")

NEWARK, Del.--(BUSINESS WIRE)--Confused about how the new federal tax act affects higher education-related tax deductions and credits? Sallie Mae — the nation’s saving, planning, and paying for college company — can help college students, graduate students, and families sort through what has changed and what has stayed the same.

“There was a lot of back-and-forth about higher education tax benefits as the new tax law was being finalized, so taxpayers might not realize that, ultimately, very little changed, and most of what did change does not apply to 2017 tax returns,” said Martha Holler, senior vice president, Sallie Mae. “Available deductions and credits for expenses like tuition, fees, and interest paid on student loans range from $2,000 to $4,000, depending on income, so it’s worth taking the time to investigate whether you qualify.”

Here is a quick look at what taxpayers need to know for their 2017 tax returns:

-

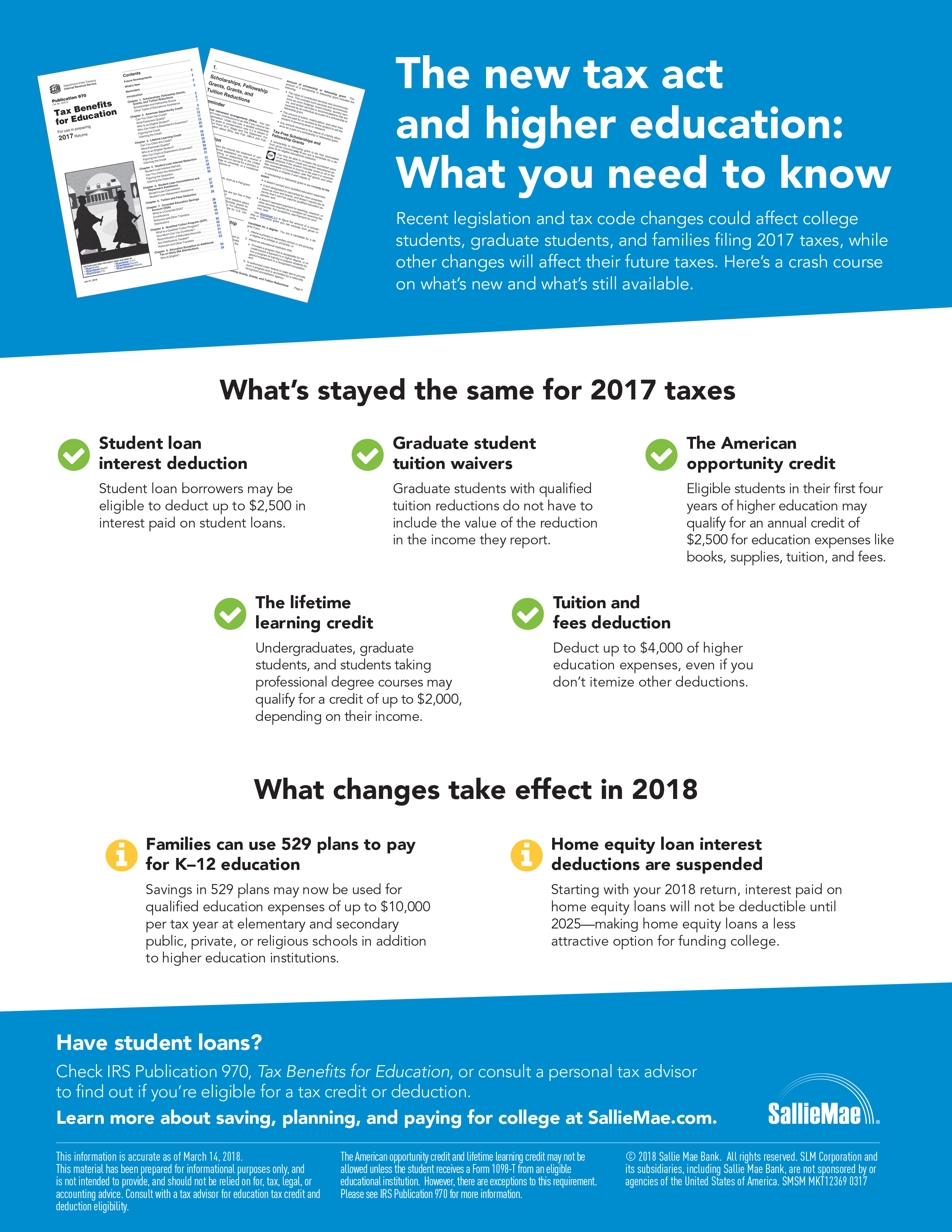

Tuition and fees deduction. Up to $4,000 in higher education

expenses can be deducted as an adjustment to taxable income, and the

deduction can be claimed even if the filer does not itemize other

deductions. Individuals with a modified adjusted gross income of up to

$80,000 and those with a joint modified adjusted gross income of up to

$160,000 may qualify for this deduction.

Initially eliminated, the tuition and fees deduction was restored retroactively by the Bipartisan Budget Act on Feb. 9. Taxpayers who already filed their 2017 federal tax return and now wish to claim the tuition and fee deduction may file an amended return. - Student loan interest deduction. Taxpayers with federal or private student loans may be eligible to deduct up to $2,500 of interest as an adjustment to taxable income. The student must be enrolled at least half time in a program leading to a degree or other recognized educational credential. Single filers with a modified adjusted gross income (MAGI) of between $65,000 and $80,000, and joint filers with a MAGI between $135,000 and $165,000 may qualify for this deduction.

-

The American opportunity tax credit. Students enrolled at least

half time in a program leading to a degree or other recognized

educational credential may be eligible for a tax credit of up to

$2,500 per year in tuition, enrollment fees, and course materials

expense during the student’s first four years of higher education.

Single filers with a MAGI of up to $90,000 and married filers with a

MAGI up to $180,000 may qualify for this credit.

