Newsroom

Sorted by: Latest

-

First Trust Global Funds PLC UK Regulatory Announcement: Net Asset Value(s)

LONDON--(BUSINESS WIRE)-- Funds Date TIDM ISIN Code Shares in Issue Currency Net Asset Value NAV/per Share First Trust SMID Rising Dividend Achievers UCITS ETF 09.06.2026 SDVI.LN IE000YVOQ2A3 40,361.00 USD 1,144,826.52 28.365 ...

-

First Trust Global Funds PLC UK Regulatory Announcement: Net Asset Value(s)

LONDON--(BUSINESS WIRE)-- Funds Date TIDM ISIN Code Shares in Issue Currency Net Asset Value NAV/per Share First Trust SMID Rising Dividend Achievers UCITS ETF 09.06.2026 SDVY.LN IE0001R850E1 14,604,007.00 USD 364,891,574.74 24.986 ...

-

First Trust Global Funds PLC UK Regulatory Announcement: Net Asset Value(s)

LONDON--(BUSINESS WIRE)-- Funds Date TIDM ISIN Code Shares in Issue Currency Net Asset Value NAV/per Share First Trust Growth Strength UCITS ETF 09.06.2026 FTGS.LN IE000YZLMXT9 25,002.00 USD 577,217.77 23.087 ...

-

First Trust Global Funds PLC UK Regulatory Announcement: Net Asset Value(s)

LONDON--(BUSINESS WIRE)-- Funds Date TIDM ISIN Code Shares in Issue Currency Net Asset Value NAV/per Share First Trust Vest U.S. Equity Moderate Buffer UCITS ETF - February 09.06.2026 GFEB.LN IE000X8M8M80 700,002.00 USD 27,241,372.34 38.916 ...

-

PhoreMost Announces Lead Oncology Programme and Appoints Chief Medical Officer to Support Clinical Entry

CAMBRIDGE, England--(BUSINESS WIRE)--PhoreMost Limited (“PhoreMost”), a biotech company focused on turning scientific breakthroughs into life-changing cancer drugs, today announced its lead programme, PMC-001, a next-generation, small molecule microtubule targeting agent (MTA) for primary and secondary brain cancers. The milestone marks the Company’s progress towards first-in-human clinical trials, with a pipeline of differentiated and first-in-class assets in oncology. PMC-001 is a highly diff...

-

Cosylab and Heron Neutron Medical Corp. Sign Letter of Intent to Advance Global Deployment of Accelerator-Based BNCT Systems

LJUBLJANA, Slovenia--(BUSINESS WIRE)--Cosylab and Heron Neutron Medical Corp. announced today, 10 June 2026, the signing of a Letter of Intent to establish a strategic framework for joint market development to support the global deployment of Accelerator-Based Boron Neutron Capture Therapy (AB-BNCT) systems. The collaboration aims to accelerate the development and integration of sophisticated software solutions for use with AB-BNCT while strengthening AB-BNCT's international market access and b...

-

Laverock Therapeutics Reports Key Oncology Research Milestones

LONDON--(BUSINESS WIRE)--Laverock Therapeutics (‘Laverock’), a biotechnology company developing disease-responsive advanced therapies through its unique, programmable gene control technology, today announced key in-vivo functional milestones across its T-cell and macrophage oncology programmes for solid tumour indications. The data support lead programme selection and progression towards the clinic. Laverock’s platform technology enables programmable, tunable and multiplex gene control for both...

-

GlobalFoundries en Qualinx demonstreren Europa's eerste soevereine productieketen voor beveiligingskritische halfgeleiders

DRESDEN, Duitsland & DELFT, Nederland--(BUSINESS WIRE)--GlobalFoundries and Qualinx Demonstrate First European Sovereign Manufacturing Flow for Security‑Critical Semiconductors...

-

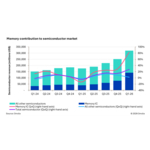

Omdia: Semiconductor Market Surpasses $300bn Quarterly Revenue in 1Q26 as Memory Market Shifts Historical Patterns

LONDON--(BUSINESS WIRE)--Following a record-setting year for the semiconductor industry, the start of the new year has continued the momentum, as semiconductor revenue grew 27% in 1Q26 from 4Q25 to reach $319bn, according to new research form Omdia. Memory revenue drove the increase, rising over 80% sequentially in 1Q26 from 4Q25. Since Omdia began tracking the semiconductor market at a quarterly level in1Q02, this 27% quarter-over-quarter (QoQ) growth is the highest observed. The market has no...

-

NextSilicon to Productize Arbel RISC-V Core Into 64-Core Enterprise Processor for AI and HPC

BOLOGNA, Italy--(BUSINESS WIRE)--NextSilicon, a leader in next-generation computing solutions for AI and high-performance computing (HPC), today announced plans to productize its Arbel RISC-V core into a 64-core and a 128-core, enterprise-grade processor suited to deliver ultra-speed performance for agentic tools, expected to be available in early 2028. Following an October preview, the company is now sharing expanded technical detail and a roadmap shaped by early customer and partner feedback....