")

")

")

VANCOUVER, British Columbia--(BUSINESS WIRE)--Black Dragon Gold Corp. (ASX/TSX-V: BDG) ("Black Dragon" or the "Company") is pleased to announce the positive results of the Preliminary Economic Assessment ("PEA") completed on its 100% owned Salave Gold Project ("Salave" or "Project") located in Asturias in northern Spain. The PEA is based on the recently completed Mineral Resource Estimate completed by CSA Global (See October 25, 2018 News Release). All figures are in United States Dollars unless otherwise stated.

The PEA demonstrates robust economics for an underground mining operation with a 14-year mine life.

Paul Cronin, Managing Director and CEO commented,

"The completion of the PEA is a major milestone on the path to development of the Salave Project and the metrics support our belief that Salave can potentially generate strong returns for shareholders. It forms the first step in our permitting process, presenting a new optimised process on a zero- discharge basis that minimises the visual and surface impact of the project.

The robust results of this PEA underline the potential economic viability of the current Salave resource to be mined over an initial 14 year mine life, and our successful drilling campaign last year indicates strong potential for growth in mine life at Salave.

This study supports that Salave can produce over 1.1Moz (560 kt of concentrate averaging over 59 g/t Au), providing a number of marketing options for export and refining, minimising the need for additional plant and equipment, and hence reducing the Project’s footprint. The relatively low upfront capex also opens alternative financing opportunities which will ensure that both shareholders and the local community benefit from the success of this Project."

KEY PEA OUTCOMES

- Pre-Tax NPV at 5% discount rate: US$ 296.2 million.

- After-Tax NPV: US$ 230.0 million

- Pre-Tax Internal Rate of Return ("IRR"): 28%

- After-Tax Internal Rate of Return ("IRR"): 25%

- After-Tax Payback: 3.8 years

- Pre-Production Capital Cost, including contingency: US$ 95.3 million

- Life of Mine ("LOM") Sustaining Capital Cost: US$19.3 million

- Estimated Average LOM Total Cash Cost: $729/ounce (oz) Au

- Estimated Average LOM All-In Sustaining Costs ("AISC"): $752/oz Au

CAUTIONARY STATEMENT

- The PEA is a preliminary technical and economic study of the potential viability of the Salave Gold Project. It is preliminary in nature and includes Inferred Mineral Resources that are considered too speculative geologically to have economic considerations applied to them that would enable them to be categorized as Mineral Reserves. There can be no assurance, and there is no certainty, that the preliminary economic assessment contained therein will be realised. Further exploration and evaluation work and appropriate studies are required before Black Dragon will be in a position to estimate any Ore Reserves or to provide any assurance of an economic development case.

- The production target and forecast financial information referred to in this PEA are comprised of Measured and Indicated Mineral Resources (73%) and Inferred Mineral Resources (27%). The proportion of Inferred Mineral Resources is not determinative of the project viability and does not feature as a significant proportion early in the mine plan.

- Metallurgical recoveries have been based on test work data and costs have been estimated by independent consultants generally from budget quotations, factored estimates or cost data from similar operations/projects. Cost estimate accuracy for the PEA is in the order of +/-35%.

- The PEA is based on the material assumptions outlined herein and in the report. These include assumptions about the availability of funding. While BDG considers all of the material assumptions to be based on reasonable grounds, there is no certainty that they will prove to be correct or that the range of outcomes indicated by the PEA will be achieved. To achieve the range of outcomes indicated in the PEA, among other things, funding of in the order of US$100 million will likely be required. Investors should note that there is no certainty that Black Dragon will be able to raise that amount of funding when needed.

- It is also likely that such funding may only be available on terms that may be dilutive to or otherwise affect the value of BDG’s existing shares. It is also possible that BDG could pursue other ‘value realisation’ strategies such as a sale, partial sale or joint venture of the project. If it does, this could materially reduce BDG’s proportionate ownership of the project. Given the uncertainties involved, investors should not make any investment decisions based solely on the results of the PEA.

NEXT STEPS

- Submission of the Project Description for the Environmental and Social Impact Assessment ("ESIA") in February 2019;

- Additional geophysics over the entire Investigation Permit at Salave – April 2019;

- Issuance of the ESIA Terms of Reference in June 2019;

- Soil Geochemistry testing on potential drill targets – June 2019;

- Pre-Feasibility Study – October 2019.

