Newsroom

Sorted by: Latest

-

Laverock Therapeutics Reports Key Oncology Research Milestones

LONDON--(BUSINESS WIRE)--Laverock Therapeutics (‘Laverock’), a biotechnology company developing disease-responsive advanced therapies through its unique, programmable gene control technology, today announced key in-vivo functional milestones across its T-cell and macrophage oncology programmes for solid tumour indications. The data support lead programme selection and progression towards the clinic. Laverock’s platform technology enables programmable, tunable and multiplex gene control for both...

-

GlobalFoundries en Qualinx demonstreren Europa's eerste soevereine productieketen voor beveiligingskritische halfgeleiders

DRESDEN, Duitsland & DELFT, Nederland--(BUSINESS WIRE)--GlobalFoundries and Qualinx Demonstrate First European Sovereign Manufacturing Flow for Security‑Critical Semiconductors...

-

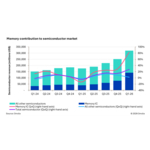

Omdia: Semiconductor Market Surpasses $300bn Quarterly Revenue in 1Q26 as Memory Market Shifts Historical Patterns

LONDON--(BUSINESS WIRE)--Following a record-setting year for the semiconductor industry, the start of the new year has continued the momentum, as semiconductor revenue grew 27% in 1Q26 from 4Q25 to reach $319bn, according to new research form Omdia. Memory revenue drove the increase, rising over 80% sequentially in 1Q26 from 4Q25. Since Omdia began tracking the semiconductor market at a quarterly level in1Q02, this 27% quarter-over-quarter (QoQ) growth is the highest observed. The market has no...

-

NextSilicon to Productize Arbel RISC-V Core Into 64-Core Enterprise Processor for AI and HPC

BOLOGNA, Italy--(BUSINESS WIRE)--NextSilicon, a leader in next-generation computing solutions for AI and high-performance computing (HPC), today announced plans to productize its Arbel RISC-V core into a 64-core and a 128-core, enterprise-grade processor suited to deliver ultra-speed performance for agentic tools, expected to be available in early 2028. Following an October preview, the company is now sharing expanded technical detail and a roadmap shaped by early customer and partner feedback....

-

Lewis & Clark Capital Announces the Formation of AirCore Environmental

ST. LOUIS--(BUSINESS WIRE)--Lewis & Clark Capital today announced the formation of AirCore Environmental, a new indoor air quality ("IAQ") platform built through the acquisitions of Radon Mitigation Services ("RMS") and Radon Professional Services ("RPS"). AirCore provides radon mitigation services predominantly to commercial customers across the Southeastern United States, with a mission to help property owners, managers, and builders create safer, healthier indoor environments. Formed by...

-

Riassunto: OKX lancia X-Perps sui titoli Magnificent 7, oro, argento e petrolio per i trader europei

AMSTERDAM--(BUSINESS WIRE)--OKX, una società fintech globale leader nel settore, nonché piattaforma di trading di criptovalute, oggi ha lanciato 13 nuovi mercati X-Perp per trader in tutta Europa, dando agli utenti retail un accesso diretto ai futures sui titoli tecnologici "Magnificent 7", quattro principali materie prime e i principali* indici mondiali. A partire da oggi, i clienti OKX in Europa possono negoziare futures su Apple, Amazon, Alphabet, Meta, Microsoft, Nvidia e Tesla, assieme a o...

-

Hack The Box and Semperis Form Strategic Technology Alliance to Advance Enterprise Identity Resilience

NEW YORK & HOBOKEN, New Jersey--(BUSINESS WIRE)--Hack The Box (HTB), the global leader in AI cybersecurity readiness, and Semperis, the identity-driven cyber resilience and crisis management company, today announced a strategic technology alliance. The alliance brings together Semperis’ hybrid identity-security expertise with HTB’s hands-on cyber readiness platform, supporting security teams with the skills, workflows, and response capabilities needed to prepare for and respond to identity-base...

-

Organisation d’une visioconférence destinée aux actionnaires et investisseurs particuliers de Winamp Group

BRUXELLES--(BUSINESS WIRE)--Regulatory News: Winamp Group SA (Paris: ALWIN) (Brussels: ALWIN), propriétaire des plateformes Winamp, Bridger, Jamendo et Hotmix, annonce l’organisation d’une visioconférence à destination des actionnaires et investisseurs individuels le : LUNDI 22 juin à 18H00 (Version FR) Cette visioconférence sera l’occasion de revenir sur les dernières actualités du groupe, les avancées stratégiques du premier semestre 2026 ainsi que les priorités et perspectives pour le second...

-

Organization of a Videoconference for Winamp Group Shareholders and Retail Investors

BRUSSELS--(BUSINESS WIRE)--Regulatory News: Winamp Group SA (Paris: ALWIN) (Brussels: ALWIN), owner of the Winamp, Bridger, Jamendo and Hotmix platforms, announces the organization of a videoconference for shareholders and individual investors on: MONDAY, June 22 at 6:00 PM (French session) This videoconference will be an opportunity to review the Group’s latest developments, the strategic progress achieved during the first half of 2026, as well as the priorities and outlook for the second half...

-

GitLab Expands Collaboration with Google to Deliver a Fully Managed DevSecOps Platform with the Latest Gemini and Gemma Models

SAN FRANCISCO--(BUSINESS WIRE)--All Remote – GitLab Inc., the intelligent orchestration platform for DevSecOps, today announced a managed GitLab offering on Google Cloud, delivered by GitLab-certified managed service providers, enabling secure and sovereign deployments for enterprises. Enterprises running software development at scale benefit from having AI model access and control over their code, pipelines, and security data in the same platform. This collaboration addresses both. GitLab and...