(Source: IHS Markit)")

")

")

NEW YORK--(BUSINESS WIRE)--Latest survey data signalled a marked improvement in business conditions across the U.S. manufacturing sector in May. The strong performance reflected sharp expansions in output and new orders. Strong client demand meant operating capacity came under greater strain, with backlogs increasing at the fastest pace since September 2015 and supplier delivery times lengthening to the greatest extent on record. Strong demand for inputs contributed to a sharp rise in purchasing costs, which in turn fed through to a marked rise in output prices.

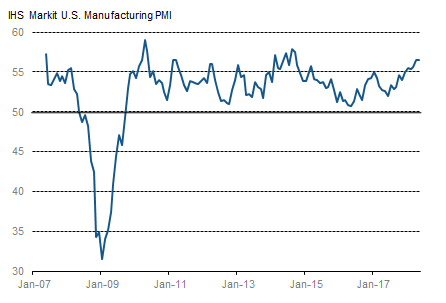

The seasonally adjusted IHS Markit final U.S. Manufacturing Purchasing Managers’ Index™ (PMI™) registered 56.4 in May, down fractionally from 56.5 in April. The reading marked the second-strongest improvement in the health of the sector since September 2014. The upturn was largely driven by sharp increases in production and new business. The greatest lengthening in supplier delivery times since the series began in October 2009 also contributed to the headline figure.

Factory output continued to increase at a robust pace in May, despite the rate of growth softening slightly. More favourable demand conditions and greater client demand were widely cited as driving the expansion of production.

Reflective of stronger demand conditions, new orders increased sharply in May. Moreover, the rate of growth was the second-fastest since September 2014 (after April 2018). Alongside the acquisition of new clients, panellists also noted that customers were demonstrating a greater propensity to spend. In contrast, new export orders increased only marginally.

As the rate of new business growth continued to outstrip that of output, backlogs rose again in May, increasing at the fastest rate in over two-and-a-half years. As a result, firms added to their payrolls again, with the rate of job creation picking up slightly during the month though failing to match the highs seen earlier in the year.

Meanwhile, price pressures remained elevated. Although rates of both input cost and selling price inflation eased slightly, they were nonetheless the second-fastest since September and June 2011 respectively (both after April 2018). Panellists reported that higher input costs were often due to suppliers being able to hike prices in response to strong demand.

Increased pressure on supply chains led to the greatest deterioration in vendor performance in the series’ history. Consequently, stocks of purchases rose at the quickest pace for four months as firms increased their efforts to create safety stocks.

Finally, business confidence remained robust in May, climbing to the second-highest since February 2015.

Comment

Commenting on the final PMI data, Chris Williamson, Chief Business Economist at IHS Markit, said:

“The US manufacturing sector enjoyed another bumper month in May, though continues to run hot.

“The past two months have seen the strongest back-to-back improvements in order books since the fall of 2014, fueled by strengthening domestic demand. New orders have in fact now grown at a faster rate than output in each of the past five months, highlighting how producers have struggled to boost production to meet sales. In the words of one manufacturer, 'we’re selling more than we can make.'

“The upturn has stretched supply chains to the extent that May saw the greatest lengthening of delivery times in the near-ten year history of the survey. Producers are also finding it difficult to find suitable staff.

“With sales growing faster than production, backlogs of work are accumulating at the fastest rate for nearly four years, which should support further production growth in coming months. Business expectations regarding future production in fact picked up again to one of the highest levels seen over the past three years, adding to signs that strong growth will persist through the summer months.”

Note to Editors:

IHS Markit originally began collecting monthly Purchasing Managers' Index™ (PMI™) data in the U.S. in April 2004, initially from a panel of manufacturers in the U.S. electronics goods producing sector. In May 2007, IHS Markit’s U.S. PMI research was extended out to cover producers of metal goods. In October 2009, IHS Markit’s U.S. Manufacturing PMI survey panel was extended further to cover all areas of U.S. manufacturing activity. Back data for IHS Markit’s U.S. Manufacturing PMI between May 2007 and September 2009 are an aggregation of data collected from producers of electronic goods and metal goods producers, while data from October 2009 are based on data collected from a panel representing the entire U.S. manufacturing economy. IHS Markit’s total U.S. Manufacturing PMI survey panel comprises over 600 companies.

The panel is stratified by North American Industrial Classification System (NAICS) group and company size, based on industry contribution to U.S. GDP. Survey responses reflect the change, if any, in the current month compared to the previous month based on data collected mid-month. For each of the indictors the ‘Report’ shows the percentage reporting each response, the net difference between the number of higher/better responses and lower/worse responses, and the ‘diffusion’ index. This index is the sum of the positive responses plus a half of those responding ‘the same’.

The Purchasing Managers’ Index™ (PMI™) is a composite index based on five of the individual indexes with the following weights: New Orders – 0.3, Output – 0.25, Employment – 0.2, Suppliers’ Delivery Times – 0.15, Stocks of Items Purchased – 0.1, with the Delivery Times Index inverted so that it moves in a comparable direction.

Diffusion indexes have the properties of leading indicators and are convenient summary measures showing the prevailing direction of change. An index reading above 50 indicates an overall increase in that variable, below 50 an overall decrease.

IHS Markit do not revise underlying survey data after first publication, but seasonal adjustment factors may be revised from time to time as appropriate which will affect the seasonally adjusted data series. Historical data relating to the underlying (unadjusted) numbers, first published seasonally adjusted series and subsequently revised data are available to subscribers from IHS Markit. Please contact economics@ihsmarkit.com.

About IHS Markit (www.ihsmarkit.com)

IHS Markit (Nasdaq: INFO) is a world leader in critical information, analytics and solutions for the major industries and markets that drive economies worldwide. The company delivers next-generation information, analytics and expertise to forge solutions for customers in business, finance and government, improving their operational efficiency and providing deep insights that lead to well-informed, confident decisions. IHS Markit has more than 50,000 business and government customers, including 80 percent of the Fortune Global 500 and the world’s leading financial institutions.

IHS Markit is a registered trademark of IHS Markit Ltd. and/or its affiliates. All other company and product names may be trademarks of their respective owners © 2018 IHS Markit Ltd. All rights reserved.

About PMI

Purchasing Managers’ Index™ (PMI™) surveys are now available for over 40 countries and also for key regions including the eurozone. They are the most closely-watched business surveys in the world, favoured by central banks, financial markets and business decision makers for their ability to provide up-to-date, accurate and often unique monthly indicators of economic trends. To learn more go to www.ihsmarkit.com/products/pmi.

The intellectual property rights to the U.S. Manufacturing PMI™ provided herein are owned by or licensed to IHS Markit. Any unauthorised use, including but not limited to copying, distributing, transmitting or otherwise of any data appearing is not permitted without IHS Markit’s prior consent. IHS Markit shall not have any liability, duty or obligation for or relating to the content or information (“data”) contained herein, any errors, inaccuracies, omissions or delays in the data, or for any actions taken in reliance thereon. In no event shall IHS Markit be liable for any special, incidental, or consequential damages, arising out of the use of the data. Purchasing Managers' Index™ and PMI™ are either registered trade marks of Markit Economics Limited or licensed to Markit Economics Limited. IHS Markit is a registered trademark of IHS Markit Ltd. and/or its affiliates.