Newsroom

Sorted by: Latest

-

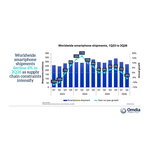

Omdia:2026年第二季度全球智能手机出货量同比下降6%,供应端压力正在重塑市场格局

伦敦--(BUSINESS WIRE)--(美国商业资讯)-- 根据 Omdia 最新发布的数据,2026年第二季度全球智能手机出货量同比下降6%,降至2.72亿部。 此前,2026年第一季度受提前备货需求带动,市场表现较强,而第二季度则进入存储器成本周期的调整阶段。持续高企的存储价格扰乱了供应,推高了元器件成本,迫使厂商重新思考定价策略、产品组合和渠道战略。 市场呈现出明显的两极分化态势,厂商的表现越来越取决于其规模、供应链韧性、定价能力以及在入门级智能手机市场的布局。 各大厂商表现 三星保持全球份额第一地位,出货量达6050万部(同比增长5%),市场份额为22%。三星垂直整合的存储业务帮助其比竞争对手更有效地应对元器件短缺。Galaxy S26系列的延迟发布也将高端需求转移到第二季度,同时三星在入门级市场获得了额外份额,因为中国竞争对手缩减了产品线并提高了价格。 苹果实现了有史以来最强劲的第二季度表现,出货量达5510万部(同比增长23%),在传统淡季创下20%的市场份额纪录。渠道合作伙伴在预期价格上涨和iPhone 18系列将以更高价位发布的背景下,大幅增加了基础款iPhone...

-

Expereo acelera su estrategia de crecimiento en EE. UU. con el nombramiento de Margi Shaw como presidenta independiente

RESTON, Va.--(BUSINESS WIRE)--Expereo, proveedor líder de servicios gestionados de red (NaaS), anunció hoy la siguiente fase de crecimiento de su consolidado negocio en Estados Unidos, donde ya ofrece a las empresas estadounidenses un único socio para sus redes, tanto a nivel nacional como en todos los mercados internacionales en los que operan. Para respaldar esta estrategia, la compañía ha nombrado a Margi Shaw presidenta independiente para las Américas. Las empresas estadounidenses con opera...

-

Expereo acelera estratégia de crescimento nos EUA com a nomeação de Margi Shaw como presidente independente

RESTON, Va.--(BUSINESS WIRE)--A Expereo, provedora líder de Rede como Serviço (NaaS) gerenciada, anunciou hoje a próxima fase de crescimento para seus negócios consolidados nos EUA, onde já oferece às empresas com sede nos EUA um único parceiro para suas redes, tanto no país de origem quanto em todos os mercados internacionais em que atuam. Para apoiar essa estratégia, a empresa nomeou Margi Shaw como presidente independente para as Américas. Empresas americanas com operações internacionais ger...

-

Tanium zeigt auf der Black Hat USA 2026 neue autonome Funktionen, mit denen Sicherheitsteams KI-basierten Bedrohungen zuvorkommen

EMERYVILLE, Kalif.--(BUSINESS WIRE)--Tanium, führend bei Autonomer IT , hat heute eine Reihe von autonomen Sicherheitsfunktionen für die Tanium Autonomous IT Platform auf der Black Hat USA 2026 vorgestellt. Diese Funktionen decken die Bereiche agentenbasierte KI, Exposure Management und Security Operations ab. Sie versetzen IT- und Sicherheitsverantwortliche in die Lage, einer durch KI beschleunigten Bedrohungslandschaft einen Schritt voraus zu sein, ohne dabei die Kontrolle zu verlieren. „Auf...

-

Tanium présente des capacités de sécurité autonome au Black Hat USA 2026 pour permettre aux opérateurs de garder une longueur d'avance sur les menaces accélérées par l'IA

EMERYVILLE, Californie--(BUSINESS WIRE)--Tanium, leader de l’autonomous IT, annonce aujourd’hui une série de nouvelles capacités de sécurité autonomes disponible sur l’ensemble de la plateforme Tanium Autonomous IT au Black Hat USA 2026. Couvrant l'IA agentique, la gestion de l'exposition et les opérations de sécurité, les capacités permettent aux opérateurs informatiques et de sécurité de conserver une longueur d'avance sur un écosystème de menaces accéléré par l'IA, en toute sécurité, sans pe...

-

UMC Reports Sales for July 2026

TAIPEI, Taiwan--(BUSINESS WIRE)--United Microelectronics Corporation (NYSE: UMC; TWSE: 2303) (“UMC”), today reported unaudited net sales for the month of July 2026. Revenues for July 2026 Period 2026 2025 Y/Y Change Y/Y (%) July 23,844,045 20,040,049 3,803,996 18.98% Jan.-July 153,614,609 136,656,663 16,957,946 12.41% (*) All figures in thousands of New Taiwan Dollars (NT$), except for percentages. (**) All figures are consolidated Additional information about UMC is available on the web at htt...

-

Centrica Energy und Zelestra unterzeichnen Tolling-Vertrag für 297-MWh-Batteriespeicher in Deutschland

BERLIN--(BUSINESS WIRE)--Zelestra wird den Speicher errichten und betreiben, während Centrica Energy die vertraglich gesicherte Kapazität über seinen Multi-Market-Optimierungsansatz handeln und optimieren wird. Der Baubeginn ist für 2027 vorgesehen; der vollständige Betrieb wird in der zweiten Jahreshälfte 2028 erwartet. Centrica Energy und Zelestra haben einen physischen Tolling-Vertrag über 99 MW / 297 MWh Batteriespeicherkapazität für Zelestras Batteriespeicherprojekt Hilgermissen in Nieders...

-

Centrica Energy and Zelestra Sign Tolling Agreement in Germany to Enable 297 MWh Standalone BESS

BERLIN--(BUSINESS WIRE)--Centrica Energy and Zelestra have signed a physical tolling agreement for 99 MW / 297 MWh of battery storage capacity at Zelestra’s Hilgermissen BESS project, located in Lower Saxony, Germany. Under the agreement, Zelestra will develop, construct and own the battery storage project, building on their experience in delivering major projects in other markets and their extensive pipeline across Europe. Engineering and procurement activities will be completed this year lead...

-

CoStar Data Shows Strong Prelet Activity Driving UK Lab Space Demand to a Record High

LONDON--(BUSINESS WIRE)--GSK’s landmark life sciences prelet drove UK laboratory space demand to a new record, according to data from CoStar, a global leading provider of online real estate marketplaces, information and analytics in the property markets. Rolling four-quarter take-up exceeded 1.2 million square feet in Q3 2026, with two months still remaining, following the 300,000-square-foot prelet at Cambridge Biomedical Campus. In July, Prologis received planning approval for another Phase 2...

-

Great Britain Leads Europe’s FMCG Inflation as NIQ Launches New Inflation Barometer

LONDON--(BUSINESS WIRE)--NIQ (NYSE: NIQ) today launches its new EU5 FMCG Inflation Barometer - a monthly tracker across five Western Europe markets – France, Great Britain, Germany, Italy and Spain – designed to help retailers, manufacturers and the media understand how inflation is evolving across Europe’s largest grocery markets and how shoppers are responding. The first edition of the Barometer reveals that while inflation across Europe’s FMCG sector remains relatively contained overall, sig...