Newsroom

Sorted by: Latest

-

Actor and Cancer Advocate Patrick Dempsey Stars in Emotional Tribute Video From Guardant Health Memorializing Those Who Have Lost Their Lives to Colorectal Cancer

PALO ALTO, Calif.--(BUSINESS WIRE)--Guardant Health, Inc. (Nasdaq: GH), a leading precision oncology company, today announced the launch of a new video featuring actor and cancer advocate Patrick Dempsey that highlights the more than 55,000 Americans who will lose their lives to colorectal cancer (CRC) this year1, a majority of which will not have been up to date with their colorectal cancer screening.2 The video pays an emotional tribute to Americans from across the country who have passed fro...

-

Binary Defense Names Industry Veteran Rafal Los as Chief Strategy Officer

CLEVELAND--(BUSINESS WIRE)--Binary Defense names cybersecurity veteran Rafal Los Chief Strategy Officer to advance AI-driven MDR, SOC innovation and market strategy....

-

Dealer Pay Joins The Shop by FordDirect as a Preferred Vendor

SAINT CHARLES, Mo.--(BUSINESS WIRE)--Dealer Pay, driven by Vehlo, today announced it has been named a preferred vendor in The Shop by FordDirect, which is a curated marketplace of trusted dealership solutions. Dealer Pay is the first payments solution approved as an endorsed vendor within The Shop. The inclusion of Dealer Pay in FordDirect marks the 27th OEM that Vehlo’s solutions now have a partnership with, highlighting the trust the automotive industry has in the company. Dealer Pay’s status...

-

AST SpaceMobile Announces Launch Date for BlueBird Satellites 11, 12, and 13

MIDLAND, Texas--(BUSINESS WIRE)--AST SpaceMobile, Inc. (“AST SpaceMobile”) (NASDAQ: ASTS), the company building the first and only space-based cellular broadband network accessible directly by everyday smartphones, designed for both commercial and government applications, today announced that the launch of BlueBird 11, 12, and 13 satellites is currently scheduled for Wednesday, August 5, 2026, from Cape Canaveral Space Force Station, Florida, aboard a Falcon 9 rocket. Liftoff is targeted for 3:...

-

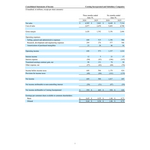

Core Scientific Announces Second Quarter 2026 Results

MIAMI--(BUSINESS WIRE)--Core Scientific, Inc. (NASDAQ: CORZ), a leader in digital infrastructure for high-density colocation services (“HDC”), today announced financial results for the second quarter ended June 30, 2026. Recent Business Developments Announced a partnership with AMD with the potential to support up to 2.5 GW of leasable capacity, anchored by 15-year agreements for approximately 530 MW across five sites and more than $14 billion of potential base contracted revenue. Increased tot...

-

Massachusetts Financial Services Company UK Regulatory Announcement: Form 8.3

LONDON--(BUSINESS WIRE)-- FORM 8.3 PUBLIC OPENING POSITION DISCLOSURE/DEALING DISCLOSURE BY A PERSON WITH INTERESTS IN RELEVANT SECURITIES REPRESENTING 1% OR MORE Rule 8.3 of the Takeover Code (the “Code”) 1. KEY INFORMATION (a) Full name of discloser: Massachusetts Financial Services Company (b) Owner or controller of interests and short positions disclosed, if different from 1(a): The naming of nominee or vehicle companies is insufficient. For a trust, the trustee(s), settlor and beneficiari...

-

Everforth ECS Wins $115M AI Research and Engineering Contract Supporting US Army Nautilus Program

FAIRFAX, Va.--(BUSINESS WIRE)--Everforth ECS Wins $115M AI Research and Engineering Contract Supporting US Army Nautilus Program...

-

Corning’s Strong Second-Quarter 2026 Financial Results(1) Demonstrate Progress on Recently Upgraded Springboard Plan

CORNING, N.Y.--(BUSINESS WIRE)--Corning Incorporated (NYSE: GLW) today announced its second-quarter 2026 results and provided its outlook for third-quarter 2026. News Summary: Year over year, Q2 core sales grew 17% to $4.74 billion. Core EPS grew 30% to $0.78. Optical Communications grew sales 32% to $2.07 billion, including a 65% increase in Enterprise Networks, with Gen AI product sales growing significantly faster. Solar grew sales 90% and completed an extended maintenance shutdown and equip...

-

Asbury Automotive Group Reports Second Quarter Results

ATLANTA--(BUSINESS WIRE)--Asbury Automotive Group, Inc. (NYSE: ABG) (the “Company”), one of the largest automotive retail and service companies in the U.S., reported second quarter 2026 net income of $115 million ($6.25 per diluted share), a decrease of 25% from $153 million ($7.76 per diluted share) in second quarter 2025. The Company reported second quarter 2026 adjusted net income, a non-GAAP measure, of $125 million ($6.82 per diluted share), a decrease of 15% from $146 million ($7.43 per d...

-

908 Devices to Report Second Quarter 2026 Financial Results on August 11, 2026

BURLINGTON, Mass.--(BUSINESS WIRE)--908 Devices Inc. (Nasdaq: MASS), a core small-cap growth company focused on purpose-built handheld chemical analysis tools for vital health, safety and defense tech applications, announced it will report financial results for the second quarter 2026 before market open on Tuesday, August 11, 2026. Company management will webcast a corresponding conference call beginning at 8:30 a.m. Eastern Time. Live audio of the webcast will be available on the “Investors” s...