")

NEW YORK--(BUSINESS WIRE)--The new federal tax reform law makes substantial changes to the U.S. tax code and will have a major impact on Americans’ financial plans. While most of the attention has been on adjustments to tax brackets and the doubling of the standard deduction, the new law is a 1,097-page document representing the most substantial revision to the U.S. tax code in more than 30 years.

A recent survey of affluent Americans, conducted before the Tax Cuts and Jobs Act of 2017 was signed into law, found that three-in-five (63 percent) are likely to adjust their financial plans according to changes in tax policy. The survey, conducted online by The Harris Poll for the American Institute of CPAs (AICPA), found that over half of affluent Americans (53 percent) believe that working with an advisor, such as a CPA financial planner, with substantial tax expertise could make them more likely meet their financial goals.

“Effective financial planning takes an individual’s personal situation into account, as well as the current laws and overall economic climate,” said Jeannette Koger, CPA, CGMA, vice president of advisory services and credentialing at the Association of International Certified Professional Accountants. “The newly enacted tax legislation is going to have an impact on the financial plans of tens of millions of Americans. With their foundational knowledge in tax, CPA financial planners are best positioned to understand the consequences of the new law and work with clients to ensure that their financial plans are tax efficient and designed to meet their long-term goals.”

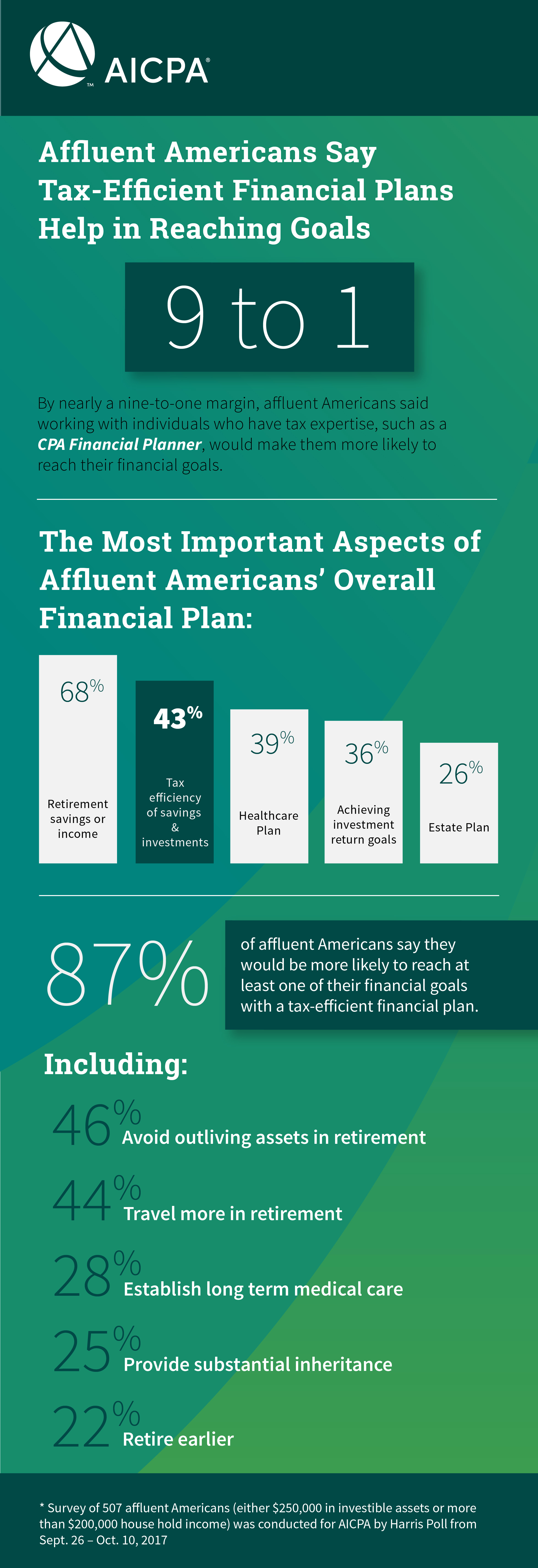

The survey found that affluent adults understand the value of a financial planner with substantial tax expertise. By nearly a nine-to-one ratio, (53 percent more likely versus 6 percent less likely) affluent Americans say working with individuals, such as a CPA financial planner, would make them more likely to reach their financial goals.

What’s more, ‘tax efficiency of savings and investment’ (43 percent) was the second most cited important aspect of their financial plan. That was behind only ‘retirement savings and income’ (68 percent), but ahead of ‘healthcare plan’ (39 percent), ‘achieving investment return goals’ (36 percent), and ‘estate plan’ (26 percent). A tax efficient plan utilizes investment vehicles, such as municipal bonds or 401(k)s, that grow in a manner that allows the taxpayer to maximize the amount of income they keep. While affluent Americans recognize tax efficiency as a crucial aspect of their financial plan, on average, only 43.5 percent of affluent adults’ total investments and retirement savings are in tax qualified accounts or tax favored investments.

“Given the sharp bite taxes can take out of returns, the importance of structuring investments and income-generating savings in a tax-efficient manner cannot be overstated,” said Andrea Millar, CPA/PFS, director of the AICPA’s Personal Financial Planning Division. “However, taxes have an impact on all aspects of a financial plan, from retirement to medical care to charitable giving. CPA financial planners work with their clients to understand their financial goals and structure their financial plan in a tax-optimized manner accordingly.”

