Newsroom

Sorted by: Latest

-

Xsolla SDK现已面向全球游戏开发者开放

洛杉矶--(BUSINESS WIRE)--(美国商业资讯)-- 致力于帮助游戏开发者发布、拓展游戏业务并变现的全球视频游戏商务公司Xsolla今日宣布推出Xsolla SDK,这是一款统一的跨平台软件开发工具包,将Xsolla的PC、移动和网页盈利工具整合到一个下载包中。将于2026年游戏开发者大会(GDC)上正式发布的Xsolla SDK为开发者内置了支付、登录、目录和积分墙(Offerwall)等功能,开发者只需配置一次定价和库存,即可部署至全部所支持的平台,而无需重复配置。 Xsolla依托专攻游戏的业界顶尖、成熟的技术基础,致力于提供全方位解决方案,助力开发者实现跨平台盈利。Xsolla SDK凝聚了公司二十年来为游戏开发者打造支付和盈利工具的丰富经验,累计处理支付总额超过100亿美元,其支付基础设施深受全球前100名最畅销游戏中超过60%的信任。Xsolla深厚的经验涵盖了数千款游戏、各种监管环境以及平台更迭,现通过单一整合即可惠及各种规模的开发者。 “游戏开发者需要能够在所有平台上无缝协作,且不会增加复杂性的工具,”Xsolla总裁Chris Hewish表示,“Xsol...

-

Xsolla SDK現已對全球遊戲開發者開放

洛杉磯--(BUSINESS WIRE)--(美國商業資訊)-- 協助遊戲開發者發行遊戲並使之成長變現的全球性商務公司Xsolla今日宣布推出Xsolla SDK,這是一款統一的跨平台軟體開發套件,將Xsolla的PC、行動和網頁獲利工具整合到一次下載中。將於2026年遊戲開發者大會(GDC)上正式發布的Xsolla SDK為開發者內建了支付、登入、目錄和積分牆(Offerwall)等功能,開發者只需配置一次定價和庫存,即可部署至全部所支援的平台,而無需重複配置。 Xsolla依托專攻遊戲的業界頂尖、成熟的技術基礎,致力於提供全方位解決方案,協助開發者實現跨平台獲利。Xsolla SDK凝聚了公司二十年來為遊戲開發者打造支付和盈利工具的豐富經驗,累計處理支付總額超過100億美元,其支付基礎設施深受全球前100名最暢銷遊戲中超過60%的信任。Xsolla深厚的經驗涵蓋了數千款遊戲、各種監理環境以及平台更迭,現在透過單一整合即可惠及各種規模的開發者。 「遊戲開發者需要能夠在所有平台上無縫協作,且不會增加複雜性的工具,」Xsolla總裁Chris Hewish表示,「Xsolla長期致力於解...

-

Citibank UK Regulatory Announcement: FRN Variable Rate Fix

LONDON--(BUSINESS WIRE)-- Re: TSB BANK plc. GBP 500,000,000.00 MATURING: 11-Sep-2029 ISIN: XS2898163568 PLEASE BE ADVISED THAT THE INTEREST RATE FOR THE PERIOD 11-Dec-2025 TO 11-Mar-2026 HAS BEEN FIXED AT 4.32 PCT DAY BASIS: ACTUAL/365(FIX) INTEREST PAYABLE VALUE 11-Mar-2026 WILL AMOUNT TO: GBP 5,329,627.40 PER GBP 500,000,000.00 DENOMINATION ...

-

SDK da Xsolla agora disponível para desenvolvedores de jogos em todo o mundo

LOS ANGELES--(BUSINESS WIRE)--A Xsolla, empresa global de comércio de videogames que ajuda desenvolvedores a lançar, expandir e monetizar seus jogos, anunciou hoje a disponibilidade do SDK da Xsolla, um kit de desenvolvimento de software unificado e multiplataforma que consolida as ferramentas de monetização para PC, dispositivos móveis e web da empresa em um único download. Com lançamento previsto para o GDC Festival of Games 2026, o SDK da Xsolla apresenta integrações nativas de Pagamentos, L...

