Newsroom

Sorted by: Latest

-

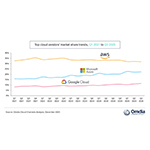

Omdia: Global Cloud Infrastructure Spending Hits $102.6 Billion, up 25% in Q3 2025

LONDON--(BUSINESS WIRE)--According to new research from Omdia, global spending on cloud infrastructure services reached $102.6 billion in Q3 2025, representing 25% year-on-year growth. Market momentum remained stable, marking the fifth consecutive quarter in which growth has remained above 20% highlighting continued strength across the sector. This performance reflects a significant shift in the technology landscape as enterprise demand for AI moves beyond early experimentation toward scaled pr...

-

Axelspace Signing Agreement on a Multi-Launch Arrangement and the Launch of New Satellites with Exolaunch

TOKYO--(BUSINESS WIRE)--Axelspace Corporation (“Axelspace”), a leading microsatellite company committed to making “Space within Your Reach,” is pleased to announce a multi-launch agreement (MLA) with Exolaunch, a global launch integrator and leader in launch mission management, satellite integration and satellite deployment technologies. The Multi-Launch Agreement will accelerate the growth of Axelspace. In particular, one satellite scheduled for launch under the new Agreement will be used in t...

-

Axelspace: Notice of Signing a Service contract for In-Orbit Demonstration with Pale Blue, Inc.

TOKYO--(BUSINESS WIRE)--Axelspace Corporation (“Axelspace”), a leading microsatellite company committed to making “Space within Your Reach,” has entered into a service agreement with Pale Blue Inc. (“Pale Blue”), a company that develops, manufactures, and sells thrusters (engines) for small satellites, for an in-orbit demonstration, as detailed below. Axelspace provides AxelLiner Laboratory (AL Lab), a new service originating from the AxelLiner business that is specialized in in-orbit demonstra...

-

アクセルスペース、Pale Blue社との軌道上実証サービス提供に関する契約締結のお知らせ

東京--(BUSINESS WIRE)--(ビジネスワイヤ) -- 小型衛星を開発・運用し、誰もが宇宙を利用できる社会を目指して事業を展開する株式会社アクセルスペース(本社:東京都中央区、代表取締役:中村友哉、以下「当社」)はこのたび、小型衛星向けのスラスタ (エンジン) を開発・製造・販売する株式会社Pale Blue(本社:千葉県柏市、代表取締役:浅川純、以下「Pale Blue社」)と軌道上実証に関するサービス契約を締結いたしましたので、下記の通りお知らせいたします。 当社は、AxelLiner事業発の新サービスとして、宇宙用コンポーネントの軌道上実証に特化したAxelLiner Laboratory(以下、AL Lab)のサービスを提供しております。本契約ではPale Blue社が開発する、起動時間が短いホールスラスタの実証を2027年に予定しております。 軌道上実証ミッションは実施頻度が低く、また、採択から打ち上げまでに数年かかってしまうことから、タイムリーな実証が難しいことが挙げられます。 そのような中、宇宙戦略基金をはじめとする政府機関が推進する宇宙政策において、国内の...

-

アクセルスペース、Exolaunchとの衛星打上げに関するマルチ ローンチ アグリーメントおよび新たな衛星の打上げに合意

東京--(BUSINESS WIRE)--(ビジネスワイヤ) -- 小型衛星を開発・運用し、誰もが宇宙を利用できる社会を目指して事業を展開する株式会社アクセルスペース(本社:東京都中央区、代表取締役:中村友哉、以下「当社」)は、打上げミッションマネジメントや衛星統合、衛星展開技術のグローバルリーダーであるExolaunch GmbH(本社:ドイツ、CEO: Robert W. Sproles、以下「Exolaunch社」)とマルチローンチアグリーメント(multi-launch agreement、以下、「MLA」)の契約及び新たな衛星打上げスロット確保の契約について合意いたしましたので、お知らせいたします。 今回の契約および合意により、当社のAxelLiner事業での軌道上実証サービス「AxelLiner Laboratory」に供する小型衛星1機の打上げ機会が、Exolaunchにより確保されます。なお、本件および同社と契約を締結している打上げスロット手配契約7機分を含め、現時点でExolanchにより合計8機の打上げ機会を確保することとなります。 当社は、AxelLiner事業...

-

Zambon Biotech annonce la première administration d'IPX203 à un patient dans le cadre de l'étude clinique ADIP de phase 3b dans la maladie de Parkinson

CADEMPINO, Suisse--(BUSINESS WIRE)--Zambon Biotech, une biotech spécialisée faisant partie du groupe Zambon visant à constituer un portefeuille scientifiquement solide et commercialement viable de médicaments innovants centrés sur le patient grâce à l'identification, à l’acquisition, à l’octroi de licences et au développement de nouvelles molécules, annonce aujourd'hui que le premier patient à un stade avancé de la maladie de Parkinson stade avancé a été inclus dans l’étude européenne ADIP de p...

-

Zambon Biotech Announces First Patient Dosed in Phase 3b ADIP Clinical Study of IPX203 in Parkinson’s Disease

CADEMPINO, Switzerland--(BUSINESS WIRE)--Zambon Biotech, a specialized biotech company part of the Zambon group that aims to build a scientifically robust and commercially viable portfolio of innovative patient-oriented drugs through the scouting, acquisition, licensing and development of new molecules, today announced that the first participant with advanced Parkinson’s disease has been enrolled in the European Phase 3b ADIP (IPX203 in Advanced Parkinson’s disease) study, which is planned to e...

-

Zambon Biotech annuncia l'arruolamento del primo paziente nello studio clinico di Fase 3b ADIP su IPX203 nella malattia di Parkinson

CADEMPINO, Svizzera--(BUSINESS WIRE)--Zambon Biotech, azienda biotech parte del gruppo Zambon impegnata nella creazione di un portafoglio scientificamente solido e commercialmente valido di farmaci innovativi orientati al paziente tramite lo scouting, l’acquisizione, il licensing e lo sviluppo di nuove molecole, annuncia oggi che il primo paziente con malattia di Parkinson avanzata è stato arruolato nello studio europeo di Fase 3b ADIP (IPX203 in Advanced Parkinson’s disease), progettato per va...

-

Zambon Biotech meldet erste Dosisverabreichung der klinischen Phase-3b-Studie ADIP zu IPX203 bei Parkinson

CADEMPINO, Schweiz--(BUSINESS WIRE)--Zambon Biotech – ein spezialisiertes Biotechnologie-Unternehmen der Zambon-Unternehmensgruppe, das den Aufbau eines wissenschaftlich fundierten und wirtschaftlich tragfähigen Portfolios innovativer und patientenorientierter Arzneimittel anstrebt – gab heute bekannt, dass der erste Teilnehmer mit fortgeschrittener Parkinson-Krankheit in die europäische Phase-3b-Studie ADIP (IPX203 bei fortgeschrittener Parkinson-Krankheit) eingeschlossen wurde. Diese Phase-3-...

-

Resumen: Zambon Biotech anuncia la administración al primer paciente en el estudio clínico ADIP fase 3b de IPX203 para Mal de Parkinson

CADEMPINO, Suiza--(BUSINESS WIRE)--Zambon Biotech, una empresa de biotecnología especializada que forma parte del Grupo Zambon con el objetivo de diseñar una cartera de fármacos innovadores orientados a pacientes que sea comercialmente viable y científicamente sólida a través de la exploración, la adquisición, el licenciamiento y el desarrollo de moléculas nuevas, anunció hoy que el primer participante con Enfermedad de Parkinson en estadio avanzado fue inscrito en el estudio ADIP (IPX203 para...