PEA KEY ASSUMPTIONS AND INPUTS

- Assumed gold price: US$1,250/oz

- Exchange Rate of $1.15 / €

- Life of Mine: 14-years

- Main Underground Mining Method: Vertical Retreat & Sub-Level Stoping

- Average Diluted Head Grade: 3.87 g/t Au

- Total Underground Dilution: 43%

- LOM Plant Throughput 9.19 Mt

- Access Ramp Gradient of 15% at a 5.0m x 5.5m profile

- Mineralised Zone Development at a 4.0m x 4.5m profile

- Average Mining and Processing throughput: 2,000 tonnes per day ("tpd")

- Flotation Plant Recoveries: 97%

- Average Annual Production (LOM): 79,200 oz Au in concentrate at an average grade of 59.7 g/t Au

- LOM recovered gold in concentrate production: 1,108,420 oz;

- Refining and Processing Charges: US$368/t concentrate or US$188/oz Au

Table 1 - PEA Summary Parameters

| Input | Unit | ||||

| Physical Parameters | |||||

| Total Mineralised Material Tonnes Mined (LOM) | Mt | 9.19 | |||

| Average Annual Throughput (LOM) | ktpa | 656.3 | |||

| Head Grade | Au g/t | 3.87 | |||

| Gold Recovery to Concentrate | % | 97% | |||

| Mine Life | years | 14 | |||

| Gold Grade of Concentrate | Au g/t | 59.71 | |||

| Total Concentrate Produced | kt | 560.5 | |||

| Total Ounces in Concentrate | koz | 1,108.4 | |||

| Average Annual Production (LOM) | koz | 79.2 | |||

| Cost Parameters | |||||

| Mining Costs | US$/t | 40.68 | |||

| Processing Costs | US$/t | 14.00 | |||

| General & Administrative | US$/t | 2.71 | |||

| Total Costs | US$/t | 57.39 | |||

| Pre-Production Capital Costs | |||||

| Mine Development & Infrastructure | US$m | 29.7 | |||

| Mining Equipment | US$m | 11.2 | |||

| Tailings | US$m | 1.3 | |||

| Process Plant | US$m | 28.3 | |||

| Owners Costs & EPCM | US$m | 12.5 | |||

| Contingency (15%) | US$m | 12.4 | |||

| Total Pre-Production Capital | US$m | 95.3 | |||

| Sustaining Capital | US$m | 19.3 | |||

| LOM Cash Costs | US$/oz | 729.15 | |||

| LOM AISC | US$/oz | 752.80 |

MINERAL RESOURCE ESTIMATE

An updated NI 43-101 Mineral Resource Estimate, effective 22 October 2018 is included in this PEA and has been filed on SEDAR and the ASX market announcements platform (See October 25, 2018 News Release).

| Category | Tonnes | Au | |||||

| Mt | g/t | koz | |||||

| Measured | 1.03 | 5.59 | 185 | ||||

| Indicated | 7.18 | 4.43 | 1,023 | ||||

| Measured & Indicated | 8.21 | 4.58 | 1,208 | ||||

| Inferred | 3.12 | 3.47 | 348 | ||||

Notes:

1. Rounding may cause apparent discrepancies

2.

Resource Estimate conducted by CSA Global of Perth Australia ("CSA")

with an effective date of October 22, 2018. Classification of the MRE

was completed based on the guidelines presented by Canadian Institute

for Mining (CIM, May 2014), adopted for Technical Reports which adhere

to the regulations defined in Canadian NI 43-101. The Mineral Resource

Estimate was also prepared in accordance with the Australasian Code for

Reporting of Exploration Results, Mineral Resources and Ore Reserves,

2012 edition ("2012 JORC Code").

3. The Mineral Resource

Estimate was first announced on 25 October 2018. Black Dragon confirms

that it is not aware of any new information or data that materially

affects the information in the previous announcement and that all

material assumptions and technical parameters underpinning the Mineral

Resource Estimate continue to apply and have not materially changed.

4.

A cut-off grade of 2 g/t Au has been applied when reporting the Mineral

Resource Estimate.

5. Mineral Resources that are not Mineral

Reserves do not have demonstrated economic viability but do have

reasonable prospects for eventual economic extraction.

