Newsroom

Sorted by: Latest

-

First Trust Global Funds PLC UK Regulatory Announcement: Net Asset Value(s)

LONDON--(BUSINESS WIRE)-- Funds Date TIDM ISIN Code Shares in Issue Currency Net Asset Value NAV/per Share First Trust Capital Strength UCITS ETF 10.07.2026 FTCS. IE00BL0L0D23 350,002.00 USD 11,793,806.92 33.696 ...

-

Solink Awarded AI Agent Product of the Year Award from TMCnet

OTTAWA, Ontario--(BUSINESS WIRE)--Solink, the leader in AI vision intelligence, announced today that TMC, a global, integrated media company, has named Solink AI Agents as a 2026 AI Agent Product of the Year Award winner. These awards honor innovative solutions that harness the power of artificial intelligence to elevate performance across all verticals and business functions. In leveraging its AI solutions to drive real outcomes for customers, Solink is redefining how multi-location businesses...

-

CACI’s SkyValor Selected to Strengthen Drone Defense at the Southern Border

RESTON, Va.--(BUSINESS WIRE)--CACI International Inc (NYSE: CACI) announced today that it was awarded a contract by the Department of War (DoW) to deploy SkyValor, CACI’s advanced drone defense system, at the Southern Border. The deployment will support a broader national security effort to counter the growing threat of hostile drones and strengthen homeland defense in high-priority operating environments. “Drone threats are evolving quickly, and they are challenging the way we protect our forc...

-

Medalist Diversified, Inc. Announces Dividend of $0.0675 Per Share on Its Common Stock

RICHMOND, Va.--(BUSINESS WIRE)--Medalist Diversified, Inc. (NASDAQ: MDRR) (the "Company" or "Medalist"), a Virginia-based sponsor of Delaware Statutory Trusts, announced that its Board of Directors has authorized and the Company has declared a quarterly dividend on its common stock (the "Common Stock") in the amount of $0.0675 per share (the "Dividend"). The Dividend will be payable in cash on July 30, 2026 to holders of record of the Common Stock as of July 23, 2026....

-

Tenpoint Therapeutics Announces United Kingdom Submission of Marketing Authorization Application to the Medicines and Healthcare Products Regulatory Agency (MHRA) for the Treatment of Blurry Close-Up Vision (Presbyopia) in Adults

LONDON & WARREN, N.J.--(BUSINESS WIRE)--Tenpoint Therapeutics announced the submission of an MAA to the United Kingdom’s MHRA for the review of YUVEZZI™ for the treatment of presbyopia....

-

Guthrie AI Raises $4 Million Seed Round Led by Chicago Ventures to Put a Virtual Bid Assistant on Every Glazing Team

PHILADELPHIA--(BUSINESS WIRE)--Guthrie AI Raises $4 Million Seed Round Led by Chicago Ventures to Put a Virtual Bid Assistant on Every Glazing Team...

-

First Trust Global Funds PLC UK Regulatory Announcement: Net Asset Value(s)

LONDON--(BUSINESS WIRE)-- Funds Date TIDM ISIN Code Shares in Issue Currency Net Asset Value NAV/per Share First Trust Value Line Dividend Index UCITS ETF 10.07.2026 FVD. IE00BKVKW020 300,002.00 USD 9,020,253.63 30.067 ...

-

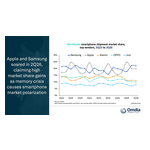

Omdia: Global Smartphone Market Down 4% in 2Q26 While Apple and Samsung Soared

LONDON--(BUSINESS WIRE)--According to Omdia’s latest research, global smartphone shipments fell 4% year-on-year in 2Q26 as the ongoing memory crisis disrupted supply and pushed up component costs. The current dynamic has created severe market polarization, reflecting stark differences in vendors’ mitigation strategies which vary according to their priorities, scale, price-band focus, and core audience demographics. In particular, Samsung and Apple bucked the downward trend, growing shipments an...

-

Healthcare Monitor 2025-2026: Pharmaceutical companies must better respond to website quality, target-group-oriented communication, and AI visibility

NEW YORK--(BUSINESS WIRE)--Worldcom Public Relations Group presents new edition of healthcare monitor, providing an in-depth analysis of trust, visibility, and findability....

-

Applebee’s® Aims to Raise Over $1.5 Million for Childhood Cancer Research with Annual Alex’s Lemonade Stand Foundation Fundraiser

PASADENA, Calif.--(BUSINESS WIRE)--Today, Applebee’s® kicked off its “Squeeze Out Childhood Cancer” fundraiser for Alex’s Lemonade Stand Foundation (ALSF), the largest independent charity in the U.S. dedicated to childhood cancer research and family support. In celebration of its 22-year partnership, Applebee’s aims to raise more than $1.5 million this year to help fund lifesaving research and provide critical support to families.Now through August 30, Applebee’s will donate 50¢ from every NEW L...