Newsroom

Sorted by: Latest

-

Comera Financial Holdings, Part of Abu Dhabi’s Royal Group, and SC Ventures Announce Strategic Collaboration to Explore Innovation in SME and Beyond

ABU DHABI, United Arab Emirates--(BUSINESS WIRE)--Comera Financial Holdings, Part of Abu Dhabi’s Royal Group, and SC Ventures Announce Strategic Collaboration to Explore Innovation in SME and Beyond...

-

Completion of the Fast Plasma Positioning Control Coil for stable confinement of the world’s largest plasma

TOKYO--(BUSINESS WIRE)--The National Institutes for Quantum Science and Technology (President: KOYASU Shigeo; hereinafter referred to as "QST") and Mitsubishi Electric Corporation (President & CEO: URUMA Kei; hereinafter referred to as "Mitsubishi Electric") have successfully completed the fabrication of two Fast Plasma Positioning Control Coils (FPPCs)—a core technology for high-speed, high-precision plasma position control—for JT-60SA as part of the Broader Approach Activities, which is a...

-

Over $1.5 Billion Baltimore Verdict Holds Johnson & Johnson Liable Over Iconic Baby Powder

BALTIMORE--(BUSINESS WIRE)--A Baltimore city jury has returned a verdict in favor of Cherie A. Craft, awarding her over $1.5 billion after finding that Johnson & Johnson and its subsidiaries exposed her to asbestos through talc-based personal care products and caused her to develop peritoneal malignant mesothelioma, an incurable cancer. The verdict is believed to be the largest ever returned against Johnson & Johnson for a single plaintiff. Ms. Craft, a mother and the founder, CEO and e...

-

Celltrion旗下SteQeyma™ (ustekinumab biosimilar) autoinjector 獲歐盟 CHMP 正面評價

韓國·仁川--(BUSINESS WIRE)--(美國商業資訊)-- 賽特瑞恩(Celltrion)公司今日宣布,歐洲藥品管理局(EMA)的人用藥品委員會(CHMP)已對其生物相似藥 SteQeyma™(對照原研藥 Stelara®,學名:ustekinumab)的自動注射筆給予正面評價,該產品適用於治療斑塊狀乾癬、乾癬性關節炎 (PsA)及克隆氏症 (CD)。 CHMP 的正面意見涵蓋了 45 毫克/0.5 毫升與 90 毫克/1 毫升劑型的 SteQeyma 自動注射筆,這將擴展現有已核准的 SteQeyma™ 產品組合——該組合原先包括 45 毫克/0.5 毫升與 90 毫克/1 毫升的預充式注射器,以及 130 毫克/26 毫升的靜脈輸注濃縮液 「新型 SteQeyma™ 自動注射筆結合了便利性與實用操作性,以應對慢性發炎性疾病患者日常面臨的挑戰。」賽特瑞恩歐洲事業部資深副總裁暨負責人河泰勳(Taehun Ha)表示:「隨著自動注射筆的加入,我們完整的 SteQeyma™ 劑型與強度組合,將為患者與醫療專業人員提供更個人化的治療選擇,這些選擇不僅易於使用,更有助於提升用藥依從性...

-

EQUITY ALERT: Rosen Law Firm Files Securities Class Action Lawsuit Against Klarna Group plc – KLAR

NEW YORK--(BUSINESS WIRE)--Rosen Law Firm, a global investor rights law firm, announces it has filed a class action lawsuit on behalf of purchasers of securities of Klarna Group plc (NYSE: KLAR) pursuant and/or traceable to the registration statement and related prospectus (collectively, the “Registration Statement”) issued in connection with Klarna’s September 2025 initial public offering (the “IPO”). The lawsuit seeks to recover damages for Klarna investors under the federal securities laws....

-

StratCap Digital Infrastructure REIT Sells Cell Towers to Accelerate Rebalancing Toward Core Data Centers

NEW YORK--(BUSINESS WIRE)--StratCap Digital Infrastructure REIT Sells Cell Towers to Accelerate Rebalancing Toward Core Data Centers...

-

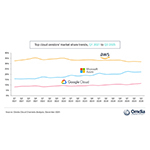

オムディア、世界のクラウド・インフラ支出、2025年第3四半期に25%増の1026億ドルに達する

ロンドン--(BUSINESS WIRE)--(ビジネスワイヤ) -- オムディアの最新調査によると、クラウド・インフラサービスへの世界の支出は2025年第3四半期に1026億ドルに達し、前年同期比25%増となりました。市場の勢いは安定していて、5四半期連続で20%以上の成長率を維持しており、業界全体の堅調さが持続していることが浮き彫りになっています。この結果には、AIに対する企業の需要が初期の実験段階から大規模な本番環境への展開へと移行する中で、テクノロジー環境が大きく変化していることが反映されています。この移行が加速するにつれて、ハイパースケーラーは競争の焦点を、モデルパフォーマンスの漸進的な向上から、マルチモデルの展開をサポートして実環境におけるAIエージェントの信頼性の高い運用を可能にするプラットフォームレベルの機能へと転換させています。 2025年第3四半期、AWS、Microsoft Azure、Google Cloudは前四半期から市場ランキングを維持し、合計で世界のクラウド・インフラ支出の66%を占めました。3社のハイパースケーラーは、合計で前年比29%の成長を達成し...

-

Kashiv BioSciences Secures INR 648 Crore Financing from Union Bank of India to Expand Manufacturing Facilities in Gujarat, India

AHMEDABAD, India--(BUSINESS WIRE)--Kashiv BioSciences Private Limited (“Kashiv”), a biopharmaceutical company, today announced that it has secured financing of INR 648 crore from the Union Bank of India. The proceeds will be used to expand its state-of-the-art manufacturing facility in Pipan, near Ahmedabad, Gujarat. The new single-use commercial manufacturing facility will be one of India’s largest, equipped with cutting-edge technologies to support the production of high-quality biologics and...

-

Se entrega el primer Cessna SkyCourier en México, ampliando las capacidades de carga aérea de FlexCoah

WICHITA, Kansas--(BUSINESS WIRE)--El primer Cessna SkyCourier en México fue entregado recientemente a FlexCoah —proveedora de servicios de transporte de carga— para ser operado por Altair, la filial aérea de la empresa. La aeronave, en su versión carguera, permitirá ampliar las capacidades de carga aérea de la empresa en todo el país. El Cessna SkyCourier ha sido diseñado y fabricado por Textron Aviation Inc., una empresa de Textron Inc. (NYSE: TXT). "La combinación de confiabilidad, capacidad...

-

SLM ALERT: Kirby McInerney LLP Announces the Filing of a Securities Class Action on Behalf of SLM Corporation a/k/a Sallie Mae Investors

NEW YORK--(BUSINESS WIRE)--The law firm of Kirby McInerney LLP announces that a class action lawsuit has been filed on behalf of investors who acquired SLM Corporation a/k/a Sallie Mae (“SLM” or the “Company”) (NASDAQ:SLM) securities during the period of July 25, 2025 through August 14, 2025, inclusive (“the Class Period”). If you suffered a loss on your SLM investments, you have until February 17, 2026 to request lead plaintiff appointment. For more information: [CONTACT THE FIRM IF YOU SUFFER...