6. The

quantity and grade of reported Inferred Resources in this estimation are

conceptual in nature and there has been insufficient exploration to

define these Inferred Resources as an Indicated or Measured Resource. It

is uncertain if further exploration will result in upgrading them to an

Indicated or Measured Resource category, although it is reasonably

expected that the majority of the Inferred Resources could be upgraded

to Indicated Mineral Resources with further exploration.

7. The

Mineral Resource Estimate underpinning the production targets in this

announcement was prepared by a Competent Person under the 2012 JORC Code.

8.

The title of the report is "Salave Gold Project Mineral Resource Update

for Black Dragon Gold Corp.", with an effective date of October 22,

2018, and it was authored by Ian Stockton, B.Sc (Geol)., MAusIMM, FAIG,

Dmitry Pertel, MSc (Geol), MAIF, GAA, and Galen White, B.Sc, FAusIMM,

FGS.

POTENTIALLY EXTRACTABLE PORTION OF MINERALISATION FOR MINE PLANNING

The mine plan supported by the PEA demonstrates that approximately 81.1% of the total 2018 updated Mineral Resource tonnage is amenable to underground extraction. For purposes of mine planning, the potentially extractable portion of the Mineral Resources are comprised of 9.19 million tonnes at a diluted grade of 3.87 g/t Au, containing just over 1.1 million ounces of gold. The mineralised material modelled to be mined in the PEA contains Mineral Resources classified in the Inferred category (28%) that are too speculative geologically to have economic considerations applied that would enable them to be categorized as Mineral Reserves. These Inferred Resources will require further exploration and definition to meet the criteria to be classified as Indicated or Measured Mineral Resources before being considered for conversion to Mineral Reserves at the next level of detailed economic study.

MINE PLAN

Given environmental and community considerations, the PEA has only evaluated underground mining operations. The primary mining method selected for detailed analysis in this study was the vertical retreat mining ("VRM"). Sub-level stoping was considered as a secondary method applicable to specific vertical thin geometries (<15m length). Rock and paste fill will be used as backfill to maximize mining recovery.

The mine design was based on basic economic assumptions to create mineable stope outlines. A value of 2 g/t was assumed as mine cut-off grade. Mining dilution and mineralised material loss factors were also applied to each mining shape to reflect the selected mining method.

