")

")

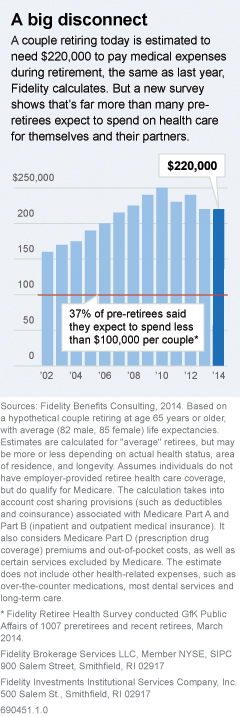

BOSTON--(BUSINESS WIRE)--Couples retiring at age 65 are expected to incur $220,000 in health care costs on average during their retirement years1, according to the 2014 Retiree Health Care Cost Estimate2 by Fidelity Investments®. The estimate is consistent with 2013 and doesn’t include the added expenses of nursing home or long-term care and assumes traditional Medicare coverage. While unchanged over 2013, the estimate reinforces the need to incorporate health care into retirement planning conversations – including how much to save and when to retire.

A recent Fidelity survey3 found that when asked, pre-retirees planned to retire at an average age of 65. However, recently retired respondents said they did so at 62 on average, often by choice but sometimes due to health issues or physical limitations. This gap points to a growing reality for many individuals and couples who are at risk of facing far greater health care costs in retirement than anticipated.

In response, Fidelity estimated the possible extra health care costs for couples who start their retirement at 62 as well as potential savings for those who can delay it to 674. Similar to the decision pre-retirees make about when to start claiming Social Security5, health care costs should be factored in to the retirement timing decision. For couples who opt to retire at age 62, they can anticipate an additional estimated cost of $17,000 per year. The extra costs are health insurance premiums for this period prior to Medicare eligibility and estimated out-of-pocket costs. On the other hand, the potential annual cost reduction for couples who can delay retirement to 67 could be $10,000 per year.

“Rising health care expenses are forcing people to make educated decisions now more than ever, ranging from the services they utilize to the age at which they choose to retire,” said Brad Kimler, executive vice president of Fidelity’s Benefits Consulting business. “We understand some people don’t have a choice in when they retire. Sometimes health issues or someone’s occupation play a role. So it’s critical that people plan well in advance for the considerable cost of health care by adding it into their overall retirement planning discussions.”

Health Care Costs for Retirees Remain Daunting, but have Moderated

Fidelity’s estimate underscores that while health care costs in retirement are significant, they have moderated in recent years. Factors that play a role include:

- Long-term prescription drug savings due to the gradual closure of Medicare Part D’s “donut hole”6 leaving retirees with a reduced, 25 percent co-insurance cost by 2020 where there was previously no coverage at all.

- The trend of slower Medicare spending per enrollee through 2022, as projected by the U.S. Department of Health & Human Services7.

- An increasingly cautious – and selective – health care consumer as ongoing economic uncertainty is leading to reduced utilization of discretionary health care services, such as elective surgeries.

“Even if couples make informed decisions, the only real prescription to prepare financially for health care costs in retirement is to plan well in advance to optimize health and wealth,” said Kimler.

Consider Tax-Advantaged Health Care Savings Opportunities

In an effort to help both companies and employees reduce health care expenses, many companies offering high-deductible health plans (HDHP) combine them with health savings accounts (HSA). Similar to how workplace retirement savings plans such as 401(k)s provide tax-advantaged savings, HSAs offer tax-advantaged opportunities to save for qualified medical expenses both today and in retirement.

Fidelity encourages employers to consider adopting HDHPs and HSAs to help foster a culture of savings within their workplace. The combination of an HDHP and HSA makes for a powerful health care savings option now and in the future, as HSAs allow pre-tax dollars that are unspent each year to carry over and stay invested tax free for qualified medical expenses in retirement8.

