HONG KONG--(BUSINESS WIRE)--Oasis Management Company Ltd. (“Oasis”) and the Oasis Investments II Master Fund Ltd. (the “Oasis Fund”), the largest minority shareholder of Japan Asset Marketing Co., Ltd. (8922 JT) (“JAM” or the “Company”), sent a proposal letter to the Board of Directors of JAM on cash flow management, shareholder returns, and governance restructuring. This letter follows on our meeting with and presentation to the Company in February.

We call on JAM to take immediate steps to improve its corporate governance, or, failing that, to privatize the Company at a fair price. All shareholders must be treated equally.

Oasis has been a JAM shareholder since 2017. In early February 2018, we presented proposals to a JAM Board member regarding the Company’s corporate restructuring in an effort to maximize shareholder returns and improve corporate governance.

Oasis has since filed a formal request to the Tokyo District Court to review JAM’s Board meeting minutes on a related party transaction with Don Quijote Holdings Co., Ltd. (“Don Quijote”), the controlling shareholder of JAM with 81.9% ownership. We believe these minutes will provide important and relevant information to clarify whether there were serious corporate governance violations around this transaction.

In response to our engagement, JAM announced on May 8 that two of its external directors – Ms. Mabuchi and Mr. Kaneko – will step down at JAM’s 2018 annual shareholders meeting on June 28.

The following summarizes our letter to JAM’s Board of Directors, which advocates for changes that will serve the interests of all stakeholders, including employees, shareholders, and Don Quijote’s management

JAM’s problems

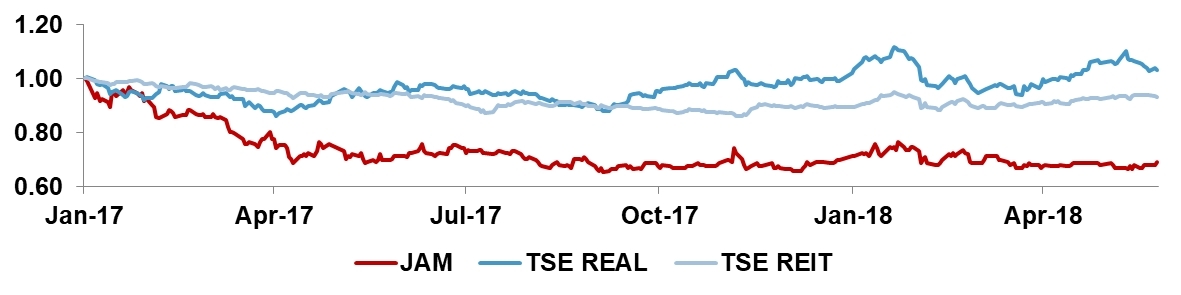

JAM’s stock price has historically underperformed the TSE Real Estate Index and TSE REIT Index. Oasis believes that this underperformance is due to the absence of a shareholder return program, and the Company’s poor corporate governance structure. See Figure 1.

No shareholder return program

Since April 2013, when Don Quijote acquired a substantial ownership of JAM and took on a substantial role in management, JAM has not implemented any shareholder return program or declared any dividends. JAM stated in its latest earnings press release on May 8 that payment of dividend for this fiscal year is subject to its “business performance and financial condition” – implying they will not pay a dividend for fiscal year ending March 2019. The past three years, this same terminology has foreshadowed the absence of any dividend payment to shareholders.

Oasis strongly believes JAM’s rhetoric is incongruous with the reality of its financial performance:

- Their EBITDA for the last five years is positive and steadily growing. See Figure 2.

- Moreover, JAM’s net income attributable to shareholders has continued to grow. See Figure 3.

- As a result of its robust profit generation, the distributable amount of JAM which was negative at the time of Don Quijote’s participation, has surged to JPY23,388 million as of the end of March 2017, and is expected to increase to JPY29,935 million as of the end of March 2018. See Figure 4.