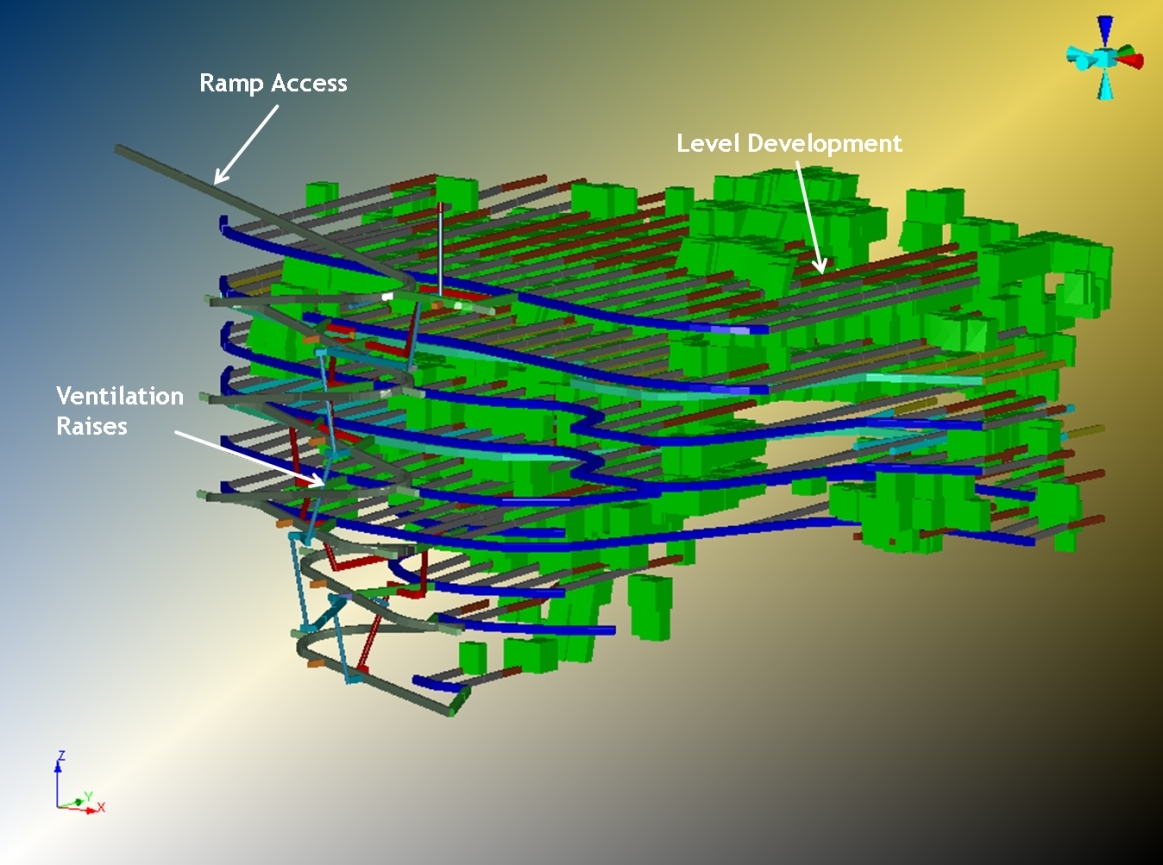

The mine production rate targets a 0.70 Mtpa of RoM. A conceptual mine layout was designed including stopes and development as illustrated in Figure 1, with 60m levels and 3 x 20m sub-levels. The total mineralised material from stopes, drives and sill pillar recovery (50%) will total 9.2Mt at 3.87 g/t Au.

A long term mine schedule was created integrating stopes and development as shown in Figures 2 and 3. Mineralised zones were sequenced to prioritise higher grades at lower operating costs.

MINERAL PROCESSING

In order to minimise potential social and environmental issues, processing of Salave mineralised material has been limited to crushing, grinding and flotation, with concentrates exported via local ports. Mine feed will be crushed on surface at a rate of 0.7 Mtpa, and then be processed via conventional SAG and ball milling followed by sulphide flotation and thickening.

The run-of-mine will feed a primary jaw crusher with a capacity of 400 t/h with a physical availability of 70% with design factor of 20%.

From an intermediate stockpile, the coarse material will feed the mill circuit which consists of a conventional SAG and ball mill configuration working in close circuit with the cyclones.

The flotation circuit consists of a number of cells of 300-400 m3 capacity (9-10 cells of 40 m3 each) with two conditioning tanks for pH stabilisation and reagents.

The final stage consists of tailings thickening to minimise the fresh water consumption and to re-cycle process water. A ‘paste’ thickener will achieve a product of 70-75% of solids.

Based on flotation test work conducted to date, it is assumed that 97% of the gold head grade will be recovered in the flotation concentrate that will be thickened, filtered and bagged for shipping to customers.

INFRASTRUCTURE AND TAILINGS

Power to the project is available from Tapia, which is linked to the Asturias main distribution grid, and an existing network of power lines enter the property that are connected to the Spanish national transmission grid. Water for both domestic and plant usage can be sourced from wells, the Porcia River (2.5km east of the property) or the reticulated water supply that is currently in place near the plant location.

A Tailings Management Facility ("TMF") will be constructed at surface for temporary storage of plant tailings. The paste and backfill of the mine will minimise the amount of tailings storage at surface, and various options for complete tailings disposal are being evaluated. The TMF design will involve water recovery in the processing plant and transportation to geo-membrane lined facility eliminating any risk for potential surface and ground water contamination.

Surface facilities to support the Salave Project will include an administration and engineering building, security, warehouse, fuel and explosive storage, fire protection, maintenance shops with a site design to accommodate for 50 full time staff.

