Newsroom

Sorted by: Latest

-

TWO Determines Unsolicited Proposal from CrossCountry Mortgage is a “Company Superior Proposal”

NEW YORK--(BUSINESS WIRE)--TWO Determines Unsolicited Proposal from CrossCountry Mortgage is a “Company Superior Proposal”...

-

Ford and Major League Baseball Unite to Celebrate America’s Pastime and the People Who Power It

DETROIT & NEW YORK--(BUSINESS WIRE)--Ford Motor Company and Major League Baseball today announced a multiyear exclusive partnership that brings together two American icons. As MLB’s Official Automotive Partner, Ford will show up for baseball at every level—from neighborhood Little League fields to the World Series—honoring tradition, celebrating human capability, and powering the moments that matter most. The partnership unites America’s favorite pastime with America’s Most Iconic Company and A...

-

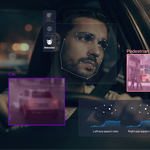

Mobileye Secures Major DMS Production Program with Leading U.S. Automaker

JERUSALEM--(BUSINESS WIRE)--Mobileye (Nasdaq: MBLY) today announced that a leading U.S. automaker will integrate the Mobileye Driver Monitoring System™ (Mobileye DMS) into future vehicles equipped with Mobileye's EyeQ6L system-on-chip, with start of production targeted for 2027. The newly awarded win expands the scope and feature set of an existing ADAS program and is expected to span millions of vehicles across multiple models and model years. Mobileye’s in-cabin sensing platform includes both...

-

Acture Solutions Receives Strategic Financing from Stonepeak Credit

ALBANY, N.Y. & NEW YORK--(BUSINESS WIRE)--Acture Solutions (“Acture” or the “Company”), a leading managed service provider serving K–12 educational and regional organizations across the Northeast, today announced that it has received strategic growth financing from Stonepeak Credit. This financing will support the Company’s continued expansion, including through its acquisition of Artilus, Inc. (“Artilus”), a Long Island–based provider of cybersecurity, managed information technology, and syste...

-

State Street Elects Susan Gordon to Its Board of Directors

BOSTON--(BUSINESS WIRE)--State Street Corporation (NYSE:STT) today announced the election of Susan Gordon to its Board of Directors. Ms. Gordon is an accomplished leader in national security, intelligence, and technology, with a career spanning over three decades at the highest levels of the U.S. government. As the former Principal Deputy Director of National Intelligence, she provided operational leadership across the agencies and organizations of the U.S. intelligence community. Throughout he...

-

Lufax Holding Ltd Sued for Securities Law Violations - Contact the DJS Law Group to Discuss Your Rights – LU

LOS ANGELES--(BUSINESS WIRE)--Lufax Holding Ltd Sued for Securities Law Violations - Contact the DJS Law Group to Discuss Your Rights – LU...

-

First Trust Global Funds PLC UK Regulatory Announcement: Net Asset Value(s)

LONDON--(BUSINESS WIRE)-- Funds Date TIDM ISIN Code Shares in Issue Currency Net Asset Value NAV/per Share First Trust Vest U.S. Equity Moderate Buffer UCITS ETF- August 20.03.2026 GAUG LN IE000TGSG3Y5 550,002.00 USD 19,037,708.77 34.614 ...

-

First Trust Global Funds PLC UK Regulatory Announcement: Net Asset Value(s)

LONDON--(BUSINESS WIRE)-- Funds Date TIDM ISIN Code Shares in Issue Currency Net Asset Value NAV/per Share First Trust Bloomberg Scarce Resources UCTS ETF 20.03.2026 SCAR LN IE000BW2B3J3 25,002.00 USD 718,777.53 28.749 ...

-

First Trust Global Funds PLC UK Regulatory Announcement: Net Asset Value(s)

LONDON--(BUSINESS WIRE)-- Funds Date TIDM ISIN Code Shares in Issue Currency Net Asset Value NAV/per Share FIRST TRUST INDXX FUTURE ECONOMY METALS UCITS ETF 20.03.2026 METL LN IE000UDFKE13 150,002.00 USD 4,844,327.77 32.295 ...

-

First Trust Global Funds PLC UK Regulatory Announcement: Net Asset Value(s)

LONDON--(BUSINESS WIRE)-- Funds Date TIDM ISIN Code Shares in Issue Currency Net Asset Value NAV/per Share First Trust Low Duration Global Government Bond UCITS ETF 20.03.2026 FGOV LN IE00BKS2X200 58,638.00 GBP 866,173.56 17.021 ...