- JAM’s capital adequacy ratio has also significantly improved from 6.3% to 57.7% in the last five years. The current level is higher than the level of most Japanese listed real estate related companies, including major general contractors. It is even at a sufficient level after deducting its entire distributable amount, and would afford the Company a sufficient buffer after issuing a 3% dividend. See Figure 5.

-

Lastly, JAM currently deposits JPY24,944 million of its cash to Don

Quijote in order to participate in its group’s cash management

service. Oasis believes such cash deposited to Don Quijote will be

spent for JAM’s planned capital expenditure over time, as JAM only

holds JPY2,204 million cash on its balance sheet. However, we have

concerns over whether the cash will be used for the mutual interest of

all shareholders, including minority shareholders, as questions remain

regarding JAM’s independence from Don Quijote.

- It appears that there are certain cash needs at Don Quijote, judging from its leverage and the cash needs of its stated growth strategy. JAM’s decision to use the cash custodial services of Don Quijote presents a significant hazard of minority shareholder abuse. We believe that JAM may be influenced by Don Quijote to not withdraw the capital, as Don Quijote would prefer to use the cash for itself, or in ways that do not otherwise serve all of JAM’s shareholders’ interests

Poor Governance

Excessive capital and personnel ties with Don Quijote are key features of JAM’s governance problems. Oasis plans to pursue various options, including legal options, to accelerate JAM’s governance restructuring. JAM’s governance problems include:

- Of the seven directors on JAM’s Board, three of them are external directors. Currently, all of the non-external directors are associates of Don Quijote. Moreover, Ms. Mabuchi, who serves as an external director and member of the audit and supervisory committee, is an auditor of wholly-owned subsidiary of Don Quijote. In summary, more than half of JAM’s Board of Directors and half of its audit and supervisory committee are associates of Don Quijote. These conflicts of interest are of serious concern to JAM’s minority shareholders. See Figure 6.

- As stated above, Oasis has filed a formal request to the Tokyo District Court to review JAM’s Board meeting minutes regarding one particular related party transaction with Don Quijote. Even outside this transaction, there have been numerous business and capital transactions between the two parties in the past few years. Resolutions by three external directors (Ms. Mabuchi, Mr. Kaneko, and Mr. Miyata) were required to carry out these related party transactions, as JAM believed that this step would help them maintain the appearance of fairness. However, once Oasis pointed out the potential conflict of interests in a transaction between JAM and Don Quijote, two out of three of JAM’s external directors (Ms. Mabuchi and Mr. Kaneko) decided to step down. This reinforces our suspicions about JAM and Don Quijote and their poor governance structure.

- Star Asia Partners II (“SAP”), a renowned real estate investment management fund, used to be JAM’s largest minority shareholder, owning 6.31% of the Company in 2016. On June 8, 2016, SAP disclosed a public proposal to JAM focused on improving the Company’s balance sheet, cash flow management and corporate governance. During our discussion with JAM, we confirmed that SAP and JAM had a dialogue at that time, including letters and meetings. It is very unfortunate that to date JAM has not dealt with these issues or expressed their response to SAP publicly. It appears that JAM has simply ignored SAP’s proposals.

Oasis Proposals to JAM’s Board of Directors

JAM’s governance is currently only form over substance. As an independent, listed company, JAM should be managed to maximize the mutual interests of all shareholders, including minority shareholders. Yet, JAM today is managed like a private company for the sole interest of Don Quijote. Oasis strongly believes that JAM should take action to transform its structure in line with global standards for a listed company, or privatize at a fair price.

-

Recommendations for transformation to a sustainable listed company

structure

-

Immediate activation of shareholder return program

- JAM’s business model is amazingly similar to that of REITs. As such, Oasis believes that dividend yield should be used as a metric to determine dividend policy, instead of dividend payout ratio.

- Target dividend yield of at least 3% would be a fair target.