CAPITAL COSTS AND SENSITIVITIES

| Input (US$M) | Pre-Production | Sustaining | LOM | ||||

| Development | 29.7 | 15.7 | 45.3 | ||||

| Equipment & Infrastructure | 11.2 | 3.6 | 14.8 | ||||

| Tailings | 1.3 | 0.0 | 1.3 | ||||

| Process Plant | 28.3 | 0.0 | 28.3 | ||||

| Owner Costs & EPCM | 12.5 | 0.0 | 12.5 | ||||

| Contingency (15%) | 12.4 | 0.0 | 12.4 | ||||

| Total Capex | 95.3 | 19.3 | 114.6 |

|

Sensitivity Analysis |

|||||||||||||||||||

| Parameter | After-Tax NPV (US$M) | % relative to the Base Case | |||||||||||||||||

| -20% | Base Case | +20% | -20% | Base Case | +20% | ||||||||||||||

| Gold price | 95.8 | 230.0 | 361.0 | -58% | 0% | 57% | |||||||||||||

| Processing costs | 244.5 | 230.0 | 163.4 | 6% | 0% | -29% | |||||||||||||

| Mining costs | 296.1 | 230.0 | 192.3 | 29% | 0% | -16% | |||||||||||||

| Capex | 245.3 | 230.0 | 214.6 | 7% | 0% | -7% | |||||||||||||

| Gold Price Sensitivities | |||||||||||||||||||

| Macro Parameters | Unit | -20% | Base Case | +20% | |||||||||||||||

| Gold Price | US$/oz | 1,000 | 1,250 | 1,500 | |||||||||||||||

| Pre-Tax | |||||||||||||||||||

| NPV5% | US$M | 122.2 | 296.2 | 469.2 | |||||||||||||||

| IRR | % | 16% | 28% | 40% | |||||||||||||||

| Post-Tax | |||||||||||||||||||

| NPV5% | US$M | 95.8 | 230.0 | 361.0 | |||||||||||||||

| IRR | % | 14% | 25% | 36% | |||||||||||||||

| Payback | Years | 6.3 | 3.8 | 2.6 | |||||||||||||||

PROJECT FUNDING

The Board of BDG believes there is a reasonable basis to assume the necessary funding for the Salave Gold Project will be obtained for the following reasons:

- The Company has been able to raise funding for its exploration over the past years in order to progress its project. In the last two years BDG has raised over $14.5 million via equity placements. These raises indicate a clear base of support from new and existing shareholders and third-party investors. The Company considers it will be able to raise funding for the next stage of the Project, which will advance the Project to the completion of a detailed Feasibility Study.

- The positive outcomes delivered by the PEA give confidence to the Board in the ability of the Company to fund the development capital through conventional debt and equity financing. A mix of debt and equity is the most likely funding model so 100% of the capital expenditure will not need to be borrowed. The Board has a strong financing track record in funding start up mining operations, and in their view, it is reasonably expected that when the project parameters in this PEA are met, that funding will be able to be arranged. Notwithstanding this, the normal risks for the raising of capital will apply to the Company, such as the state of equity capital and debt markets, the results of the Feasibility Study and the price of gold.

-

The Company believes that its funding opportunities will be improved

at the completion of the Feasibility Study as a result of:

- (i) confidence in the possibility to increase the Mineral Resource Estimate that would serve to improve the mine life of the Project;

- (ii) confirmation of earlier metallurgical test work to support, optimise and potentially improve concentrate grades; and

- (iii) finalisation of further engineering studies to improve the accuracy of the assessed capital and operating costs

- (iv) offtake contracts for concentrates to improve revenue and treatment charge assumptions

- The funding models being considered will depend on the outcomes of the Feasibility Study, but as set out above will likely be conventional debt and equity financing, but may include convertible notes, gold streaming, prepayment of royalties and other options for projects of a similar nature.

- The raising of equity by the Company may be dilutive to existing shareholders, but that will depend on the price at which the then funding is completed. Where the market capitalisation of the Company is low as against the amount of equity that is required to be raised at the time, there is a high likelihood that shareholders will be substantially diluted. This is to be balanced against the reasonable expectation of the Company that as the Project becomes more advanced, the value of the Company is more likely to increase, resulting in the actual dilution to existing shareholders being less. The reality is that in this case, although the percentage holding of each shareholder will be reduced, the value of that holding will be assessed against a Company that is anticipated to have a higher market capitalisation at the time of the raising.

PEA KEY RECOMMENDATIONS

CRS Ingenieria ("CRS"), in Madrid were the principal authors of the PEA and have made the following recommendations for further evaluation that may improve the economics of the project:

- The mineralisation style indicates that both vertical retreat mining (VRM) and room and pillar (RP) are applicable to Salave. For this study, a combination of VRM and SLS was selected, configured with 60m-height panels, however, CRS recommends assessing the benefits of RP for individual panels.