-

Citibank UK Regulatory Announcement: FRN Variable Rate Fix

LONDON--(BUSINESS WIRE)-- Re: The Toronto-Dominion Bank (Covered Bonds) GBP 800,000,000.00 MATURING: 11-Jun-2029 ISIN: XS2838372113 PLEASE BE ADVISED THAT THE INTEREST RATE FOR THE PERIOD 11-Dec-2025 TO 11-Mar-2026 HAS BEEN FIXED AT 4.39 PCT DAY BASIS: ACTUAL/365(FIX) INTEREST PAYABLE VALUE 11-Mar-2026 WILL AMOUNT TO: GBP 8,665,486.03 PER GBP 800,000,000.00 DENOMINATION ...

-

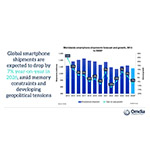

Omdia: Global Smartphone Shipments to Fall 7% in 2026 Amid Memory Constraints and Geopolitical Pressures

LONDON--(BUSINESS WIRE)--Global smartphone shipments are forecast to decline by around 7% year-on-year in 2026 according to Omdia’s latest outlook. This projection based on Q1 memory price assumptions, which indicate that pricing pressure and constrained supply will begin to ease in the second half of the year. The global smartphone market will face significant challenges in 2026 as tightening memory supply and elevated pricing place increasing cost pressures for vendors. Memory now accounts fo...

-

Zestaw Xsolla SDK teraz dostępny dla twórców gier na całym świecie

LOS ANGELES--(BUSINESS WIRE)--Xsolla, globalna firma prowadząca działalność w obszarze handlu grami wideo, która pomaga twórcom wprowadzać i rozwijać gry oraz czerpać z nich dochody, poinformowała dzisiaj o udostępnieniu Xsolla SDK – ujednoliconego, możliwego do zastosowania w ramach każdej platformy zestawu dla twórców oprogramowania łączącego opracowane przez firmę narzędzia służące czerpaniu dochodów za pomocą komputerów, urządzeń mobilnych i środowisk internetowych w jednym pakiecie materia...

-

Citibank UK Regulatory Announcement: FRN Variable Rate Fix

LONDON--(BUSINESS WIRE)-- Re: Nationwide Building Society (N Covered Bonds) GBP 750,000,000.00 MATURING: 08-Jun-2028 ISIN: XS2633544601 PLEASE BE ADVISED THAT THE INTEREST RATE FOR THE PERIOD 08-Dec-2025 TO 09-Mar-2026 HAS BEEN FIXED AT 4.27 PCT DAY BASIS: ACTUAL/365(FIX) INTEREST PAYABLE VALUE 09-Mar-2026 WILL AMOUNT TO: GBP 10.64 PER GBP 1,000.00 DENOMINATION ...

-

Hercules Capital Receives a BBB (high) Affirmed Investment Grade Corporate and Credit Rating from Morningstar DBRS

SAN MATEO, Calif.--(BUSINESS WIRE)--Hercules Capital, Inc. (NYSE: HTGC) (“Hercules,” “Hercules Capital,” or the “Company”), the largest and leading specialty financing provider to innovative venture, growth and established stage companies backed by some of the leading and top-tier venture capital and select private equity firms, today announced that Morningstar DBRS (“DBRS”) has affirmed Hercules’ investment grade corporate and credit rating of BBB (high). DBRS issued a statement announcing the...

-

Xsolla SDK nu wereldwijd beschikbaar voor gameontwikkelaars

LOS ANGELES--(BUSINESS WIRE)--Xsolla, een wereldwijd bedrijf in de videogamehandel dat ontwikkelaars helpt bij het lanceren, ontwikkelen en monetiseren van hun games, kondigt vandaag de beschikbaarheid aan van Xsolla SDK, een uniforme, platformonafhankelijke softwareontwikkelingskit die de tools voor pc-, mobiele en webmonetisatie van het bedrijf in één download combineert. De Xsolla SDK, die wordt gelanceerd tijdens het GDC Festival of Games 2026, introduceert ingebouwde integratie met betalin...