Affluent adults see a connection between tax-efficient financial plans and prosperity. Eighty-seven percent say they would be more likely to reach at least one of their financial goals with a tax-efficient financial plan. The most frequently cited goal they would be more likely to reach was avoiding outliving assets in retirement (46 percent). Establishing their long term medical care (28 percent), retiring earlier (22 percent), and delaying taking social security in retirement (21 percent) were also among the goals improved by tax-efficient financial planning.

Many affluent Americans saw the benefit of a tax-efficient financial plan for their families as well, with one-in-four (25 percent) saying they would be likely to provide a more substantial inheritance for their children or grandchildren and 18 percent stating they’d have an increased likelihood of paying for their children’s college education. Affluent Americans see potential lifestyle improvements with tax-efficient financial planning as well, including travelling more in retirement (44 percent) and purchasing a vacation home (12 percent).

Over the course of a career, tax-efficient financial planning can have a significant impact on an individual’s nest egg in retirement. The vast majority of affluent adults agreed, with 90 percent saying that effective tax planning would be either very or somewhat important to their overall financial well-being in retirement.

The following tips are among the strategies CPA financial planners recommend their clients consider based on the new tax law:

- Charitable Contributions – For Americans who are regularly making charitable gifts, it may be more advantageous to place a few years’ worth of contributions in a Donor Advised Fund. Bunching their contributions together, rather than contributing on an annual basis, may put them over the standard deduction hurdle and help them to receive a greater tax benefit for their charitable giving.

- Home Equity Loan or Line of Credit – If you have a home equity loan or line of credit with a balance, you may want to accelerate the payoff. If the funds were used for anything other than to buy or substantially improve your home, the interest you pay will no longer be deductible as mortgage interest. Which means you could be paying a higher effective rate than you were in prior years when the interest reduced your taxable income. However, financial decisions should not be based on the tax impact alone. Consideration must be given to how the loan will be paid off to ensure it is a wise overall move.

- 20% Deduction Against Qualified Business Income – American business owners should consider whether the current structure of their business continues to make sense, as this deduction can be significant for businesses that qualify. Record keeping and documentation is more important than ever, as wages paid and cost basis (purchase price) information will be factored into the calculation.

- Lifetime Gifting – On the transfer tax front, the estate, gift, and generation skipping transfer tax exemptions doubled to $10,000,000, adjusted for inflation. CPA financial planners can discuss the trade-offs and run the analysis of whether it makes sense to gift assets during life and remove the future appreciation for their estate or retain the assets until death and receive a step-up in cost basis.

- Estate Plans – If a taxpayer’s documents were drafted when the transfer tax exemption amount was $5 million, it may have made sense to fully fund an exemption trust and pass the remainder to the beneficiary. However, with the exemption increased to $10 million (adjusted for inflation), it may be that the entire value of the estate will be transferred to the exemption trust, with nothing passing to the beneficiary. This could present a problem, as the beneficiary may not want to have all the funds tied up in trust.

Survey Methodology

This survey was conducted online by The Harris Poll for AICPA within the United States from September 26 to October 10, 2017, among 507 affluent U.S. adults aged 18+, who either have $250,000 in investable assets or more than $200,000 house hold income. Results are weighted to bring them into line with their actual proportions in the population.

About the AICPA’s PFP Division

The AICPA’s Personal Financial Planning (PFP) Section is the premier provider of information, tools, advocacy, and guidance for CPAs who specialize in providing estate, tax, retirement, risk management, and investment planning advice to individuals, families, and business owners. The primary objective of the PFP Section is to support its members by providing resources that enable them to perform valuable PFP services in the highest professional manner.

CPA financial planners are held to the highest ethical standards and are uniquely able to integrate their extensive knowledge of tax and business planning with all areas of personal financial planning to provide objective and comprehensive guidance for their clients. The AICPA offers the Personal Financial Specialist (PFS) credential exclusively to CPAs who have demonstrated their expertise in personal financial planning through testing, experience and learning, enabling them to gain competence and confidence in PFP disciplines.

About the American Institute of CPAs

The American Institute of CPAs (AICPA) is the world’s largest member association representing the CPA profession, with more than 418,000 members in 143 countries, and a history of serving the public interest since 1887. AICPA members represent many areas of practice, including business and industry, public practice, government, education and consulting. The AICPA sets ethical standards for its members and U.S. auditing standards for private companies, nonprofit organizations, federal, state and local governments. It develops and grades the Uniform CPA Examination, offers specialized credentials, builds the pipeline of future talent and drives professional competency development to advance the vitality, relevance and quality of the profession.

The AICPA maintains offices in New York, Washington, DC, Durham, NC, and Ewing, NJ.

Media representatives are invited to visit the AICPA Press Center at www.aicpa.org/press

About the Association of International Certified Professional Accountants

The Association of International Certified Professional Accountants (the Association) is the most influential body of professional accountants, combining the strengths of the American Institute of CPAs (AICPA) and The Chartered Institute of Management Accountants (CIMA) to power opportunity, trust and prosperity for people, businesses and economies worldwide. It represents 650,000 members and students in public and management accounting and advocates for the public interest and business sustainability on current and emerging issues. With broad reach, rigor and resources, the Association advances the reputation, employability and quality of CPAs, CGMAs and accounting and finance professionals globally.

About the Harris Poll:

The Harris Poll is one of the longest-running surveys in the U.S. tracking public opinion, motivations and social sentiment since 1963 that is now part of Harris Insights & Analytics, a global consulting and market research firm that strives to reveal the authentic values of modern society to inspire leaders to create a better tomorrow. We work with clients in three primary areas; building twenty-first-century corporate reputation, crafting brand strategy and performance tracking, and earning organic media through public relations research. Our mission is to provide insights and advisory to help leaders make the best decisions possible. To learn more, please visit www.harrisinsights.com.