")

BOSTON--(BUSINESS WIRE)--Fidelity Investments® − America’s No. 1 provider of 401(k) plans and Individual Retirement Accounts (IRA)1 − today announced its average 401(k) balance is $88,600 at the end of the first quarter 2014, up more than 9 percent from $80,900 one year earlier2. The balance is up 92 percent over the 5 years since the first quarter of 2009 – the market low of the economic downturn – when it was $46,200. For pre-retirees age 55 and older, the average balance is $165,000. In addition, Fidelity Individual Retirement Account (IRA)3 average balances rose to $89,500, up 11 percent from $80,500 one year earlier.

“It’s encouraging to see such positive savings results for millions of Americans in the five years since the market downturn, both in 401(k)s and IRAs,” said Julia McCarthy, executive vice president of Workplace Investing at Fidelity. “But even with this quarter’s positive news, there is still more that can be done to improve outcomes in retirement. That’s why Fidelity continuously develops innovative tools and programs to help individuals learn how to invest and determine how much to save so they can create the future they envision.”

It’s Not Just When but How You Start Saving that Makes a Huge Difference

For many American workers, a 401(k) will provide the bulk of their retirement paycheck. So evaluating the choices employers and their employees make at enrollment could really make a difference in retirement income. Overall, 26 percent of employers automatically enroll employees in their retirement plan4. But getting employees enrolled isn’t enough. Helping them save more is the true challenge.

Fidelity’s average employee deferral rate is 8 percent. Yet for those who were auto enrolled into a 401(k) plan, their average deferral rate is only 5 percent, in part because 73 percent of employers enroll employees at 3 percent or less. Even with an average employer contribution of 4.4 percent, the savings rate for many auto enrolled employees falls below Fidelity’s recommended annual total savings rate of 10-15 percent5. According to Fidelity, in order to achieve adequate retirement income, it is important that both employers and employees play a role in closing this savings gap.