Fidelity Urges People to Seek Guidance on How to Transition into Retirement

To help individuals and couples better plan for health care expenses in retirement, Fidelity issued two informative Viewpoints articles (“Retiree Health Costs Fall” and “How to Tame Retiree Health Care Costs”). The firm also provides comprehensive guidance to its workplace participants through its Plan for Life experience. Part of this experience helps pre-retirees transition into retirement by offering comprehensive retiree income solutions; guidance around how and when to begin claiming Social Security payments; and help finding private insurance options on the exchange marketplace9. Participants receive guidance from licensed benefit advisors who offer assistance navigating the Medicare exchange environment and selecting Medicare Advantage and Medicare Supplemental plans from national and regional providers. This support complements ongoing retirement guidance from Fidelity to help participants adapt to their changing needs.

Media-Ready Infographics

Media-ready infographics about 2014’s estimate are available for download. One includes the history of the estimated costs of health care in retirement and the other looks at the costs of retiring early or later, along with compelling survey data on when people expect to retire and how much they anticipate spending on health care.

About Fidelity’s Benefits Consulting

Fidelity’s Benefits Consulting business helps employers nationwide assess the effectiveness of their benefits programs. The business provides a holistic approach to benefits design, strategy, funding, communications and delivery by looking at clients’ health care and retirement plans before diagnosing business solutions. The group’s specialties include retirement and health care plan consulting, custom data administration, compliance and employee communication. Benefits Consulting has offices in Boston, New York City, San Francisco, Chicago, Raleigh, Dallas and Merrimack, N.H.

About Fidelity Investments

Fidelity Investments is one of the world’s largest providers of financial services, with assets under administration of $4.7 trillion, including managed assets of $1.9 trillion, as of April 30, 2014. Founded in 1946, the firm is a leading provider of investment management, retirement planning, portfolio guidance, brokerage, benefits outsourcing and many other financial products and services to more than 20 million individuals and institutions, as well as through 5,000 financial intermediary firms. For more information about Fidelity Investments, visit www.fidelity.com.

Fidelity Brokerage Services LLC, Member NYSE, SIPC

900

Salem Street, Smithfield, RI 02917

Fidelity Investments Institutional Services Company, Inc.

500

Salem St., Smithfield, RI 02917

690433.1.0

©2014 FMR LLC. All rights reserved.

1 2014 Fidelity analysis performed by its Benefits Consulting group.

2 Fidelity Benefits Consulting, 2014. Based on a hypothetical couple retiring in 2014, 65 years or older, with average (82 male, 85 female) life expectancies. Estimates are calculated for "average" retirees, but may be more or less depending on actual health status, area of residence, and longevity. The Fidelity Retiree Health Care Costs Estimate assumes individuals do not have employer-provided retiree health care coverage, but do qualify for the federal government’s insurance program, Medicare. The calculation takes into account cost-sharing provisions (such as deductibles and coinsurance) associated with Medicare Part A and Part B (inpatient and outpatient medical insurance). It also considers Medicare Part D (prescription drug coverage) premiums and out-of-pocket costs, as well as certain services excluded by Medicare. The estimate does not include other health-related expenses, such as over-the-counter medications, most dental services and long-term care.

3 Survey performed for Fidelity Investments by GfK Public Affairs and Corporate Communications in February 2014, using GfK’s KnowledgePanel of 1,007 U.S. adults ages 55-70.

4 Analysis only valid for ages 62-67 and couples retiring in 2014.

5 Social Security’s full retirement age depends on a person’s year of birth and may be determined by visiting www.ssa.gov.

6 Analysis from The Medicare Blog of the Centers for Medicare & Medicaid Services.

7 U.S Department of Health & Human Services. Office of the Assistant Secretary for Planning and Evaluation. Growth in Medicare Spending Per Beneficiary Continues to Hit Historic Lows. By Richard Kronick and Rosa Po, January 7, 2013.

8 With respect to federal taxation only. Contributions, earnings and distributions may or may not be subject to state taxation.

9 Service provided with OneExchangeTM, a business of Towers Watson.