- Share buybacks in this case are less helpful, as they further lower the level of float and liquidity of JAM’s stock.

-

Disciplined cash flow management

- JAM should cap its capital expenditure at the level where it can maintain its dividend yield. However, this will not be applicable if JAM can dramatically improve its EPS by making big investments. In such a case, we would ask the Company to disclose the details of such investments and their pro forma EPS figure.

-

Capital restructuring

- JAM should maintain a certain level of leverage, as cost of equity is generally much higher than cost of debt in Japan. We believe Japanese REITs’ loan-to-value metrics could be used as a reference. JAM should publicly disclose its leverage policy as a commitment.

- Don Quijote should reduce its ownership in JAM to improve JAM’s free float and liquidity. This can be accomplished by Don Quijote either selling its JAM stake in the market (via secondary offering, block trade or dribble-out) or by tendering to JAM’s discount tender offer, targeting JAM stock held by Don Quijote.

- After improving float level and liquidity, Oasis suggests that JAM take steps to be promoted to the Tokyo Stock Exchange 1st section by following the guidance of Japan Exchange Group policy on Mothers. This is the best way to increase the diversity of shareholders.

-

Governance restructuring

- JAM should form a Board of Directors comprised of a majority of truly independent external directors. Such a structure is very common in the U.S. and Europe, and even in Japan the idea is starting to build, as Mitsubishi UFJ Financial Group, Inc., the largest domestic financial institution, decided to adopt this structure from this fiscal year. Companies like JAM with governance flaws should increase the proportion of independent external directors. Such a step would help maintain fairness and avoid conflicts of interest on future related party transactions.

- JAM’s current directors’ compensation structure does not align interests with minority shareholders. Thus, Oasis suggests that JAM adopt performance incentives and distribute stock options.

-

Recommendations for privatization

- In general, there is a low bar in Japan for companies to become privatized when a controlling shareholder exists (Don Quijote owns 81.9% of JAM).

-

Don Quijote should pay a sufficient premium over the current

stock price to privatize JAM.

-

Premiums over the stock price have been paid in every

privatization case in Japan after 2010 where the acquirer

owns more than two-thirds of the voting rights before the

transaction.

- These also include immediate minority squeeze out cases, which were exercised in the form of Demand for the Sale of Shares (“Kabushiki Uriwatashi Seikyu”) and Acquisition of Class Shares subject to Wholly Call (“Zenbu Shutoku Joko-tsuki Futsu Kabushiki Shutoku”).

- Moreover, Uny Co., Ltd., a Japanese major GMS company with 40% ownership held by Don Quijote, has paid a premium over the stock price to privatize UCS Co., Ltd. even though Uny Co. owned 81.4% before the transaction.

-

Premiums over the stock price have been paid in every

privatization case in Japan after 2010 where the acquirer

owns more than two-thirds of the voting rights before the

transaction.

-

After privatization, Don Quijote should IPO JAM’s assets in a

REIT structure. To achieve this, Don Quijote should set up a

new REIT entity, inject JAM’s assets into the entity, and

subsequently launch the IPO for that entity.

- This would enable Don Quijote’s property acquisition and property management business to obtain flexibility in capital structure planning and use of capital markets, together with the tax benefit on its profit.

-

Immediate activation of shareholder return program

We will continue our effort to engage with JAM’s Board of Directors in a collaborative and positive dialogue to improve JAM’s corporate value.

For all inquiries, please contact Taylor Hall at thall@hk.oasiscm.com.

***

Oasis Management Company Ltd. manages private investment funds focused on opportunities in a wide array of asset classes across countries and sectors. Oasis was founded in 2002 by Seth H. Fischer, who leads the firm as Chief Investment Officer. More information about Oasis is available at https://oasiscm.com. Oasis has adopted the Japan FSA’s “Principles of Responsible Institutional Investors” (a/k/a Japan Stewardship Code) and in line with those principles, Oasis monitors and engages with our investee companies.