if successful.

Ampreloxetine is a potential blockbuster with net present value of ~$1.4 billion if its Phase-III trial is successful. Ampreloxetine is an oral, once daily therapy being developed for the treatment of neurogenic orthostatic hypotension (“nOH”). nOH is a condition in which patients have impaired regulation of standing blood pressure. The current CYPRESS trial is specifically studying patients with Multiple System Atrophy (“MSA”). MSA is a slowly progressive neurodegenerative disease that afflicts an estimated 50,000 Americans. nOH is present in ~80% of MSA patients. In MSA patients with nOH, blood pressure falls when upright, which results in debilitating symptoms. This limits the ability to perform routine daily activities that require walking or standing and meaningfully impair a patient's quality of life. Today, there are two therapies available to address nOH, midodrine and droxidopa, both of which are short-acting, need to be used at least 3x per day and must be ceased in the early evening to avoid supine hypertension.

Given the limitations of existing therapies, ampreloxetine should see greater uptake (if approved). An indication of ampreloxetine’s commercial potential is found in the results of Northera (branded droxidopa). Despite its limited effectiveness for patients with MSA, Northera reached peak sales of $400 million before generic entrants cannibalized sales. Northera never received anything more than a conditional approval from the FDA. Northera pricing ranged from $120,000 to $200,000 (depending on dosage), and as such we believe ampreloxetine peak sales could exceed $1 billion at peak, assuming 8,050 patients with drug pricing of $124,225 per annum. Theravance received $25 million in cash from Royalty Pharma which is expected to fund the majority of the Phase III study costs. In exchange, Royalty Pharma will receive 2.5% for the first $500 million in ampreloxetine net sales and 4.5% for sales in excess of $500 million. This transaction further validates our assumptions around ampreloxetine’s potential value.

If the ampreloxetine Phase III CYPRESS trial reaches its endpoint and receives subsequent FDA approval, we believe that it is worth $1.4 billion. On a probability adjusted basis (we assume a 25% chance of success), we believe the net present value of ampreloxetine is worth $350 million today.

***

About Irenic

Irenic Capital Management, LP is an investment management firm founded by Adam Katz and Andy Dodge. Based in New York City, Irenic works collaboratively with publicly traded companies to ensure operating activities, capital deployment and management incentives are all aligned to create value for the company and its owners. For more information about Irenic, please visit www.irenicmgmt.com.

1 As of the close of business on February 24, 2023.

2 Cash balance for the period ended September 30, 2022 was $487 million. Pro Forma cash balance of $333 million is net of $121 million of income taxes payable and $33 million of incremental open market share repurchases completed as of December 31, 2022.

3 It is notable that not a single member of the Board has made an open market purchase of the Company’s shares since May of 2018. Mr. Winningham has not made an open market purchase of Theravance shares since August of 2017. Dr. Young, the Lead Independent Director, has never made an open market purchase. Similarly, Directors Pakianathan, O’Connor, Alsup, Mitchell, and Broshy have failed to ever buy a single share of the Company’s stock. In fact, of the current Board, the only non-executive director to ever purchase shares was Mr. Malkiel who purchased 1,000 shares in May of 2018 and made purchases in 2017 and 2015. Source: Bloomberg

4 Source: Bloomberg. Mr. Winningham’s tenure as Lead Independent Director at Jazz Pharmaceuticals plc (“Jazz”) has also failed to result in shareholder value creation. With Mr. Winningham as Lead Independent Director, over a nearly 9-year period, Jazz has produced a TSR of 6.6% (not annually, in total). By contrast, during that same time period the S&P Biotech ETF (ticker symbol XBI) produced a TSR of 94.8% and the S&P 500, a TSR of 149.0%. The performance of companies in which Dr. Young, the Lead Independent Director at Theravance, has been most involved are similarly uninspiring and required substantial shareholder intervention to drive performance improvement. To be clear, biotechnology is a high-risk industry and there will be failures and missteps. This is to be expected, but the absence of value creation at Theravance to date and elsewhere in which senior leadership has been involved means that it is all the more important for the Board to include provisions making the Board and management accountable to shareholders and for the Board to include shareholder representation.

5 We have admired the work and writing of Director Burton Malkiel for a long time. In 1994, Mr. Malkiel wrote: “We predict growing recognition of an effective board’s value and venture that, in the future, the investor community will aggressively challenge any ineffective board.” Surely Mr. Malkiel must judge board effectiveness by the results. At Theravance, the results have been disastrous for shareholders and yet management is amply rewarded (and the Board well compensated). Nevertheless, unlike Mr. Malkiel’s prediction of an aggressive challenge, we have attempted to work privately and cooperatively with Theravance’s management and Board. Despite our best efforts, the Theravance Board remains entrenched and allergic to the kind of good governance reforms institutions associated with Mr. Malkiel (Vanguard) have historically extolled. See “The Twenty-First Century Boardroom: Who Will Be in Charge?” Paul B. Firstenberg & Burton G. Malkiel, Sloan Management Review, Fall 1994.