- The production rate of Salave used for the PEA was 0.70 Mtpa. While this production capacity is optimal under current assumptions of mining method and cut-off grade, CRS suggests the evaluation of alternative cut-off strategies that may lead to review the production rate.

- Evaluate mining methods by panel and create integrated layouts.

- Develop detailed geotechnical studies to estimate stope and room dimensions and modifying factors such as dilution and mineralised material loss.

- Develop a volume balance of waste and paste over the LoM sequence.

- Further investigate low grade materials by additional drilling to verify geological continuity.

- Sill pillars may be recovered if specific technical and economic studies demonstrate that economic extraction could reasonably be justified under realistic conditions. CRS recommends the completion of detailed geotechnical studies to confirm the viability of sill pillar recovery.

- Complete an economic study considering obtain free gold through panning before shipment the product.

- Develop a detailed market study to identify potential clients for the Salave gold concentrates.

QUALIFIED PERSONS AND COMPETENT PERSONS STATEMENT

The information in this announcement that relates to the PEA for the Salave Gold Project is based on and fairly represents information and supporting documentation prepared by CRS Ingenieria and CSA Global. Paulo Laymen (P.Eng., M.AusIMM., B.Eng., M.Eng.) of CRS Ingenieria supervised the preparation of the PEA, is independent of the Company and a qualified person as defined by National Instrument 43-101 and has reviewed and approved the technical disclosure reported herein. Dmitry Pertel (P.Geo., MSc (Geol), MAIF, GAA) and Belinda van Lente (P.Geo.) of CSA Global were responsible for the Mineral Resource Estimate and are independent of the Company and qualified persons as defined by National Instrument 43-101 and have reviewed and approved the technical disclosure reported herein.

The NI 43-101 Technical Report will be fined on SEDAR within 45 days of this release.

BLACK DRAGON GOLD CORP.

1000 Cathedral Place

925 West Georgia

Street

Vancouver, BC V6C 3L2, Canada,

T- +44 20 79934077 F-

+44 20 71128814

info@blackdragongold.com

www.blackdragongold.com

ABOUT BLACK DRAGON GOLD

Black Dragon Gold "BDG" is the 100% owner of one of the largest undeveloped gold projects in Europe, the Salave project. Salave is situated in the North of Spain in the province of Asturias. The Salave project has an updated combined Measured and Indicated Mineral Resource of 8.21 million tonnes grading 4.58 g/t Au, containing 1.21 million ounces of gold, plus Inferred resources totalling 3.12 million tonnes grading 3.47 g/t Au, containing 348,000 ounces of gold.

A full technical report summarizing the Mineral Resource estimate completed by CSA Global is available on the company’s web site and posted on SEDAR. In addition to the current Mineral Resource, historical exploration work suggests there is the potential for additional mineralisation within Black Dragon’s landholdings.

FORWARD LOOKING STATEMENTS

This news release contains forward-looking statements that are based on the Corporation's current expectations and estimates. Forward-looking statements are frequently characterized by words such as "plan", "expect", "project", "intend", "believe", "anticipate", "estimate", "suggest", "indicate" and other similar words or statements that certain events or conditions "may" or "will" occur. Such forward-looking statements involve known and unknown risks, uncertainties and other factors that could cause actual events or results to differ materially from estimated or anticipated events or results implied or expressed in such forward-looking statements. Such factors include, among others: the actual results of current planned exploration activities; changes in project parameters as plans to continue to be refined; possible variations in recovered material grade or recovery rates; accidents, labor disputes and other risks of the mining industry; delays or any inability in obtaining governmental approvals or financing; and fluctuations in metal prices. There may be other factors that cause actions, events or results not to be as anticipated, estimated or intended. Any forward-looking statement speaks only as of the date on which it is made and, except as may be required by applicable securities laws, the Corporation disclaims any intent or obligation to update any forward-looking statement, whether as a result of new information, future events or results or otherwise. Forward-looking statements are not guarantees of future performance and accordingly undue reliance should not be put on such statements due to the inherent uncertainty therein.

Neither the TSX Venture Exchange, nor its Regulation Services Providers (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this news release.

All figures are rounded to reflect the relative accuracy of the news release.