Newsroom

Sorted by: Latest

-

First Trust Global Funds PLC UK Regulatory Announcement: Net Asset Value(s)

LONDON--(BUSINESS WIRE)-- Funds Date TIDM ISIN Code Shares in Issue Currency Net Asset Value NAV/per Share First Trust Nasdaq Clean Edge Global Water UCITS ETF 26.05.2026 H2O LN IE000Q8F0M81 600,002.00 USD 11,975,114.46 19.959 ...

-

First Trust Global Funds PLC UK Regulatory Announcement: Net Asset Value(s)

LONDON--(BUSINESS WIRE)-- Funds Date TIDM ISIN Code Shares in Issue Currency Net Asset Value NAV/per Share First Trust Vest U.S. Equity Buffer UCITS ETF - October 26.05.2026 FOCT.LN IE0004X8KUG5 100,002.00 USD 2,899,417.91 28.994 ...

-

Monro Announces Strategic Alternatives Review to Maximize Shareholder Value

FAIRPORT, N.Y.--(BUSINESS WIRE)--Monro, Inc. (Nasdaq: MNRO), a leading provider of automotive repair and tire services, today announced that its Board of Directors (the “Board”) has initiated a review of strategic alternatives to maximize shareholder value. In consultation with its financial and legal advisors, the Board will evaluate a broad range of alternatives, including but not limited to asset sales, refinancing of the business, strategic acquisitions and operational improvements, or the...

-

Pace Raises $46 Million Series B to Build the Next Century of Insurance

NEW YORK--(BUSINESS WIRE)--Pace, the AI operations partner for the world’s leading insurers, today announced its $46 million Series B, co-led by Thrive Capital and Sequoia Capital, with participation from Emergence Capital and Pruven Capital. Pace partners with several public insurers and brokers to provide its cutting-edge technology, including The Mutual Group, Newfront, Prudential, and WTW. Since launching last year, Pace has autonomously completed more than a quarter of a million critical i...

-

Valvoline Instant Oil Change℠ Ranked No. 1 In Automotive Franchises

LEXINGTON, Ky.--(BUSINESS WIRE)--Valvoline Inc. (NYSE: VVV), the quick, easy, trusted leader in preventive automotive maintenance, has been recognized as No. 1 in the automotive franchise category in Entrepreneur magazine’s 2026 ranking. The new ranking recognizes the Top 10 Franchises in Every Industry across major industry categories. Valvoline Instant Oil Change earned its top ranking by building a strong franchise system based on a proven operating model, broad brand awareness, and a commit...

-

lululemon Enters into Cooperation Agreement with Chip Wilson; Laura Gentile and Marc Maurer to Join Company’s Board of Directors

VANCOUVER, British Columbia--(BUSINESS WIRE)--lululemon athletica inc. (NASDAQ:LULU) today announced that it has entered into a cooperation agreement with Dennis J. “Chip” Wilson, who owns approximately 8.7% of the company’s outstanding common stock. In connection with the agreement, Laura Gentile, former Chief Marketing Officer of ESPN, and Marc Maurer, former Co-Chief Executive Officer of On, will join the company’s Board of Directors following the company’s 2026 Annual Meeting of Shareholder...

-

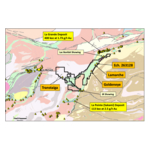

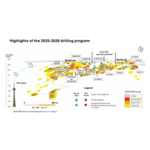

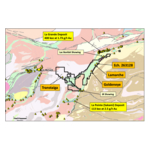

RPX Gold’s Drilling Extends Near Surface Gold Mineralization and Along Strike

TORONTO--(BUSINESS WIRE)--RPX Gold Inc. (“RPX Gold” or the “Company”) (TSXV: RPX. OTCQB: RDEXF) is pleased to announce gold assay results from its 2025-2026 drilling program at its Wawa Gold Project, Ontario. The drilling program was designed to confirm the continuity of, and potentially extend, near surface gold mineralization in the area of the open pits defined in the 2026 Preliminary Economic Assessment (“2026 PEA”). These new assay results will be included in the updated mineral resource e...

-

Verastem Oncology to Present at Jefferies Healthcare Conference

BOSTON--(BUSINESS WIRE)--Verastem Oncology (Nasdaq: VSTM), a biopharmaceutical company committed to advancing new medicines for patients with RAS/MAPK pathway-driven cancers, today announced that its management team is scheduled to participate in a fireside chat at the Jefferies Global Healthcare Conference on Wednesday, June 3, 2026, at 8:10 am ET in New York. A live webcast of the fireside chat can be accessed under “Events & Presentations” on the Company’s website at www.verastem.com. A...

-

Visible Gold Expands Exploration Portfolio With Acquisition of 250 KM² District-Scale Sakami Gold Project

ROUYN-NORANDA, Québec--(BUSINESS WIRE)--Visible Gold Mines Inc. ("Visible Gold" or the "Company") (TSXV: VGD) (FRANKFURT: 3V41) is pleased to announce that it has entered into an arm's-length agreement dated May 26, 2026 (the "Agreement") with Morocco Strategic Minerals Corp. (TSXV: MCC) (the "Vendor") to acquire a 100% interest in the Sakami property ("Sakami" or the "Property") located in the James Bay Territory of Québec. CEO QUOTE Jean-Marc Lacoste, President and CEO of Visible Gold stated:...

-

Visible Gold renforce son portefeuille d’exploration avec l’acquisition du projet aurifère Sakami couvrant 250 km²

ROUYN-NORANDA, Québec--(BUSINESS WIRE)--Visible Gold Mines Inc. (« Visible Gold » ou la « Société ») (TSXV: VGD) (FRANCFORT: 3V41) est heureuse d’annoncer qu’elle a conclu une entente sans lien de dépendance datée du 26 mai 2026 (l’« entente ») avec Morocco Strategic Minerals Corp. (TSXV: MCC) (le « vendeur ») afin d’acquérir une participation de 100 % dans la propriété Sakami (« Sakami » ou la « propriété »), située dans le territoire de la Baie-James, au Québec. CITATION DU CHEF DE LA DIRECTI...