6 Company SEC filings.

7 For example, Dr. Young, the Lead Independent Director, sits on four public company boards. He is the Chairman of one of those companies. Dr. Young, while eminently qualified, is over-boarded and violates Theravance’s own over-boarding guidelines. Similarly, Dr. Pakianathan sits on four public company boards, is the Managing Partner of a biotechnology venture capital firm and also serves as the Vice Chairman of the San Francisco Conservatory of Music. Directors Dr. Alsup and Dean Mitchell serve on the boards of five public companies. Additionally, Dr. Alsup has a full-time job as Chief Scientific and Medical Officer of NDA Group AB, a Swedish pharmaceutical consulting firm. Remarkably, the Board is clearly aware of the problem of over-boarding and yet fails to adhere to its own guidelines. Theravance’s Corporate Governance Guidelines provide that “…in order to ensure sufficient time and attention to meet the responsibilities of Board membership, directors shall serve on no more than three boards of directors of publicly traded companies, including this Board, without consent of the Nominating/Corporate Governance Committee.” Surprisingly, and without justification to shareholders, the Nominating/Corporate Governance Committee apparently waived the three public board limitation for a majority of the Company’s non-executive directors, including the vital Lead Independent Director, and in two of those cases did so to facilitate not merely a fourth directorship but a fifth.

8 Interlocking Board directorships limit the ability of Board members to effectively provide independent supervision given the ways in which issues and relationships in one boardroom might affect decision-making in another. Amongst other things, Theravance’s own Corporate Governance Guidelines provide that “periodically, the full Board (pursuant to a process adopted by the Nominating/Corporate Governance Committee) should review Board and individual director performance.” Interlocking directorships leave the independence of these reviews and other decisions in question. Concerningly, two Theravance Board members serve on the Kinnate Biopharma Inc. board together and two Theravance Board members serve on the Praxis Precision Medicines, Inc. board together. Further, soon after FS Development Corp. II, where a current Theravance Board member served, merged with Pardes Biosciences, another current Theravance Board member was appointed to Pardes Biosciences’ board. There are further interconnections through private firms and organizations. In short, the Board is a tightly knit, economically-intertwined group unlikely to properly self-assess and provide effective supervision.

9 Because Theravance amortizes RSU issuances over time, GAAP share-based compensation expense may not match the prevailing market value of dilution. Separately, we note that Theravance’s GAAP share-based compensation expense may structurally under-represent the real economic value provided to senior executives. This is due to the Company’s granting of Performance Share Units for which the “probability of achievement” does not require their expensing.

10 Given the extremely high levels of executive compensation, the absence of insider open market purchases is of further concern. Since the spin-off of Theravance, Mr. Winningham has received over $48 million in total compensation. Board members receive ~$100,000 in cash annually (plus ~$200,000 in stock and an additional $57,000 in options). Given the marked undervaluation of Theravance, insiders should be using some of that compensation to purchase shares of the Company in the open market (which has not occurred since 2018).

11 Theravance’s governance provisions run contrary to almost all universally agreed-upon investment stewardship principles. Theravance has repeatedly received poor scores from Institutional Shareholder Services Inc. (“ISS”) for its corporate governance and yet has done little to address its governance deficiencies. In fact, the situation is getting worse. In 2020, on a scale of 1 to 10, with 10 being the highest risk, Theravance got a 6 for corporate governance from ISS. In 2021, Theravance again received a 6, and in 2022, Theravance fell to a 7. It’s not that the Board is unaware of its deficiencies, it simply refuses to address them, and while we acknowledge that shareholder approval would be required to implement certain of these governance enhancements, the Board could at least take the initial step of recommending and proposing such changes for shareholders to vote on.

12 Vanguard Global Investment Stewardship Principles, November 2021.

13 The Company’s Lead Independent Director has served in that capacity since the Company’s separation (the same tenure as the CEO and Chairman). That Lead Independent Director is over-boarded and is potentially conflicted given his role at Blackstone Life Sciences (see above). An absence of an effective Lead Independent Director makes the separation of the Chairman and CEO roles all the more critical.

14 Vanguard Global Investment Stewardship Principles, November 2021.

15 Theravance’s unwillingness to address its governance deficiencies is particularly egregious and suggests substantial management and Board entrenchment. The suggestions we have made provide for the bare minimum of rights a modern corporation provides for its shareholders.

16 Based upon a Pro Forma diluted share count of 69.4 million. As of October 31, 2022, Theravance had 67.4 million ordinary shares outstanding. As of Q3 2022, 5.0 million potential ordinary shares were excluded from the ordinary share count. The Company repurchased $33 million shares or 3.0 million shares in the open market through December 31, 2022.

17 Theravance owns a 35% profit share interest in Yupelri via a collaboration agreement with Viatris Inc (“Viatris”). Theravance’s commercial and medical teams cover the hospital market and Viatris is responsible for covering outpatient-based community healthcare professionals.

18“YUPELRI remains early in its product lifecycle, has demonstrated market share growth quarter-over-quarter, despite the respiratory pandemic. We believe it’s got the potential to generate U.S. peak sales exceeding $400 million” – Rick Winningham, November 4, 2021.

19 GSK plc, reported Q4 2022 Trelegy sales of $547 million growing +19% y/y in constant currency and a run-rate of $2.2 billion.

20 Management valued the Trelegy Long-term Royalties at $200 million per July 13, 2022 presentation.

Contacts

For Investors:

Irenic Capital Management

contact@irenicmgmt.com

For Media:

Longacre Square Partners

Greg Marose / Charlotte Kiaie, 646-386-0091

irenic@longacresquare.com