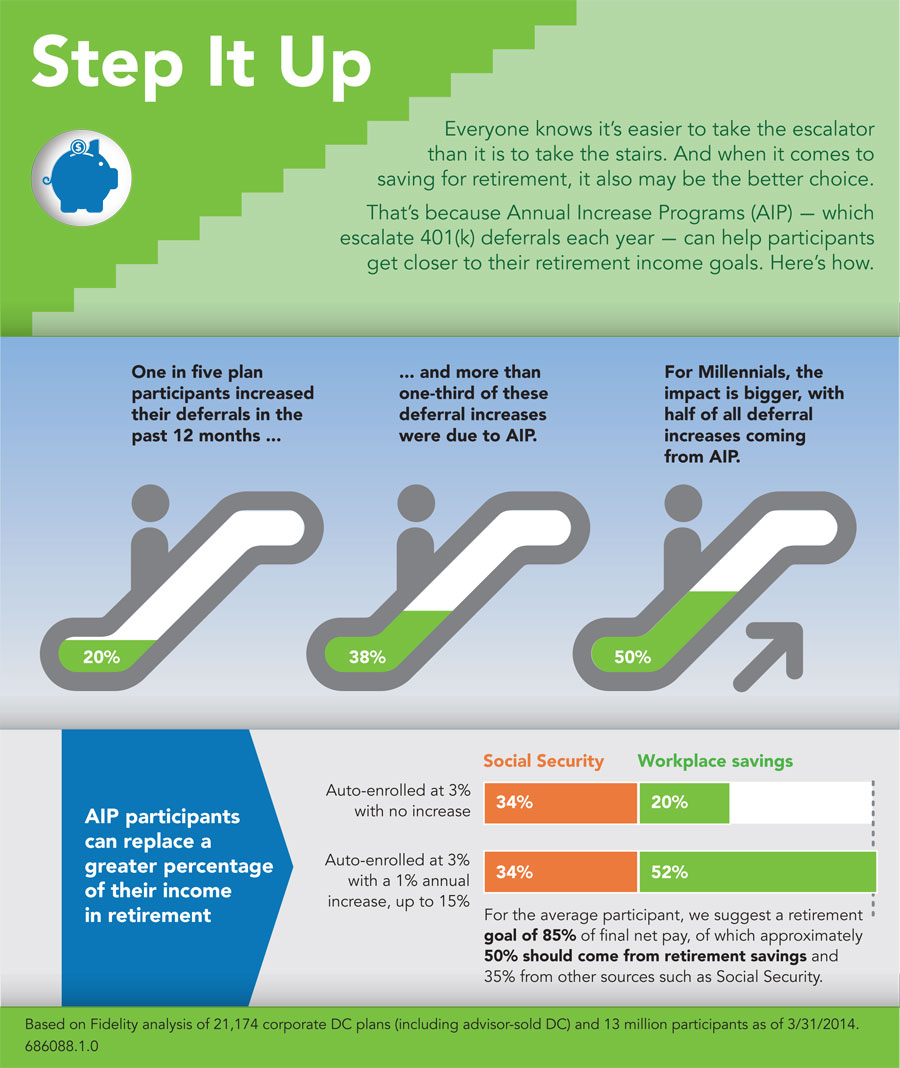

Annual Increase Programs (AIP), an optional feature in 401(k) plans that automatically increases an employee’s savings over time, may help bridge the gap. AIPs typically increase deferrals by 1 percent per year to automatically raise an employee’s total savings to the desired 10-15 percent rate6. Over the prior 12 months, 1 in 5 (20 percent) of employees increased their personal savings rate – the highest percentage since Fidelity started tracking the number seven years ago. Nearly 2 in 5 (38 percent) deferral increases were due to an AIP, and of Fidelity’s Gen Y employees7, half of all (50 percent) deferral increases were due to the feature.

AIP is offered by three quarters (77 percent) of Fidelity 401(k) plan sponsors with 12 percent of them automatically enrolling employees in the program. With only 7 percent of employees opting out when automatically enrolled in an AIP, employers could help drive savings rates higher by incorporating automatic AIP into their auto enrollment process.

“We understand that saving for retirement competes with numerous financial goals such as the purchase of a home, college tuition and the escalating costs of health care in retirement,” said McCarthy. “Fidelity recommends companies offer automatic features to promote participation and annual savings increases by employees. And we urge investors to take advantage of additional savings opportunities such as IRAs and health savings accounts, if available, to help build their individualized retirement paycheck.”

Fidelity Retirement Guidance Driving Positive Savings Actions by Employees

The company’s workplace guidance experience, Plan for Life, has made significant progress in helping employees make informed decisions. In 2013 Fidelity noted a 42 percent increase in guidance sessions, and of those employees who took advantage of them, 37 percent took a positive action such as increasing their savings rate8 or reviewing their asset allocation. In addition, Fidelity’s online participant hub, NetBenefits®, is now available on a smartphone and iPad® tablet app. Since the app’s launch it has received more than 825,000 unique logins.

Media-Ready Infographic Available

Fidelity’s downloadable infographic, Help Your Employees: Step It Up, depicts the role AIPs can play in boosting savings rates (see image).

About Fidelity Investments

Fidelity Investments is one of the world’s largest providers of financial services, with assets under administration of $4.7 trillion, including managed assets of $2.0 trillion, as of March 31, 2014. Founded in 1946, the firm is a leading provider of investment management, retirement planning, portfolio guidance, brokerage, benefits outsourcing and many other financial products and services to more than 20 million individuals and institutions, as well as through 5,000 financial intermediary firms. For more information about Fidelity Investments, visit www.fidelity.com.

Keep in mind that investing involves risk. The value of your investment will fluctuate over time and you may gain or lose money.

Diversification does not ensure a profit or protect against a loss.

Past performance is no guarantee of future results.

Fidelity Brokerage Services LLC, Member NYSE, SIPC

900 Salem Street, Smithfield, RI 02917

Fidelity Investments Institutional Services Company, Inc.

500 Salem St., Smithfield, RI 02917

685481.1.0

© 2014 FMR LLC. All rights reserved.

1 Pensions & Investments, March 3, 2014, “The largest DC record keepers” and Cerulli Associates’ The Cerulli Edge®—Retirement Edition, fourth quarter, 2013 based on an industry survey of firms reporting total IRA assets administered for Q3 2013.

2 All 401(k) data as of March 31, 2014 unless otherwise stated, and is based on our recordkept corporate defined contribution plan base of 21,200 plans and 13 million participants (who are actively employed employees and retired or terminated employees who still carry a balance), excluding tax-exempt employees.

3 Includes traditional IRA, rollover IRA and Roth IRA.

4 Fidelity data as of March 31, 2014

5 Total savings rate includes both employer and employee contributions.

6 Ibid.

7 Employees born between 1979 - 1991.

8 Deferral rate.