New this year: To claim the American opportunity tax credit, filers must provide the educational institution’s employer identification number. - The lifetime learning credit. Students do not need to be in a degree program to qualify for this credit. Up to $2,000 per year in expenses related to all years of post-secondary education, as well as courses to acquire or improve job skills, may qualify for the credit, and there is no limit on the number of years it may be claimed. Single filers with a MAGI of less than $66,000 or joint filers with a MAGI of less than $132,000 may be eligible for this credit. The credit is reduced gradually for single filers making more than $56,000, and for joint filers making more than $112,000.

- Tax benefit limitations. Either the American opportunity credit or the lifetime learning credit may be claimed in one tax year, but not both. In addition, taxpayers may not claim both the tuition and fees deduction and a tax credit in the same tax year.

- Tuition waivers for graduate students. These waivers remain tax-free; grad students who receive qualified tuition reductions do not have to report the value of the reduction as taxable income.

Here is a quick look at changes that affect 2018 tax returns:

- Expanded eligibility for 529 savings plans. Beginning Jan. 1, 2018, 529 plan savings may be used for qualified education expenses of up to $10,000 per student per year at elementary and secondary public, private, or religious schools.

- Interest paid on home equity loans is no longer tax-deductible. The home equity loan interest deduction has been suspended until 2025, making these loans a less attractive option for funding college.

Information in this release is accurate as of March 14, 2018. It is not intended to provide, nor should it be relied on, for tax, legal, or accounting advice. For more information on eligibility for higher education tax deductions and credits, consult IRS Publication 970, “Tax Benefits for Higher Education,” or a personal tax advisor.

Find additional information on saving, planning, and paying for college at SallieMae.com.

Sallie Mae (Nasdaq: SLM) is the nation’s saving, planning, and paying for college company. Whether college is a long way off or just around the corner, Sallie Mae offers products that promote responsible personal finance, including private education loans, Upromise rewards, scholarship search, college financial planning tools, and online retail banking. Learn more at SallieMae.com. Commonly known as Sallie Mae, SLM Corporation and its subsidiaries are not sponsored by or agencies of the United States of America.