Newsroom

Sorted by: Latest

-

Fastenal Company Reports 2026 Second Quarter Earnings

WINONA, Minn.--(BUSINESS WIRE)--Fastenal Company (Nasdaq:FAST) ('Fastenal,' 'we,' 'our,' or 'us'), a global leader in supply chain services, today reported results for the second quarter ended June 30, 2026. Results reflected strong daily sales growth, operating expense leverage, and continued growth with larger customers supported by our onsite, digital, and supply chain solutions. Except for share and per share information, or as otherwise noted, amounts are stated in millions. Percentage and...

-

Wells Fargo Reports Second Quarter 2026 Financial Results

SAN FRANCISCO--(BUSINESS WIRE)--Wells Fargo & Company (NYSE: WFC) has released its second quarter 2026 financial results. The financial results are available online at https://www.wellsfargo.com/about/investor-relations/quarterly-earnings/ and on a Form 8-K filed by the company with the Securities and Exchange Commission (SEC) on July 14, 2026, and available on the SEC’s website at https://www.sec.gov/.Conference callThe company will host a live conference call on Tuesday, July 14, at 10:00...

-

Ferguson Enterprises Inc. UK Regulatory Announcement: Ferguson Enterprises Inc. (“Company”): Director/PDMR Shareholding

NEWPORT NEWS, Va.--(BUSINESS WIRE)-- NOTIFICATION OF TRANSACTIONS BY PERSONS DISCHARGING MANAGERIAL RESPONSIBILITIES (“PDMRs”) IN COMMON STOCK OF PAR VALUE $0.0001 EACH IN THE COMPANY (“Shares”) 1 Details of the person discharging managerial responsibilities / person closely associated a) Name Kelly Baker 2 Reason for the notification a) Position/status Director b) Initial/Amendment notification Initial notification 3 Details of the issuer, emission allowance market participant, auction platfo...

-

Jacobs to hold its fiscal third quarter 2026 earnings conference call and webcast

DALLAS--(BUSINESS WIRE)--Jacobs to hold its fiscal third quarter 2026 earnings conference call and webcast after market close on Tuesday, Aug. 4, 2026....

-

RPX Gold Accelerates Drilling at the Wawa Gold Project

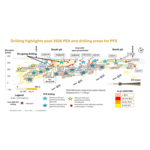

TORONTO--(BUSINESS WIRE)--RPX Gold Inc. (“RPX Gold”, “RPX” or the “Company”) (TSXV: RPX. OTCQB: RDEXF) is pleased to announce the mobilization of a second diamond drill at its Wawa Gold Project in Ontario (Figure 1). The second drill will expedite the completion of the ongoing 20,000 metre (“m”) drilling program, of which approximately 5,000 metres have been completed to date, in preparation of a prefeasibility study (“PFS”) targeted for completion in the first half of 2027 (“H1 2027”). The 20,...

-

Ferguson Enterprises Inc. (“Company”): Director/PDMR Shareholding

NEWPORT NEWS, Va.--(BUSINESS WIRE)--NOTIFICATION OF TRANSACTIONS BY PERSONS DISCHARGING MANAGERIAL RESPONSIBILITIES (“PDMRs”) IN COMMON STOCK OF PAR VALUE $0.0001 EACH IN THE COMPANY (“Shares”) 1 Details of the person discharging managerial responsibilities / person closely associated a) Name Kelly Baker 2 Reason for the notification a) Position/status Director b) Initial/Amendment notification Initial notification 3 Details of the issuer, emission allowance market participant, auction platform...

-

ISTH 2026: Incyte präsentiert Daten zur Mehrfachdosierung von VGA039 (Latarcibart) aus einer Phase-1/2-Studie, die eine deutliche Verringerung der Blutungen bei Patienten mit allen Formen des von-Willebrand-Syndroms zeigen

WILMINGTON, Del.--(BUSINESS WIRE)--Incyte (Nasdaq: INCY) gab heute die vollständigen Sicherheits- und Wirksamkeitsdaten aller Patienten (n = 16) bekannt, die an der Phase-1/2-Studie zur Mehrfachdosierung von VGA039 (Latarcibart) teilnahmen. Latarcibart ist ein neuartiger, gegen Protein S gerichteter monoklonaler Antikörper in klinischer Prüfung für Patienten mit von-Willebrand-Syndrom (VWS). Die Daten werden heute im Rahmen eines Vortrags auf dem 34. Kongress der International Society on Thromb...

-

Riassunto: Incyte presenta all'ISTH 2026 i dati di fase 1/2 su dosi multiple di VGA039 (latarcibart) ed evidenzia una sostanziale riduzione del sanguinamento nei pazienti affetti da ogni tipo di malattia di von Willebrand

WILMINGTON, Del.--(BUSINESS WIRE)--Incyte (Nasdaq: INCY) oggi ha annunciato i dati completi di sicurezza ed efficacia di tutti i pazienti (n=16) arruolati nello studio multidose di fase 1/2 su VGA039 (latarcibart), un innovativo anticorpo monoclonale sperimentale mirato alla proteina S nei pazienti affetti da malattia di von Willebrand (VWD). Il testo originale del presente annuncio, redatto nella lingua di partenza, è la versione ufficiale che fa fede. Le traduzioni sono offerte unicamente per...

-

JPMorganChase Reports Second-Quarter 2026 Financial Results

NEW YORK--(BUSINESS WIRE)--JPMorgan Chase & Co. has released its second-quarter 2026 financial results. Results can be found at the Firm’s Investor Relations website at jpmorganchase.com/ir/quarterly-earnings. JPMorgan Chase & Co. (NYSE: JPM) is a leading financial services firm based in the United States of America (“U.S.”), with operations worldwide. JPMorganChase had $5.0 trillion in assets and $375 billion in stockholders’ equity as of June 30, 2026. The Firm is a leader in investme...

-

Samenvatting: Incyte presenteert Fase 1/2 multidosisgegevens voor VGA039 (latarcibart) tijdens ISTH 2026, die aanzienlijke vermindering van bloedingen aantonen bij patiënten met alle types van de ziekte van Von Willebrand

WILMINGTON, Del.--(BUSINESS WIRE)--Incyte (Nasdaq: INCY) maakte vandaag de gegevens bekend over de volledige veiligheid en doeltreffendheid bij alle patiënten (n=16) die deelnamen aan de Fase 1/2 multidosis-studie van VGA039 (latarcibart), een nieuw, op proteïne S gericht, monoklonaal antilichaam in onderzoeksfase voor patiënten met de ziekte van von Willebrand (VWD). Deze bekendmaking is officieel geldend in de originele brontaal. Vertalingen zijn slechts als leeshulp bedoeld en moeten worden...